Download to read offline

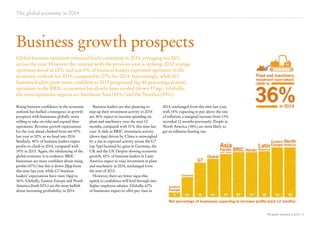

The global economy is expected to improve in 2014 with growth forecast at 3.6% after slowing to 2.9% in 2013. Business optimism and expectations for revenue, profits, and investment are up significantly from a year ago, especially in developed economies like the US, UK, and Germany. However, emerging markets face challenges from currency depreciation and slowing growth. While recoveries are taking hold in major economies, unemployment remains high in Europe and demand and skilled labor shortages constrain some business leaders. Overall uncertainties in the global economic outlook remain the top concern for businesses worldwide in 2014.