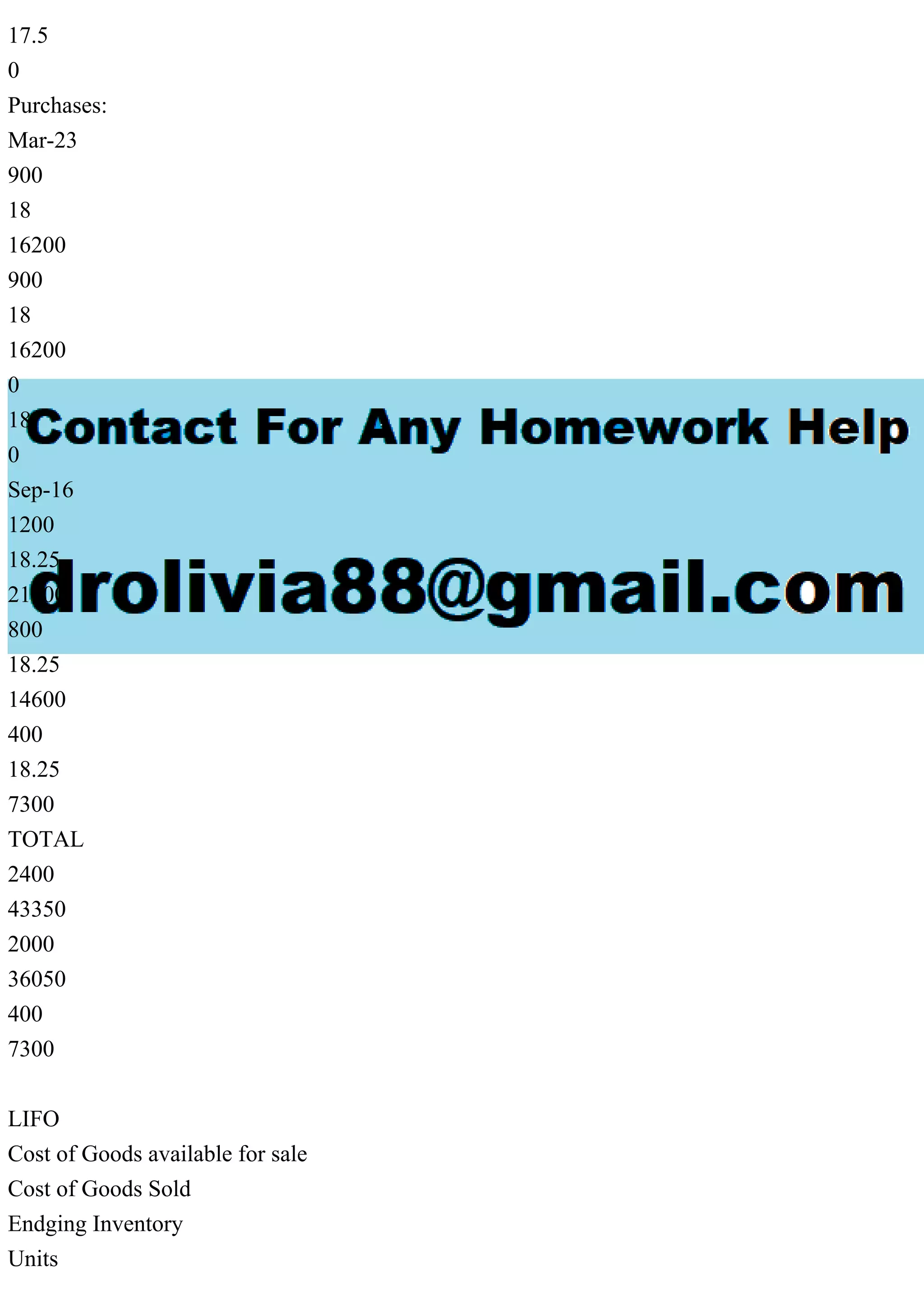

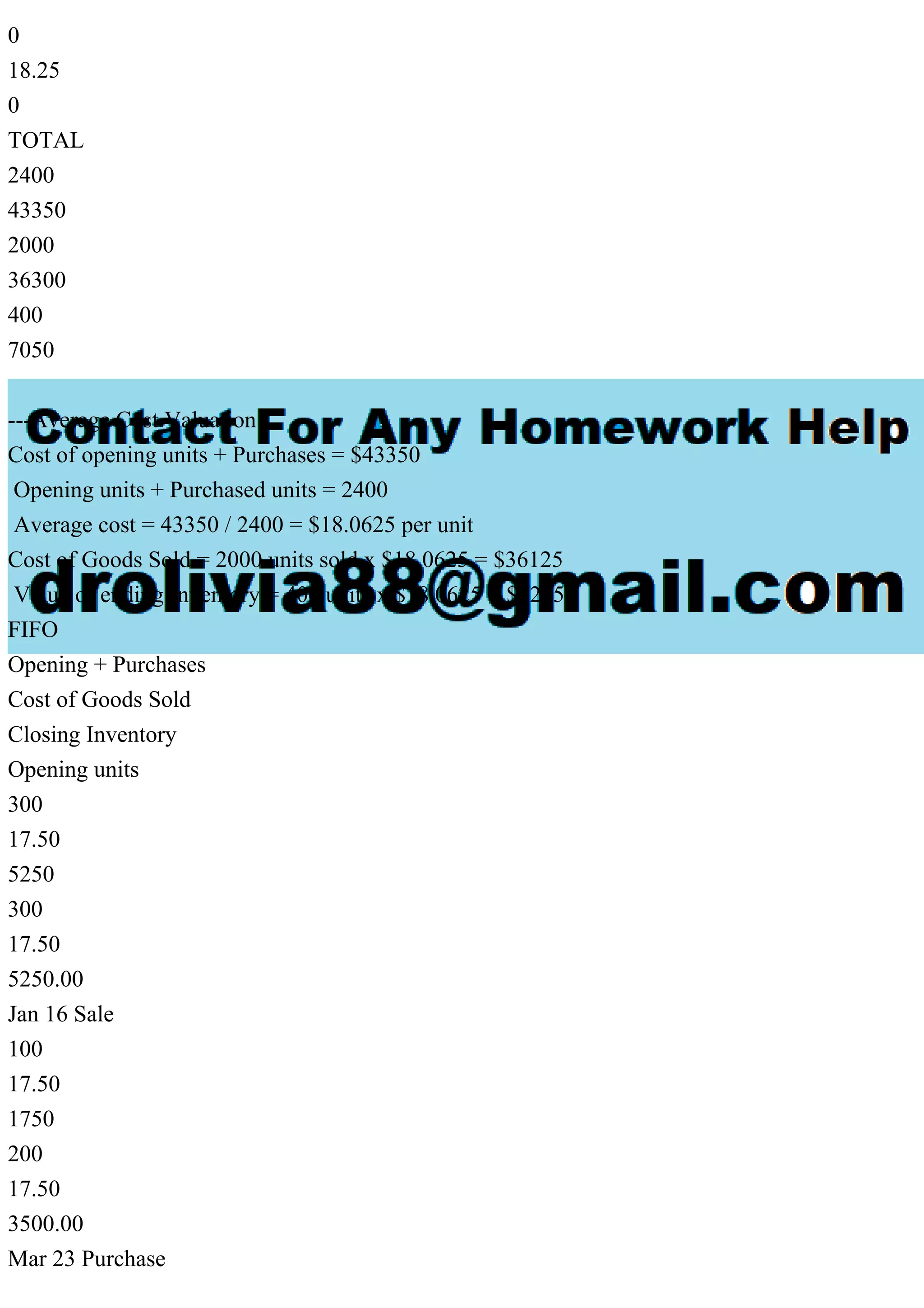

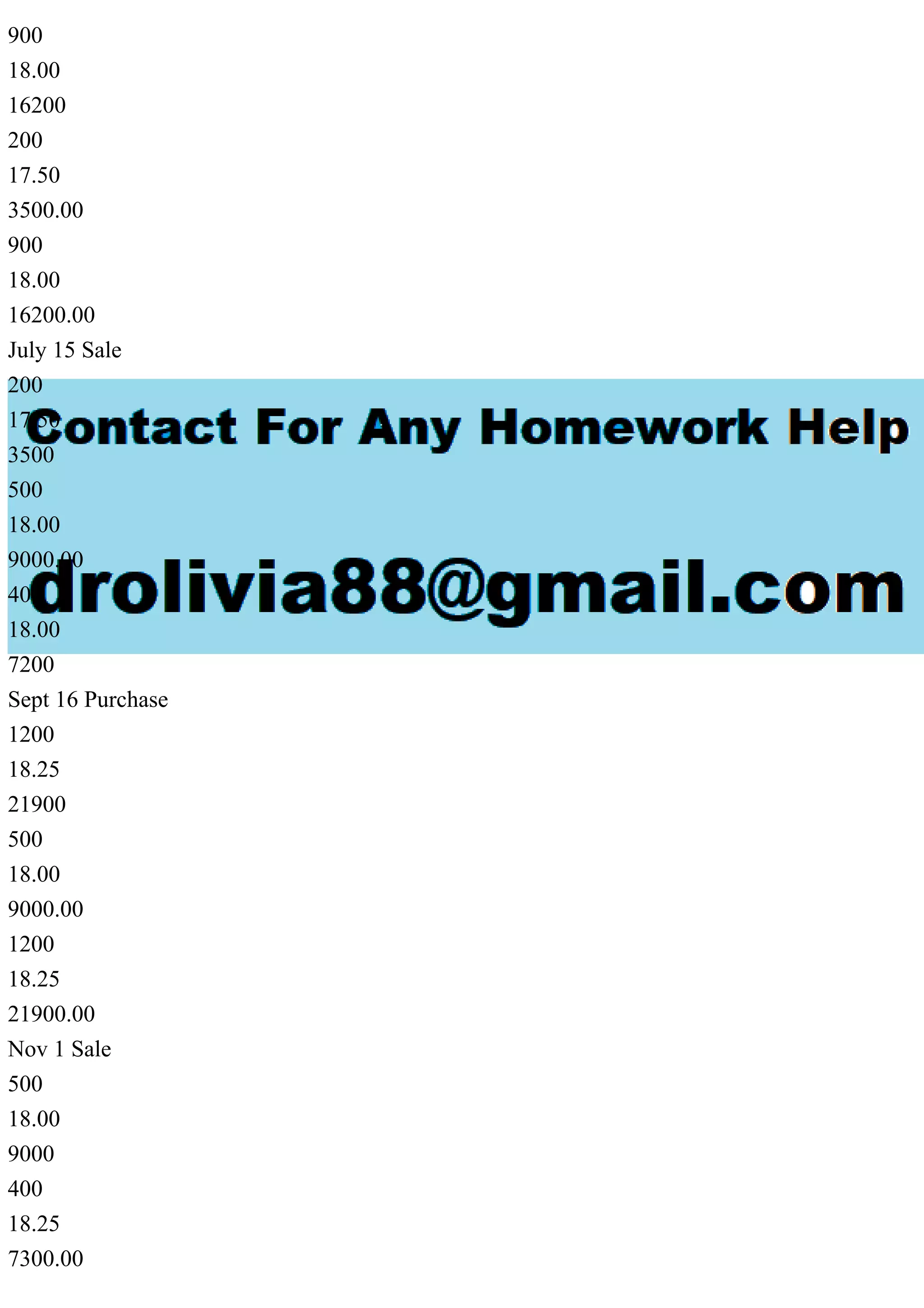

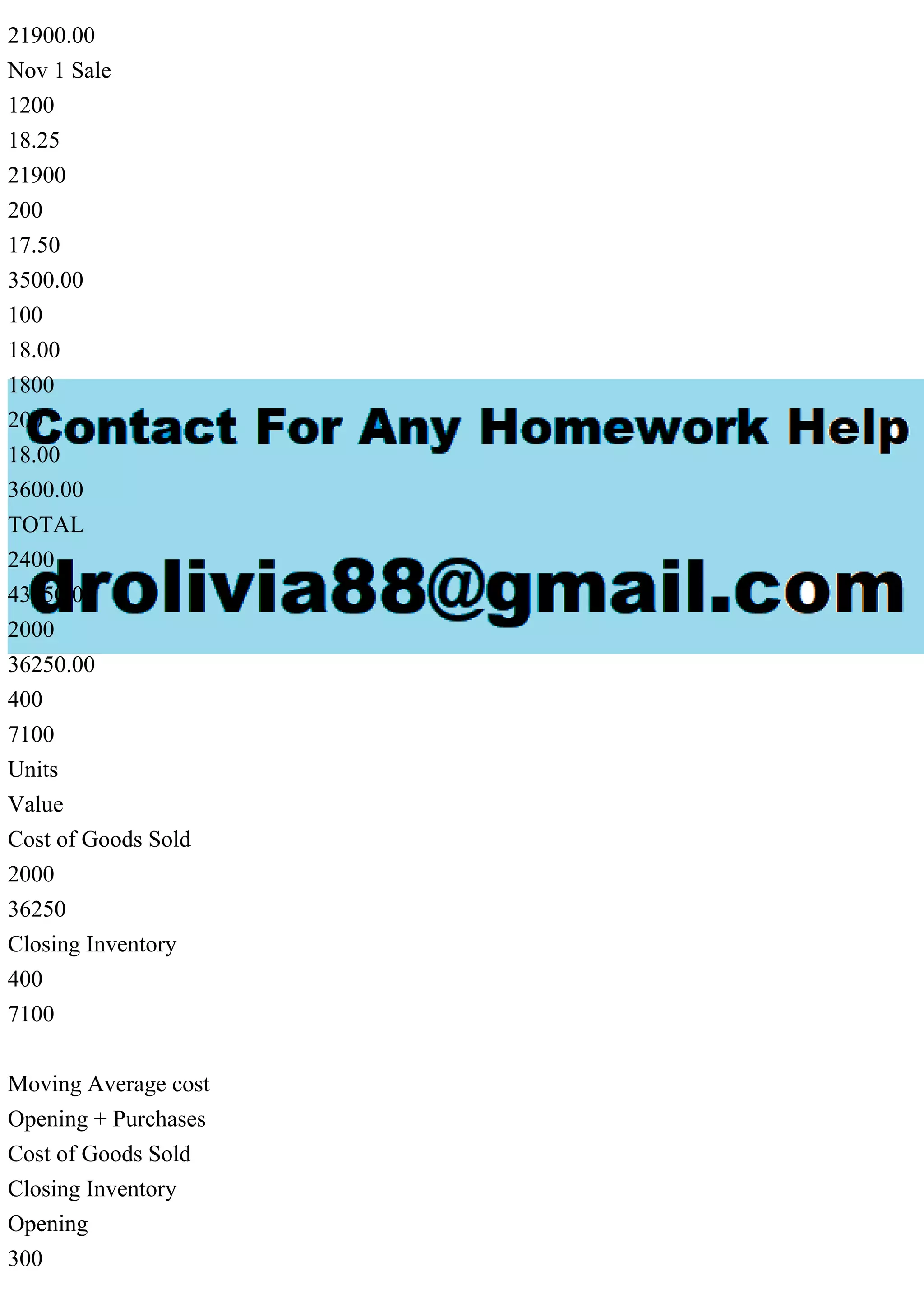

The document discusses inventory valuation methods including FIFO, LIFO, and average cost, detailing the calculations for cost of goods sold and ending inventory under different scenarios. It provides numerical data from inventory transactions and sales to illustrate the impact of each valuation method. Additionally, it includes computations for a periodic and perpetual inventory system for the given units and costs.