Download to read offline

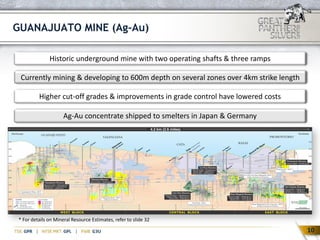

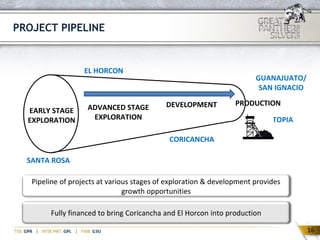

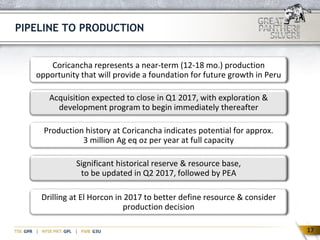

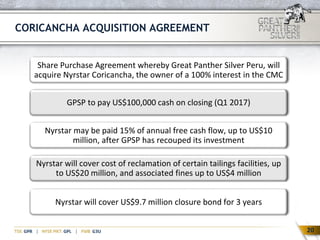

The corporate presentation provides forward-looking production guidance for 2017 of between 4-4.1 million silver equivalent ounces at a cash cost of $5-6 per ounce and all-in sustaining cost of $14-16 per ounce. It also outlines the Company's two producing mines in Mexico, the Guanajuato Mine and Topia Mine, as well as its pipeline of development projects including the near-term production opportunity at the Coricancha Mine in Peru.