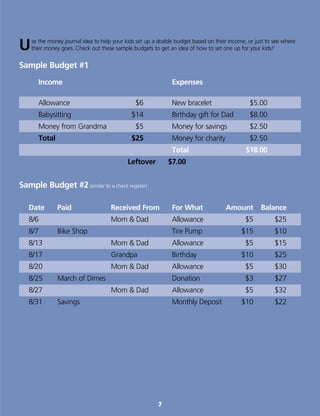

This document provides information to help parents teach their children smart money habits. It discusses the importance of modeling good financial behaviors, setting an example in spending and saving wisely, and having open conversations about money. Sample budgets are also provided to demonstrate how to help kids track their income and expenses. The goal is to equip children with skills to avoid common financial mistakes and become responsible money managers.