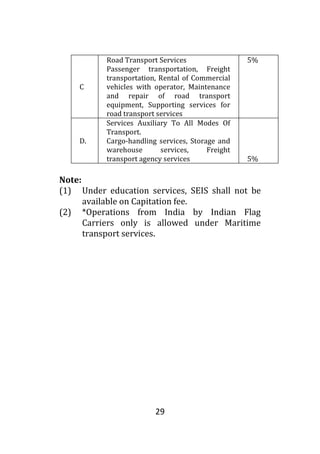

Download to read offline

![5

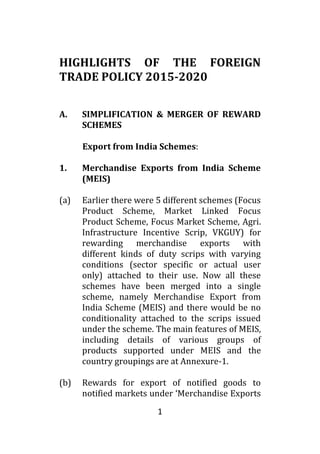

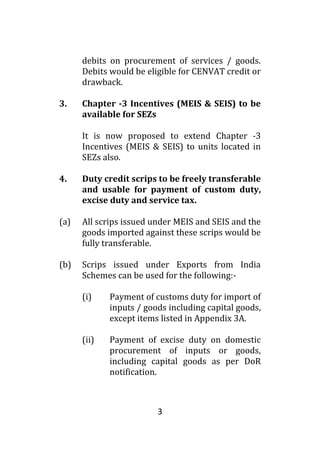

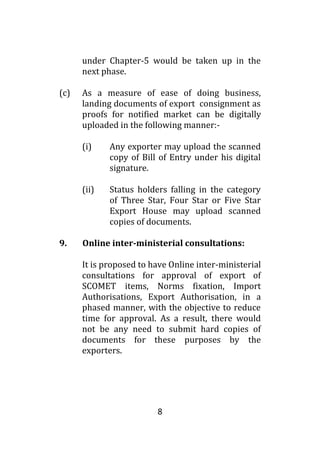

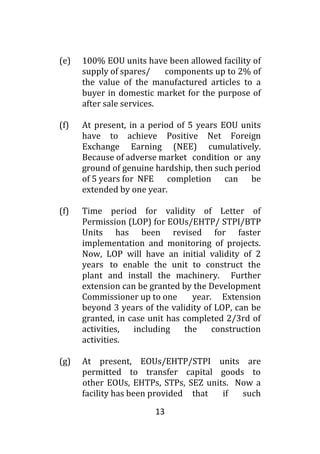

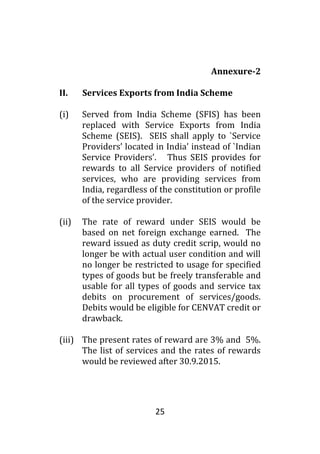

Status category

Export

Performance

FOB / FOR (as

converted)

Value (in US $

million) during

current and

previous two

years

One Star Export House 3

Two Star Export House 25

Three Star Export

House

100

Four Star Export House 500

Five Star Export House 2000

(d) Approved Exporter Scheme - Self

certification by Status Holders

Manufacturers who are also Status Holders

will be enabled to self-certify their

manufactured goods as originating from

India with a view to qualify for preferential

treatment under different Preferential

Trading Agreements [PTAs], Free Trade

Agreements [FTAs], Comprehensive

Economic Cooperation Agreements [CECAs]

and Comprehensive Economic

Partnerships Agreements [CEPAs] which are

in operation. They shall be permitted to

self-certify the goods as manufactured as per](https://image.slidesharecdn.com/cc064811-74f7-48ca-935a-b00c711db4fc-150408014805-conversion-gate01/85/highlight2015-6-320.jpg)

The document summarizes key highlights of India's Foreign Trade Policy 2015-2020. Some key points include: 1) Simplification and merger of various export reward schemes into a single Merchandise Exports from India Scheme (MEIS) and Service Exports from India Scheme (SEIS) with simplified procedures. 2) Incentives under MEIS and SEIS will be extended to Special Economic Zones to boost 'Make in India'. 3) Initiatives to facilitate trade and ease of doing business through online applications, paperless processing, and inter-ministerial consultations. 4) New initiatives to support exports of SCOMET items, defense goods, and e-commerce exports

![Optitax's presentation on carotar [07 jan 2021]](https://cdn.slidesharecdn.com/ss_thumbnails/optitaxspresentationoncarotar07jan2021-210108075952-thumbnail.jpg?width=640&height=640&fit=bounds)