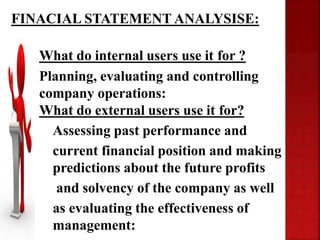

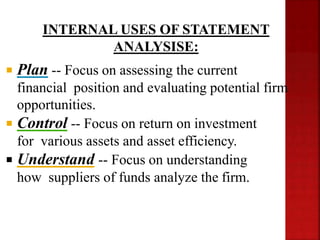

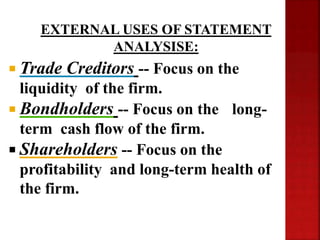

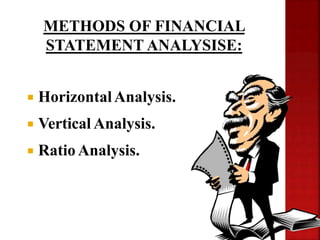

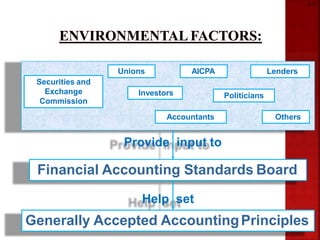

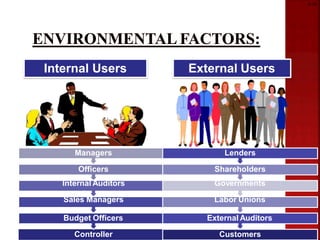

This document defines and discusses financial reporting and analysis. It begins by defining financial reporting as the financial results an organization releases publicly, which is a key function of the controller. Financial analysis is evaluating financial information for decision-making. The document then outlines the main types of financial statements used in reporting and analysis, which include the balance sheet, income statement, cash flow statement, and statement of retained earnings. It also discusses the internal and external uses of financial statement analysis and the main methods used, including horizontal analysis, vertical analysis, and ratio analysis.

![2-6

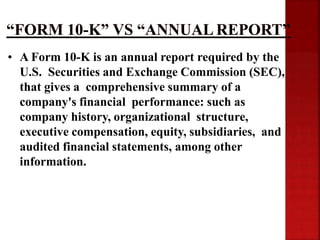

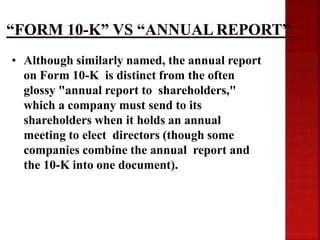

Form 10-K (Annual Report)

10-Q (Quarterly Report)

20-F (Registration Statement/ Annual Report

[Foreign])

8-K (Current Report)

14-A (Proxy Statement/Prospectus)

Other SEC Filings](https://image.slidesharecdn.com/afspptfinalzaman-221014061137-db98252c/85/Financial-Reporting-Analysis-Environment-By-Zaman-pptx-20-320.jpg)

![igcse 421702998-Acc2-Report [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/421702998-acc2-reportautosaved-251114165537-0a29fa9f-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Laila Kakar - Leveraging AI for Strategic Excellence: Enhanci...](https://cdn.slidesharecdn.com/ss_thumbnails/eykmhrtsqmaaftwkexh7-dsc-lailakakar-1-260119101520-5f3b5616-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Josip Saban - Career building for data professionals.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/zroflcttkm1vmli0txea-josip-saban-career-building-for-data-professionals-260123083019-587cdb8c-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Mikhail Rozhkov - AI Product Canvas: From Business Goals to T...](https://cdn.slidesharecdn.com/ss_thumbnails/d53doddtpgfqivmzqel6-mikhail-rozhkov-ai-product-canvas-v1-260121115910-9dd517a7-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Marcos Heidemann - Beyond the Hype: Making AI Coding Assistan...](https://cdn.slidesharecdn.com/ss_thumbnails/eexkhvldrjsopspdjbur-marcos-heidemann-beyond-the-hype-getting-real-value-out-of-ai-assisted-coding-260121115910-7e9d41ec-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Tali Fulman - Guild Meetings, Then What? Building Data Commun...](https://cdn.slidesharecdn.com/ss_thumbnails/fgohhi33rwmhqdowdj5k-tali-fulman-guild-meetings-then-what-building-data-communities-that-actually-ch-260120105855-528492c3-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Bojan Banjac - AI is always right when it comes to the matter...](https://cdn.slidesharecdn.com/ss_thumbnails/syoxtqierpydwxm5srcb-4-bojan-banjac-ai-is-always-right-when-it-comes-to-the-matters-of-taste-260119101519-694ee7d7-thumbnail.jpg?width=640&height=640&fit=bounds)