Downloaded 39 times

![AGREEING THE TERMS OF AUDIT ENGAGEMENTS

ISA 210 APPENDIX 1 120

Appendix 1

(Ref: Para. A23–24)

Example of an Audit Engagement Letter

The following is an example of an audit engagement letter for an audit of general purpose

financial statements prepared in accordance with International Financial Reporting

Standards. This letter is not authoritative but is intended only to be a guide that may be

used in conjunction with the considerations outlined in this ISA. It will need to be varied

according to individual requirements and circumstances. Itisdrafted to referto theauditof

financial statements for a single reporting period and would require adaptation if intended

or expected to apply to recurring audits (see paragraph 13 of this ISA). It may be

appropriate to seek legal advice that any proposed letter is suitable.

***

To the appropriate representative of management or those charged with governance of

ABC Company:1

[The objective and scope of the audit]

You2

have requested that we audit the financial statements of ABC Company, which

comprise the balance sheet as at December 31, 20X1, and the income statement,

statement of changes in equity and cash flow statement for the year then ended, and a

summary of significant accounting policies and other explanatory information. We are

pleased to confirm our acceptance and our understanding of this audit engagement by

means of this letter. Our audit will be conducted with the objective of our expressing an

opinion on the financial statements.

[The responsibilities of the auditor]

We will conduct our audit in accordance with International Standards on Auditing

(ISAs). Those standards require that we comply with ethical requirements and plan and

perform the audit to obtain reasonable assurance about whether the financial statements

are free from material misstatement. An audit involves performing procedures to obtain

audit evidence about the amounts and disclosures in the financial statements. The

procedures selected depend on the auditor’s judgment, including the assessment of the

risks of material misstatement of the financial statements, whether due to fraud or error.

An audit also includes evaluating the appropriateness of accounting policies used and

1

The addressees and references in the letter would be those that are appropriate in the circumstances of the

engagement, including the relevant jurisdiction. It is important to refer to the appropriate persons – see

paragraph A21.

2

Throughout this letter, references to “you,” “we,” “us,” “management,” “those charged with governance”

and “auditor” would be used or amended as appropriate in the circumstances.](https://image.slidesharecdn.com/sothg9kmtak0wgtykkaw-signature-90399e2b9d06683042b09873aff3d393c20ae73b32b9f2673d4460e3dcb28b61-poli-140718202828-phpapp02/85/Iaasb-handbook-vol-1-0-126-320.jpg)

![AGREEING THE TERMS OF AUDIT ENGAGEMENTS

ISA 210 APPENDIX 1121

AUDITING

the reasonableness of accounting estimates made by management, as well as evaluating

the overall presentation of the financial statements.

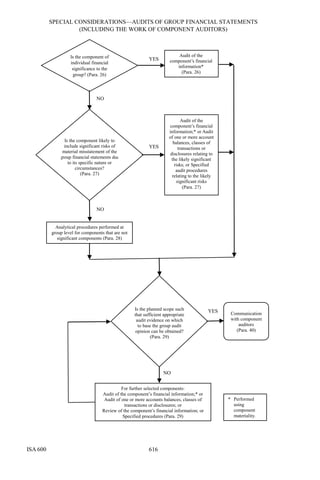

Because of the inherent limitations of an audit, together with the inherent limitations of

internal control, there is an unavoidable risk that some material misstatements may not be

detected, even though theaudit isproperly planned and performed in accordance withISAs.

In making our risk assessments, we consider internal control relevant to the entity’s

preparation of the financial statements in order to design audit procedures that are

appropriate in the circumstances, but not for the purpose of expressing an opinion on the

effectiveness of the entity’s internal control. However, we will communicate to you in

writing concerning any significant deficiencies in internal control relevant to the audit of

the financial statements that we have identified during the audit.

[The responsibilities of management and identification of the applicable financial

reporting framework (for purposes of this example it is assumed that the auditor has not

determined that the law or regulation prescribes those responsibilities in appropriate

terms; the descriptions in paragraph 6(b) of this ISA are therefore used).]

Our audit will be conducted on the basis that [management and, where appropriate, those

charged with governance]3

acknowledge and understand that they have responsibility:

(a) For the preparation and fair presentation of the financial statements in accordance

with International Financial Reporting Standards;4

(b) For such internal control as [management] determines is necessary to enable the

preparation of financial statements that are free from material misstatement,

whether due to fraud or error; and

(c) To provide us with:

(i) Access to all information of which [management] is aware that is relevant

to the preparation of the financial statements such as records,

documentation and other matters;

(ii) Additional information that we may request from [management] for the

purpose of the audit; and

(iii) Unrestricted access to persons within the entity from whom we determine

it necessary to obtain audit evidence.

As part of our audit process, we will request from [management and, where appropriate,

those charged with governance], written confirmation concerning representations made

to us in connection with the audit.

We look forward to full cooperation from your staff during our audit.

3

Use terminology as appropriate in the circumstances.

4

Or, if appropriate, “For the preparation of financial statements that give a true and fair view in

accordance with International Financial Reporting Standards.”](https://image.slidesharecdn.com/sothg9kmtak0wgtykkaw-signature-90399e2b9d06683042b09873aff3d393c20ae73b32b9f2673d4460e3dcb28b61-poli-140718202828-phpapp02/85/Iaasb-handbook-vol-1-0-127-320.jpg)

![AGREEING THE TERMS OF AUDIT ENGAGEMENTS

ISA 210 APPENDIX 1 122

[Other relevant information]

[Insert other information, such as fee arrangements, billings and other specific terms, as

appropriate.]

[Reporting]

[Insert appropriate reference to the expected form and content of the auditor’s report.]

The form and content of our report may need to be amended in the light of our audit

findings.

Please sign and return the attached copy of this letter to indicate your acknowledgement

of, and agreement with, the arrangements for our audit of the financial statements

including our respective responsibilities.

XYZ & Co.

Acknowledged and agreed on behalf of ABC Company by

(signed)

......................

Name and Title

Date](https://image.slidesharecdn.com/sothg9kmtak0wgtykkaw-signature-90399e2b9d06683042b09873aff3d393c20ae73b32b9f2673d4460e3dcb28b61-poli-140718202828-phpapp02/85/Iaasb-handbook-vol-1-0-128-320.jpg)

![EVALUATION OF MISSTATEMENTS IDENTIFIED DURING THE AUDIT

ISA 450387

AUDITING

uncorrected misstatements, rather than the details of each individual uncorrected

misstatement.

A23. ISA260 requires the auditor to communicate with those charged with governance

the written representations the auditor is requesting (see paragraph 14 of this

ISA).15

The auditor may discuss with those charged with governance the reasons

for, and the implications of, a failure to correct misstatements, having regard to the

size and nature of the misstatement judged in the surrounding circumstances, and

possible implications in relation to future financial statements.

Written Representations (Ref: Para. 14)

A24. Because the preparation of the financial statements requires management and,

where appropriate, those charged with governance to adjust the financial

statements to correct material misstatements, the auditor is required to request

them to provide a written representation about uncorrected misstatements. In

some circumstances, management and, where appropriate, those charged with

governance may not believe that certain uncorrected misstatements are

misstatements. For that reason, they may want to add to their written

representation words such as: “We do not agree that items … and … constitute

misstatements because [description of reasons].” Obtaining this representation

does not, however, relieve the auditor of the need to form a conclusion on the

effect of uncorrected misstatements.

Documentation (Ref: Para. 15)

A25. Theauditor’sdocumentationof uncorrected misstatements may take into account:

(a) The consideration of the aggregate effect of uncorrected misstatements;

(b) The evaluation of whether the materiality level or levels for particular

classes of transactions, account balances or disclosures, if any, have been

exceeded; and

(c) The evaluation of the effect of uncorrected misstatements on key ratios or

trends, and compliance with legal,regulatory and contractual requirements

(for example, debt covenants).

15

ISA 260, paragraph 16(c)(ii)](https://image.slidesharecdn.com/sothg9kmtak0wgtykkaw-signature-90399e2b9d06683042b09873aff3d393c20ae73b32b9f2673d4460e3dcb28b61-poli-140718202828-phpapp02/85/Iaasb-handbook-vol-1-0-393-320.jpg)

![INITIAL AUDIT ENGAGEMENTS—OPENING BALANCES

ISA 510 APPENDIX435

AUDITING

Appendix

(Ref: Para. A8)

Illustrations of Auditors’ Reports with Modified Opinions

Illustration 1:

Circumstances described in paragraph A8(a) include the following:

• The auditor did not observe the counting of the physical inventory at

the beginning of the current period and was unable to obtain sufficient

appropriate audit evidence regarding the opening balances of

inventory.

• The possible effects of the inability to obtain sufficient appropriate

audit evidence regarding opening balances of inventory are deemed to

be material but not pervasive to the entity’s financial performance and

cash flows.1

• The financial position at year end is fairly presented.

• In this particular jurisdiction, law and regulation prohibit the auditor

from giving an opinion which is qualified regarding the financial

performance and cash flows and unmodified regarding financial

position.

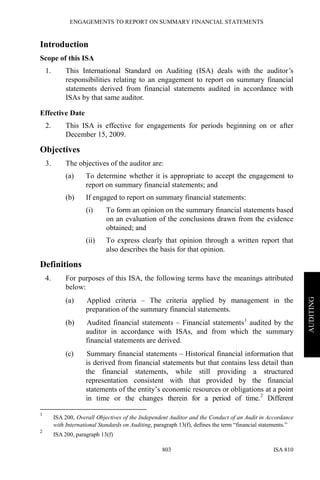

INDEPENDENT AUDITOR’S REPORT

[Appropriate Addressee]

Report on the Financial Statements2

We have audited the accompanying financial statements of ABC Company, which

comprise the statement of financial position as at December 31, 20X1, and the

statement of comprehensive income, statement of changes in equity and statement of

cash flows for the year then ended, and a summary of significant accounting policies

and other explanatory information.

Management’s3

Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these

financial statements in accordance with International Financial Reporting

1

If the possible effects, in the auditor’s judgment, are considered to be material and pervasive to the

entity’s financial performance and cash flows, the auditor would disclaim an opinion on the financial

performance and cash flows.

2

The sub-title “Report on the Financial Statements” is unnecessary in circumstances when the second

sub-title “Report on Other Legal and Regulatory Requirements” is not applicable.

3

Or other term that is appropriate in the context of the legal framework in the particular jurisdiction](https://image.slidesharecdn.com/sothg9kmtak0wgtykkaw-signature-90399e2b9d06683042b09873aff3d393c20ae73b32b9f2673d4460e3dcb28b61-poli-140718202828-phpapp02/85/Iaasb-handbook-vol-1-0-441-320.jpg)

![INITIAL AUDIT ENGAGEMENTS—OPENING BALANCES

ISA 510 APPENDIX437

AUDITING

determination of the financial performance and cash flows, we were unable to

determine whether adjustments might have been necessary in respect of the profit for

the year reported in the statement of comprehensive income and the net cash flows

from operating activities reported in the statement of cash flows.

Qualified Opinion

In our opinion, except for the possible effects of the matter described in the Basis for

Qualified Opinion paragraph, the financial statements present fairly, in all material

respects, (or give a true and fair view of) the financial position of ABC Company as

at December 31, 20X1, and (of) its financial performance and its cash flows for the

year then ended in accordance with International Financial Reporting Standards.

Other Matter

The financial statements of ABC Company for the year ended December 31, 20X0

were audited by another auditor who expressed an unmodified opinion on those

statements on March 31, 20X1.

Report on Other Legal and Regulatory Requirements

[Form and content of this section of the auditor’s report will vary depending on the

nature of the auditor’s other reporting responsibilities.]

[Auditor’s signature]

[Date of the auditor’s report]

[Auditor’s address]](https://image.slidesharecdn.com/sothg9kmtak0wgtykkaw-signature-90399e2b9d06683042b09873aff3d393c20ae73b32b9f2673d4460e3dcb28b61-poli-140718202828-phpapp02/85/Iaasb-handbook-vol-1-0-443-320.jpg)

![INITIAL AUDIT ENGAGEMENTS—OPENING BALANCES

ISA 510 APPENDIX 438

Illustration 2:

Circumstances described in paragraph A8(b) include the following:

• The auditor did not observe the counting of the physical inventory at

the beginning of the current period and was unable to obtain sufficient

appropriate audit evidence regarding the opening balances of

inventory.

• The possible effects of the inability to obtain sufficient appropriate

audit evidence regarding opening balances of inventory are deemed to

be material but not pervasive to the entity’s financial performance and

cash flows.7

• The financial position at year end is fairly presented.

• An opinion that is qualified regarding the financial performance and

cash flows and unmodified regarding financial position is considered

appropriate in the circumstances.

INDEPENDENT AUDITOR’S REPORT

[Appropriate Addressee]

Report on the Financial Statements8

We have audited the accompanying financial statements of ABC Company, which

comprise the statement of financial position as at December 31, 20X1, and the

statement of comprehensive income, statement of changes in equity and statement of

cash flows for the year then ended, and a summary of significant accounting policies

and other explanatory information.

Management’s9

Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these

financial statements in accordance with International Financial Reporting

Standards,10

and for such internal control as management determines is necessary to

enable the preparation of financial statements that are free from material

misstatement, whether due to fraud or error.

7

If the possible effects, in the auditor’s judgment, are considered to be material and pervasive to the

entity’s financial performance and cash flows, the auditor would disclaim the opinion on the

financial performance and cash flows.

8

The sub-title “Report on the Financial Statements” is unnecessary in circumstances when the second

sub-title “Report on Other Legal and Regulatory Requirements” is not applicable.

9

Or other term that is appropriate in the context of the legal framework in the particular jurisdiction

10

Where management’s responsibility is to prepare financial statements that give a true and fair view,

this may read: “Management is responsible for the preparation of financial statements that give a

true and fair view in accordance with International Financial Reporting Standards, and for such ...”](https://image.slidesharecdn.com/sothg9kmtak0wgtykkaw-signature-90399e2b9d06683042b09873aff3d393c20ae73b32b9f2673d4460e3dcb28b61-poli-140718202828-phpapp02/85/Iaasb-handbook-vol-1-0-444-320.jpg)

![INITIAL AUDIT ENGAGEMENTS—OPENING BALANCES

ISA 510 APPENDIX 440

Qualified Opinion on the Financial Performance and Cash Flows

In our opinion, except for the possible effects of the matter described in the Basis for

Qualified Opinion paragraph, the Statement of Comprehensive Income and

Statement of Cash Flows present fairly, in all material respects (or give a true and

fair view of), the financial performance and cash flows of ABC Company for the

year ended December 31, 20X1 in accordance with International Financial Reporting

Standards.

Opinion on the Financial Position

In our opinion, the statement of financial position presents fairly, in all material

respects (or gives a true and fair view of), the financial position of ABC Company as

at December 31, 20X1 in accordance with International Financial Reporting

Standards.

Other Matter

The financial statements of ABC Company for the year ended December 31, 20X0

were audited by another auditor who expressed an unmodified opinion on those

statements on March 31, 20X1.

Report on Other Legal and Regulatory Requirements

[Form and content of this section of the auditor’s report will vary depending

on the nature of the auditor’s other reporting responsibilities.]

[Auditor’s signature]

[Date of the auditor’s report]

[Auditor’s address]](https://image.slidesharecdn.com/sothg9kmtak0wgtykkaw-signature-90399e2b9d06683042b09873aff3d393c20ae73b32b9f2673d4460e3dcb28b61-poli-140718202828-phpapp02/85/Iaasb-handbook-vol-1-0-446-320.jpg)

This document provides an overview and introduction to the International Auditing and Assurance Standards Board's (IAASB) Handbook of International Quality Control, Auditing, Review, Other Assurance, and Related Services Pronouncements. Specifically: - It describes the structure and contents of the Handbook, which contains the complete set of IAASB standards, preface, and glossary of terms. - It outlines the authority of the standards issued by the IAASB for audits, reviews, and other assurance and related services engagements. - It addresses the applicability of the standards and describes non-authoritative material like International Auditing Practice Notes that are also included.