Download to read offline

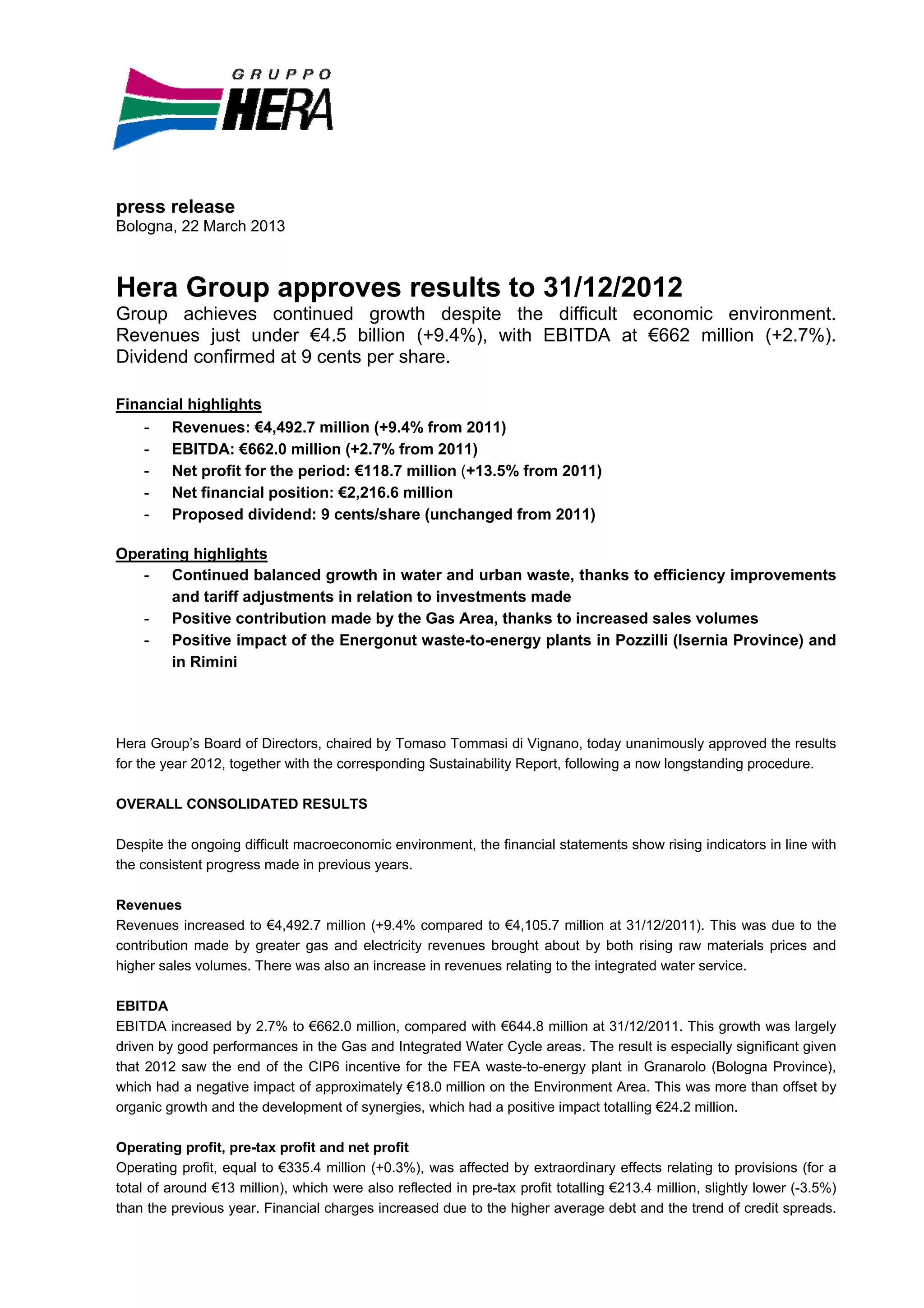

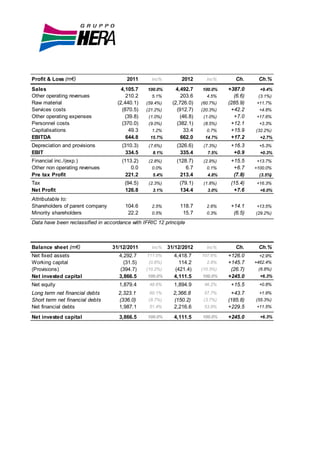

Hera Group reported revenues of €4.49 billion for 2012, a 9.4% increase from the previous year, alongside an EBITDA of €662 million, reflecting growth in the gas and integrated water sectors. Despite economic challenges, net profit rose to €118.7 million, driven by lower tax rates and strategic investments, including a proposed unchanged dividend of 9 cents per share. The results were supported by an expanding portfolio, including a merger with AcegasAps and various acquisitions in the energy and environmental sectors.