More Related Content

Viewers also liked

Similar to GPC Government Purchase Card

Similar to GPC Government Purchase Card (20)

GPC Government Purchase Card

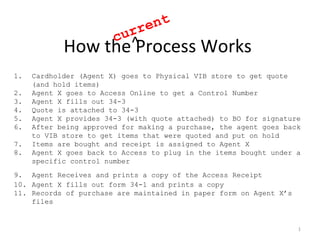

- 1. How the Process Works^current 1. Cardholder (Agent X) goes to Physical VIB store to get quote (and hold items) 2. Agent X goes to Access Online to get a Control Number 3. Agent X fills out 34-3 4. Quote is attached to 34-3 5. Agent X provides 34-3 (with quote attached) to BO for signature 6. After being approved for making a purchase, the agent goes back to VIB store to get items that were quoted and put on hold 7. Items are bought and receipt is assigned to Agent X 8. Agent X goes back to Access to plug in the items bought under a specific control number 9. Agent Receives and prints a copy of the Access Receipt 10. Agent X fills out form 34-1 and prints a copy 11. Records of purchase are maintained in paper form on Agent X’s files 1

- 2. The Staff I need printing paper! Get me a keyboard! Bring some fancy pens! Agent X vs.vs. I need printing paper! Get me a keyboard! Bring some fancy pens! Agent X HULK ANGRY! TOO MUCH EMAIL!

- 3. 3 Pens Markers Pencils Hey! Don’t forget… Paper Please Hey Agent 007, Please pick up some white paper for me! Thanks, Agent A Spammy inboxes. EW.

- 4. Agent X CARDHOLDER: Agent X MISSION: Obtain -2 packages of pen -Paper for machines -Keyboard WHEN: Bi-weekly Schedule 4

- 5. Agent X List: -2 packages of pen -Paper for machines -Keyboard STEP 1: Cardholder (Agent X) goes to Physical VIB store to get quote (and POSSIBLY hold items) 5

- 6. Agent X List: -3 packages of pen -Paper for machines -Keyboard Mr. Goldfinger, could you provide me a quote of all these items… and keep them on hold while I get my supervisor’s approval for form 34-3? Agent X Sure thing Mr. Bond, Here is your quote! STEP 1: Cardholder (Agent X) goes to Physical VIB store to get quote (and POSSIBLY hold items) 6

- 7. Agent X UGH! Paperwork…UGH! Paperwork… NOTE: Agent X does not take items; Items are left in VIB store 7

- 9. STEP 2: Agent X goes to Access Online to get a Control Number Getting a control number is basically going into the website and getting a blank check. You will need to get a control number and put this in form 34-3 9

- 10. STEP 3: Agent X finds form 34-3 and fills it out 10

- 11. Agent X All the forms are the same, the only thing that changes is the NOTE: This process can be automatized • TOTAL AMOUNT • CONTROL NUMBER • DATE • SIGNATURE STEP 3: Agent X finds form 34-3 and fills it out 11

- 13. Now that a quote has been obtained, and form 34-3 filled out, Agent X must obtain the approval of the Billing Official, Agent M. STEP 4: Quote and 34-3 are attached and prepped for B.O. (AGENT M) 13

- 14. Agent X Now, to see the B.O. Upstairs, Agent M STEP 5: Agent X provides 34-3 with Quote Attached to Billing Official (Agent M) for signature Agent MAgent M 14

- 15. Agent X Agent M, I need you to approve this purchase I want to make. Please provide your signature Approved! Agent MAgent M Agent MAgent M 15

- 16. Agent X STEP 6: After being approved for making a purchase, the agent goes back to VIB store to get items that were quoted and put on hold 16

- 17. Agent X Sure thing Mr. Bond, here is your receipt. Agent X STEP 7: Items are bought and receipt is assigned to Agent X Please charge the items I quoted and had on hold earlier to my GPC Mr.Goldfingers. 17

- 18. 18

- 19. STEP 8: Agent X goes back to Office... Agent X 19

- 20. STEP 8: Agent X goes back into Access and hand jams the purchases that were made. After he does so, he will receive a “Access Bank Receipt” NOTE: This process should be automatic, every time a purchase is made, it should automatically subtract from The Access Bank Receipt MUST Match the Amount on 34-3 20

- 21. ACCESS RECEIPT: COMPLETED STEP 9: Agent Receives and prints out a copy of the Access Receipt 21

- 22. STEP 10: Agent X fills out 34-1 to subtract from general budget and track items purchased from Supply Budget... 22

- 23. Agent X All the forms are the same, the only thing that changes is the: • Date • Agent Name • Description of Item • Quantity • Unit of Measurement • Unit Price • Total Price • Balance Pre-Purchase • Balance remaining after each individual purchase 23

- 24. FORM 34-1: COMPLETED NOTE: Form 34-1 does not prove a running tally for quick access. It is also confusing if you have more than 1 GPC holder 24

- 25. STEP 11: Given the manner in which things are done now, each purchase should contain the following materials: Quote Form 34-3 Access Receipt Form 34-1 25

- 26. STEP 11: Records of purchase are maintained in paper form on Agent X’s files 26

- 27. 27

- 28. 28

- 29. How the Process Should Work^New and improved

- 30. CARDHOLDER: Agent X MISSION: Obtain -Packages of pen -Paper for machines -Keyboard WHEN: Bi-weekly Schedule

- 31. The Staff I need printing paper! Get me a keyboard! Bring some fancy pens! Agent X vs.vs. HULK ANGRY! TOO MUCH EMAIL! I need printing paper! Get me a keyboard! Bring some fancy pens!

- 32. USE SHARED DRIVE INSTEAD OF EMAIL Less spammy email for GPC holder

- 34. Cashier Send an email with attachment of materials needed

- 35. Cashier

- 36. Cashier Supply Office sends quote back via email

- 37. Cashier

- 40. 40

- 43. Total Amount: Control Number: Date: Signature: upload VIB QUOTE: Part 1 of Ticket Number: Create a form and fill in

- 44. Total Amount: Control Number: Date: Signature: 1/11/2013 Adobe Signature $415 ABC123 1/11/2013 1/11/2013 1/11/2013 1/11/2013 1/11/2013 1/11/2013 ABC123 $415 Agent X Agent X Agent X upload VIB QUOTE: ----------- - Part 1 of Ticket Number: OL-200-10079 OL-200-10079 SUBMIT and EMAIL

- 45. Total Amount: Control Number: Date: Signature: 1/11/2013 Adobe Signature $415 ABC123 upload VIB QUOTE: ----------- - Part 1 of Ticket Number: OL-200-10079 SUBMIT and EMAIL

- 46. Agent X, Form 34-3 and quote are ready for review and approval by the Billing official. Please enter the email address of the B.O. in the space below, then click send. SENDSEND

- 49. 1/11/2013 1/11/2013 1/11/2013 1/11/2013 1/11/2013 1/11/2013 ABC123 $415 Agent X Agent X Agent X OL-200-10079 Billing Official Agent M APPROVED!

- 51. Store in the cloud!

- 52. 34-3 with signatures of Agent X (GPC holder) and Agent M (billing official) saved to cloud

- 54. List: -3 packages of pen -Paper for machines -Keyboard Agent X Mr. Bond, Here is your receipt! I also sent a copy of your receipt to your EMAIL 54 Shopping!!!

- 55. 55

- 57. Total Amount Spent Part 4 of Date of Purchase Invoice Ticket Number 1/11/2013 OL-200-10039 $415 UPLOAD COPY OF INVOICE SUBMIT!

- 59. Total Amount Spent Part 4 of Date of Purchase Invoice Ticket Number 1/11/2013 OL-200-10039 $415 UPLOAD COPY OF INVOICE SUBMIT!

- 61. 34-3 with signatures of Agent X (GPC holder) and Agent M (billing official) saved to cloud Official Invoice