Islamic banking operates under Shariah law, emphasizing profit and loss sharing while prohibiting interest (riba). It employs mechanisms like mudaraba and musharaka, where banks and clients share the risks and rewards of investment, and offers financing through trade-based contracts such as murabaha and ijarah. Ultimately, Islamic banking aims to promote ethical business practices and ensure fair distribution of wealth without engaging in interest-based transactions.

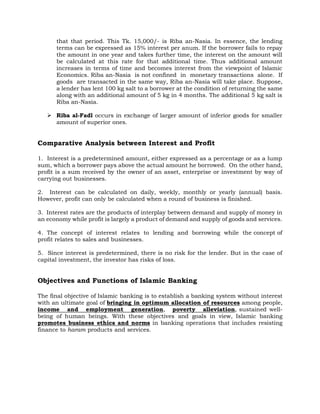

![Deposit Mobilization Process in Islamic Banking

Deposit in Islamic Banking comes from two main ways—funds laid by customers

in the hands of Islamic banker for safekeeping [Al-wadiah] and funds invested by

customers with Islamic banker to run business with on profit-sharing contracts

[Mudaraba].

In Al-Wadia contracts, customers lay funds in Islamic banks for safekeeping without

intention of receiving any additional amount for the funds. These accounts are popularly

called al-Wadia Current Accounts as well. The features of al-Wadia Account—

1) There are two parties in an al-Wadia contract—depositor (al-Mudi) and safe-keeper

(al-Mustauda). In the context of the bank, the depositor is the client and the safe-keeper

is the bank and the money that is kept for safekeeping is deposit (al-Wadia).

2) The main intention of the client to lay money with the bank under this contract is

safe-keeping and returning immediately on demand.

3) The depositor allows the bank to invest the money elsewhere, of course subject to the

Shariah principles, for the benefits of the bank only, not for any direct benefit of the

client.

4) The bank is not bound to share the profit earned from the investment of the deposit

with its depositor.

5) For safekeeping of the money, on-demand withdrawal facilities and other banking

services related to it, the bank can charge fees.

6) Since accounts conducted on the al-Wadia contract serve all the purpose of the

current accounts of a conventional bank, al-Wadiah accounts are a Shariah-based

equivalent of conventional current accounts.

Mudaraba is a business contract between two parties, where one party provides funds

and the other party provides managerial skill and experience for an enterprise. The party

providing fund is Saahib al-Maal and the party employing managerial skill is Mudarib.

The features of the Mudarabah Account—

1) Both the parties to Mudarabah contract should be capable of appointing agents and

accepting agency.

2) Any of the parties can terminate the contract unilaterally unless the Mudarib

has already started the business. In that case the termination of the Mudaraba contract

can only be done on mutual consent.

3) There should be a definite agreement between the parties as to the ratio on which the

profit is to be distributed between the parties. However, the profit cannot be a lump sum

or a percentage of the capital.](https://image.slidesharecdn.com/introductiontoislamicbankingconceptprincipalpractice-240703165330-e25e686b/85/Introduction-to-Islamic-Banking-concept-principal-practice-pdf-5-320.jpg)