Downloaded 12 times

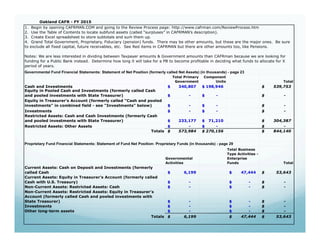

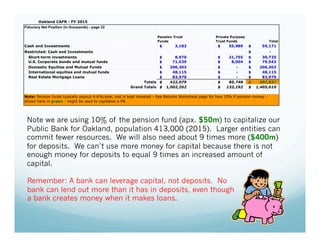

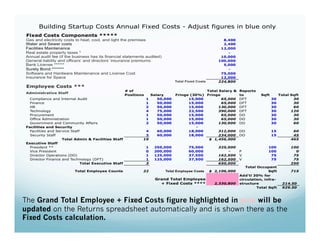

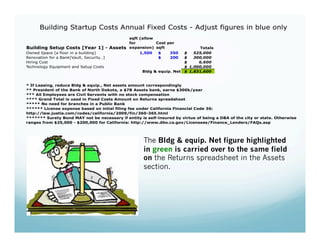

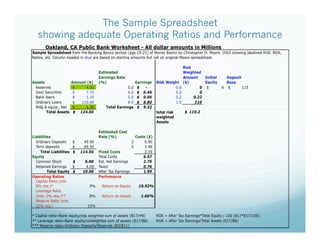

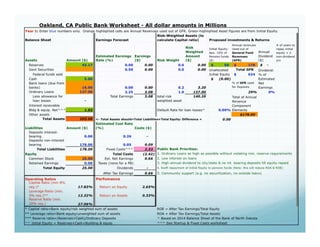

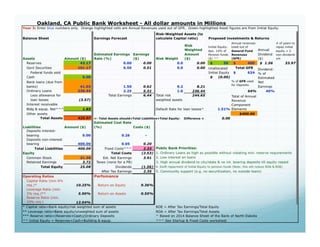

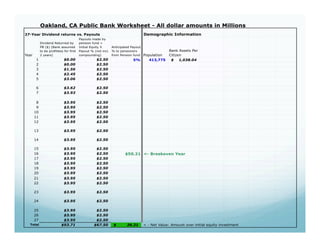

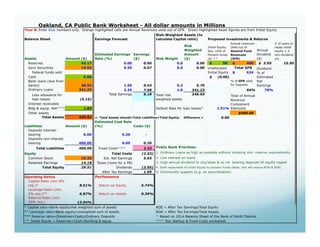

The document outlines a guide by Scott Baker on how to establish a public bank in Oakland, California. Key steps include assessing available assets for capital, determining the bank's size based on its functions, and projecting financial results over eight years. It emphasizes the importance of balancing capital and deposits and highlights the use of pension funds to capitalize the bank.