Download as PDF, PPTX

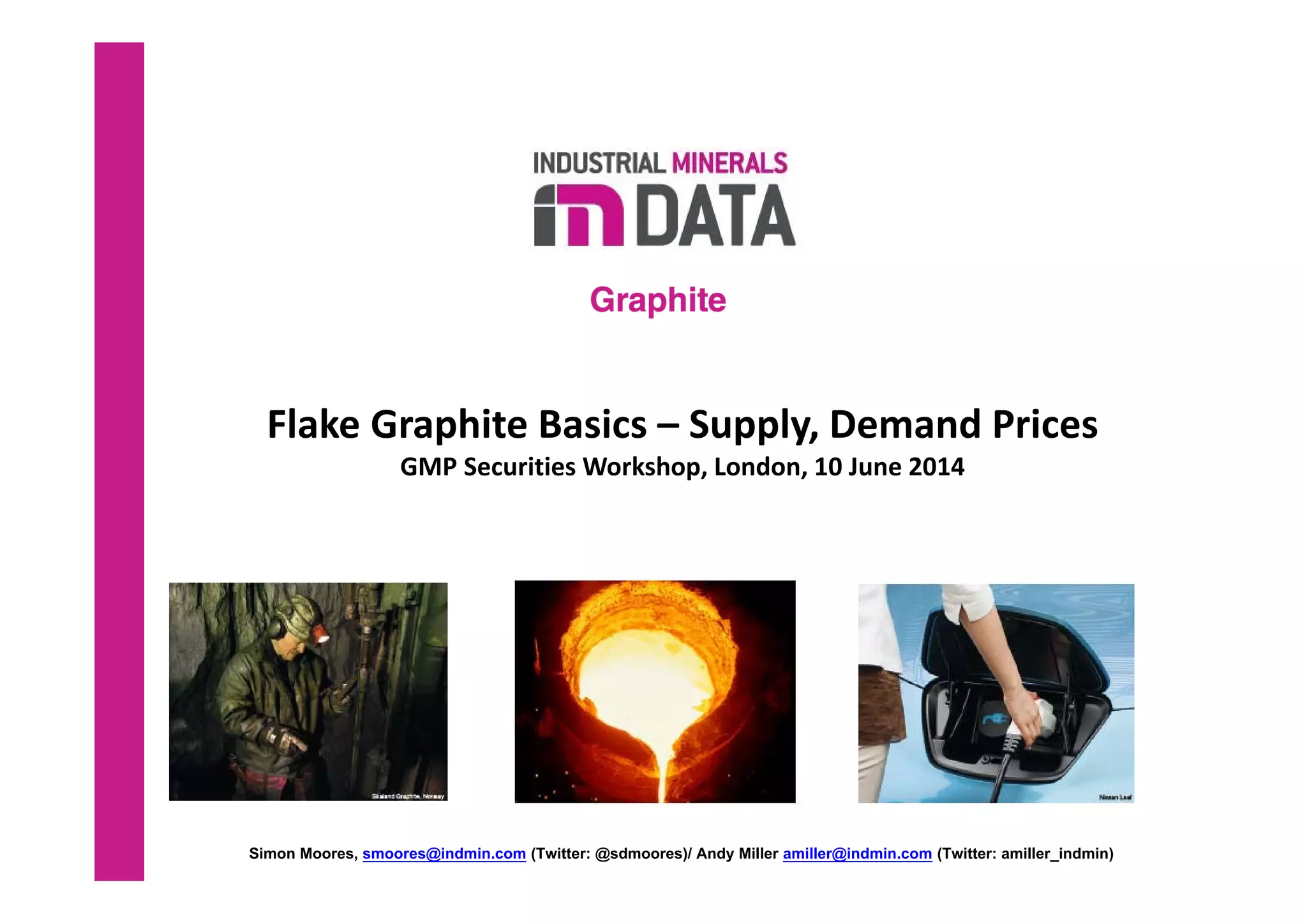

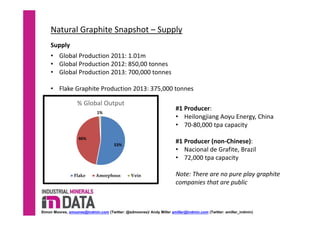

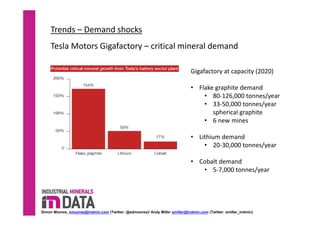

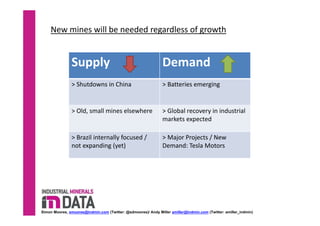

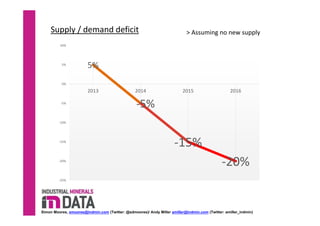

The document provides an overview of the supply and demand dynamics of natural graphite, highlighting production statistics, key producers, and price ranges. It discusses the challenges and trends in the industry, especially in relation to major markets such as refractories and batteries, and how developments like Tesla's gigafactory are affecting demand. Additionally, it notes significant supply risks due to China's consolidation efforts and the need for new mines to meet emerging demands.