Downloaded 10 times

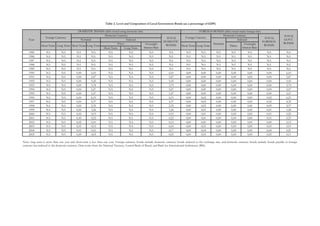

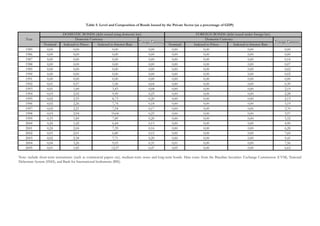

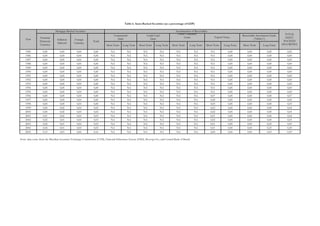

The document discusses the underdevelopment of the Brazilian bond market compared to developed countries and other emerging markets, highlighting issues such as high interest rates and limited access to credit for firms. It examines the characteristics of domestic bonds, corporate debt instruments, and regulatory frameworks, while also presenting survey results that identify key challenges like low liquidity and a lack of comprehensive benchmarks. The paper concludes with recommendations and potential policy solutions aimed at enhancing the Brazilian bond market's growth and efficiency.