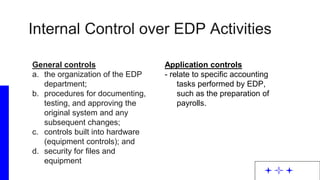

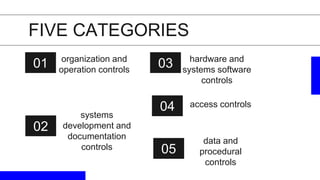

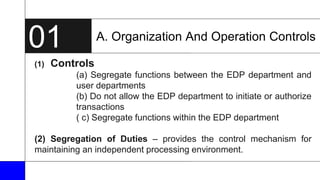

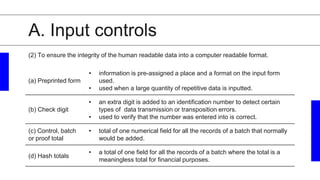

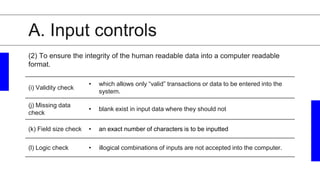

This document discusses internal controls in computer information systems. It outlines five categories of general controls: 1) organization and operation controls, 2) systems development and documentation controls, 3) hardware and systems software controls, 4) access controls, and 5) data and procedural controls. It also discusses application controls which relate to specific accounting tasks performed by computer systems, including input, processing, and output controls. The document provides examples of controls within each category to ensure integrity, authorization and security of data processing.

![4 Gestion d’entreprise et management Unité 3.ppt[Compatibility Mode].pdf](https://cdn.slidesharecdn.com/ss_thumbnails/4gestiondentrepriseetmanagementunit3-230118105138-84dec1f2-thumbnail.jpg?width=640&height=640&fit=bounds)