4

Introduction

Private investmenthas become vital to the improvement of public infrastructure.

To meet public infrastructure goals, much of urban public investment must be financed through debt.

There is a concerted effort to shift urban infrastructure investment from the public sector to private sector

recognising the benefits of risk transfer to the private sector – namely improved value for money and accelerated

delivery of the infrastructure program as well as freeing resources for social investment e.g. schools, hospitals

etc.

Possible financing options are:

– Debt Capital Markets

– Export Credit Agency Finance

– Infrastructure & Energy (Project) Finance

– Structured Finance

For each of these financing options, we highlight the advantages and challenges related to the structure.

Citi is pleased to present this paper discussing financing alternatives to the public sector physical Infrastructure.

Introduction

5.

5

Overview of PublicSector Infrastructure Financing

Infrastructure is a core element of growth and development of any country, and this includes power plants, public

telecommunications systems, water purification projects, airports, railroads, toll roads and shipping terminals.

Historical underinvestment by government which has typically been the sole provider, growing populations,

urbanization, have made infrastructure a critical development agenda for Africa.

Challenges in meeting demand for new and/or upgraded infrastructure are not only in sourcing necessary funds,

but in the financial and project management capabilities of Local & State and Federal Governments, for which

they will require private sector assistance.

Huge global demand for capital to fund large-scale infrastructure projects is likely to ignite competition among

governments to attract private investment, therefore governments have an incentive to ensure the appropriate

enabling environment.

Introduction

6.

6

Financing Options Snapshot

Citihas extensive experience in structuring, coordinating and arranging optimal financial structures as well as

executing Debt Capital Markets, Export Credit Agency, Project, and Structured Solutions financings.

Debt Capital Markets financing:

• Very attractive yields coupled with flexible maturities ranging from 1.5

years up to 30+ years for the stronger credits.

• Together with the 2 segregated pools of US$ funds (domestic and

international), there exists a “global” market for large issues, which can be

sold simultaneously into both markets.

Export Credit Agency financing:

• Citi Export and Agency Finance Group (“EAF”) has experience in

arranging structured financings for and provides export financing advice

to Citi clients.

• ECA Financing provides a cost effective solution for infrastructure

construction and equipment & plant purchases.

• EAF arranges and participates globally in structured financings that

manage risk through credit and political risk arbitrage with sovereign

Agencies as well as local and international investors and insurers

Project (Infrastructure & Energy) Financing:

Citi has experience in advising, structuring, coordinating and arranging

infrastructure and energy projects financing and believes that Nigeria can

also utilize project financing to meet part of its financing requirements.

Infrastructure and Energy projects financing will enable Nigeria to tap the

infrastructure funds market on a fully inclusive basis as both conventional

and infrastructure funds participate in developing countries facilities

Structured Solutions:

• Citi’s Structured Solutions team has structured and placed multiple

infrastructure finance transactions. These include:

– Public-Private Partnerships in the provision of road infrastructure,

– financing of rail/light rail/underground projects,

– innovative financings of airports, and

– acquisition finance of predictable cash flow generating companies

using whole business securitization and structured bonds

Introduction

9

Debt Capital Markets

Definitions

What is a Bond? A piece of “paper” issued by a borrower constituting

and evidencing a debt obligation

What is a “Euro Bond”? A paper typically issued in the European

markets outside of an issuers domestic market

What is a “Global Bond”? A paper typically issued to the global markets,

including US and Europe, often including listing in more than one

jurisdiction

Key characteristics of eurobonds issued in the current market are:

Eurobonds are freely transferable

Lenders are anonymous

Protected from “domestic” tax law (could depend on country);

“Standard” terms and conditions typically offering less protection to

creditors than bank loans; and

Settlements and payments on eurobonds made through the clearing

systems (Euroclear and Clearstream)

Advantages of Eurobonds:

Deep and an efficient markets

Market standard documentation with limited disclosure

Flexibility of maturities

Attractive absolute low yields

Position credit story

Arguments for Issuing a Bond to fund Infrastructure Financing

Expose economic policies and political developments to market scrutiny

& provide a powerful platform for underscoring the message of progress

Supplement domestic savings

Diversify funding sources and confirm market access to funding

Provide at least one data point for estimating the risk premium that

should be applied when analyzing investment prospects

Increase the government’s flexibility in planning its budget compared with

exclusive reliance on official funding sources

Steps and Consideration for Issuance

Support of all stakeholders

Economic readiness and capacity to absorb the debt proceeds

productively

Build support from official donors and supranational lenders to ensure

this exercise is complementary to their programs and avoid reducing

access to concessionary funding in the future

Build investor base focus on the story

Address how the ratings compare to other similarly rated countries

Options which maximizes the sustainability of the repayment schedule

Seek two more ratings from Moody’s and Fitch

Financing Options – Debt Capital Markets

11

Export Credit Agency

Definitions

Export Credit Agencies (ECAs) are government agencies of the Organization for Economic Cooperation and Development (OECD) which promote

employment and growth in their home countries by encouraging exports of goods and services

ECAs guarantee bank finance, supplier finance, and/or provide direct loans, transforming usually non-investment grade borrowers to AAA-rated or

AA-rated assets

ECAs may also provide fixed interest rates via a variety of subsidies/swaps

ECAs work within an established set of guidelines called the OECD Consensus

ECAs provide their guarantees on up to 85% of the contract value of imported goods; the remaining 15% must be financed via equity or other debt

Fairly straight forward structures

Who uses Export Credit Agency

Any emerging market borrower with capital expenditure program

Private Companies, Project Finance/Greenfield, subsidiaries of

Multinationals, Local Companies, Public Sector Entities,

Governments

Key industries:

– Oil & gas and petrochemicals

– Aviation and shipping

– Power and telecoms

– Cement

– Transportation

– Infrastructure

Why use credit enhanced structures?

Increase amount and tenor of debt that can be raised

– Risk mitigation increases appetite from lenders

– Low capital allocation for lenders

Reduce cost of debt

– Premium plus interest margin is usually lower than a

‘clean’ loan

Best execution

– Public OECD government support

– ECA participation considered a plus for the ‘story’

Fixed interest rate option

International market standard terms and conditions

– Relatively simple documentation

Financing Options – Export Credit Agency

12.

12

Multilateral and BilateralInstitutions

EBRD and IFC B-Loans

Co-operation with leading Multilateral Agencies

(MLAs), IFC and EBRD to structure, arrange and

often underwrite A/B-loan financings

Lenders benefit from the MLAs’ preferred

creditor status

Local currency innovation

Multilateral agencies and other sponsors often provide insurance, guarantees or other forms of credit enhancement mechanisms such

as subordinated debt in order to make projects more attractive to investors or project lenders or investors. These credit enhancement

mechanisms help reduce and reallocate project risks among lenders and investors in order to make project more attractive.

Development Finance Institutions (DFIs)

Multilateral and Bilateral Agencies are useful providers of

financing and have a keen interest in projects in Emerging

Markets

Agencies can provide credit enhancement by way of partial

guarantees, in the same manner as provided by ECAs, but with

more flexibility in the structuring of the underlying instrument

Many of these agencies also provide direct funding through loans

Key advantage - support is “untied” to exports from a certain

country; hence can be used to finance capital expenditure,

including local capex

Major Multilaterals, Bilaterals & DFIs

Multilaterals

Bilaterals

Development Finance Institutions

Financing Options – Export Credit Agency

14

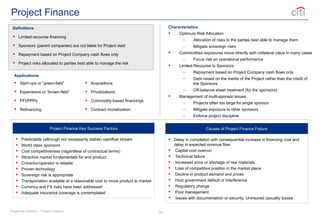

Project Finance

Definitions

Limitedrecourse financing

Sponsors (parent companies) are not liable for Project debt

Repayment based on Project Company cash flows only

Project risks allocated to parties best able to manage the risk

Characteristics

Optimum Risk Allocation

– Allocation of risks to the parties best able to manage them

– Mitigate sovereign risks

Commodities exposures move directly with collateral value in many cases

– Focus risk on operational performance

Limited Recourse to Sponsors

– Repayment based on Project Company cash flows only

– Debt raised on the merits of the Project rather than the credit of

the Sponsors

– Off-balance sheet treatment (for the sponsors)

Management of multi-sponsor issues

– Projects often too large for single sponsor

– Mitigate exposure to other sponsors

– Enforce project discipline

Applications

Start-ups or “green-field”

Expansions or “brown-field”

PFI/PPPs

Refinancing

Acquisitions

Privatizations

Commodity-based financings

Contract monetization

Project Finance Key Success Factors

Predictable (although not necessarily stable) cashflow stream

World class sponsors

Cost competitiveness (regardless of contractual terms)

Attractive market fundamentals for end product

Cntractor/operator is reliable

Proven technology

Sovereign risk is appropriate

Transportation available at a reasonable cost to move product to market

Currency and FX risks have been addressed

Adequate insurance coverage is contemplated

Causes of Project Finance Failure

Delay in completion with consequential increase in financing cost and

delay in expected revenue flow

Capital cost overrun

Technical failure

Increased price or shortage of raw materials

Loss of competitive position in the market place

Decline in product demand and prices

Host government default or interference

Regulatory change

Poor management

Issues with documentation or security, Uninsured casualty losses

Financing Options – Project Finance

15.

15

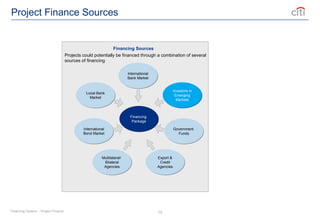

Project Finance Sources

FinancingSources

Local Bank

Market

Financing

Package

Export &

Credit

Agencies

International

Bond Market

International

Bank Market

Government

Funds

Multilateral/

Bilateral

Agencies

Investors in

Emerging

Markets

Projects could potentially be financed through a combination of several

sources of financing

Financing Options – Project Finance

17

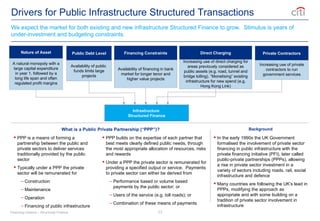

Drivers for PublicInfrastructure Structured Transactions

We expect the market for both existing and new infrastructure Structured Finance to grow. Stimulus is years of

under-investment and budgeting constraints.

A natural monopoly with a

large capital expenditure

in year 1, followed by a

long life span and often

regulated profit margins

Nature of Asset

Increasing use of direct charging for

areas previously considered as

public assets (e.g. road, tunnel and

bridge tolling). “Monetising” existing

infrastructure for new spend (e.g.

Hong Kong Link)

Direct Charging

Availability of public

funds limits large

projects

Public Debt Level

Increasing use of private

contractors to run

government services

Private Contractors

Availability of financing in bank

market for longer tenor and

higher value projects

Financing Constraints

Infrastructure

Structured Finance

What is a Public Private Partnership (“PPP”)? Background

PPP is a means of forming a

partnership between the public and

private sectors to deliver services

traditionally provided by the public

sector

Typically under a PPP the private

sector will be remunerated for

– Construction

– Maintenance

– Operation

– Financing of public infrastructure

PPP builds on the expertise of each partner that

best meets clearly defined public needs, through

the most appropriate allocation of resources, risks

and rewards

Under a PPP the private sector is remunerated for

providing a specified output or service. Payments

to private sector can either be derived from

– Performance based or volume based

payments by the public sector; or

– Users of the service (e.g. toll roads); or

– Combination of these means of payments

In the early 1990s the UK Government

formalised the involvement of private sector

financing in public infrastructure with the

private financing initiative (PFI), later called

public-private partnerships (PPPs), allowing

a rise in private sector investment in a

variety of sectors including roads, rail, social

infrastructure and defence

Many countries are following the UK’s lead in

PPPs, modifying the approach as

appropriate and with some building on a

tradition of private sector involvement in

infrastructure

Financing Options – Structured Finance

19

Conclusion

Private sectorforms a viable alternative to public sector infrastructure financing.

No single approach to addressing all infrastructure issues. Ideal sources of funding should be individually evaluated to determine

suitability for the project in mind.

Projects should be commercially viable and demonstrate sustainability over a period of time.

Important to structure a project from the beginning so that the roles and responsibilities of the partners are clearly defined and

accepted by everyone involved.

More than any other segment, public-sector clients require stable, ultra-efficient long-term financing solutions that can operate within

strict budgetary constraints – and under intense public scrutiny.

Social and economic benefits cannot be understated as infrastructure provides an enabling environment and catalyst for further

growth with power being arguably the most important at this time.

It is a collective responsibility and in the collective interest of financiers, governments and operators to arrive at workable solutions.

Conclusion

#1 Myself and role

Reason for giving presentation – inform about commodities and the group.

Reluctant speaker at best. Trader DNA – not slick sales

New presentation – tried to make more interesting. Test case. Will need polish and may be a bit patchy in places – you’ve been warned….