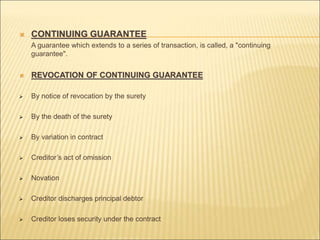

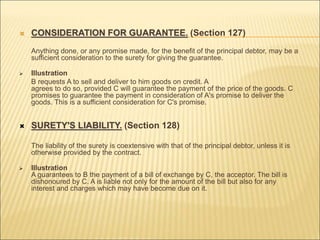

This document discusses contracts of indemnity and guarantee under Indian contract law. It defines a contract of indemnity as one where one party promises to save the other from loss caused by the conduct of the promisor or a third party. A contract of guarantee involves three parties - a principal debtor, a creditor, and a surety who guarantees to perform or discharge the liability of the debtor in case of default. The document outlines the rights and obligations of parties under these contracts and circumstances under which a surety may be discharged.

![ CONTRACT OF INDEMNITY

A contract by which one party promises to save the other from loss caused to him by

the conduct of the promisor himself, or by the conduct of any other person, is called a

‘contract of indemnity. [section 124].

For Example - A contracts to indemnify B against the consequences of any

proceedings which C may take against B in respect of a certain sum of 200 rupees.

This is a contract of indemnity.

PARTIES TO CONTRACT OF INDEMNITY:

INDEMNIFIER: The person who promises to indemnify.

INDEMNITY HOLDER: The person whose loss is to be indemnified.

Examples:

Motor insurance

Marine insurance

Fire insurance

Life insurance is not the contract of indemnity.](https://image.slidesharecdn.com/indemnityandguarantee-220716111028-da5f28bf/85/Indemnity_and_guarantee-ppt-2-320.jpg)

![ CONTRACT OF GUARANTEE

A “contract of guarantee” is a contract to perform the promise, or discharge the

liability, of a third person in case of his default. A guarantee may be either oral or

written. [section 126].

PARTIES TO CONTRACT OF GUARANTEE

SURETY: The person who gives the guarantee is called the “surety”. Person giving

guarantee is also called as ‘guarantor’. ;

PRINCIPAL DEBTOR: the person in respect of whose default the guarantee is given

is called the “principal debtor”, and

CREDITOR: the person to whom the guarantee is given is called the “creditor”.

Three parties are involved in contract of guarantee. Contract between any two of

them is not a ‘contract of guarantee’. It may be contract of indemnity.

Primary liability is of the principal debtor. Liability of surety is secondary and arises

when Principal Debtor fails to fulfill his commitments. However, this is so when surety

gives guarantee at the request of principal debtor. If the surety gives guarantee on his

own, then it will be contract of indemnity. In such case, surety has all primary

liabilities.](https://image.slidesharecdn.com/indemnityandguarantee-220716111028-da5f28bf/85/Indemnity_and_guarantee-ppt-4-320.jpg)