Downloaded 90 times

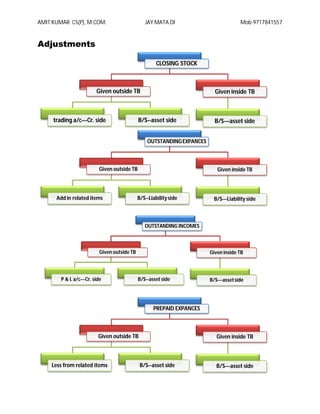

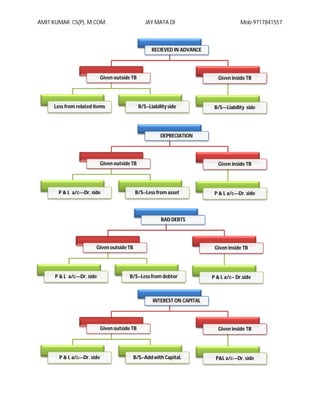

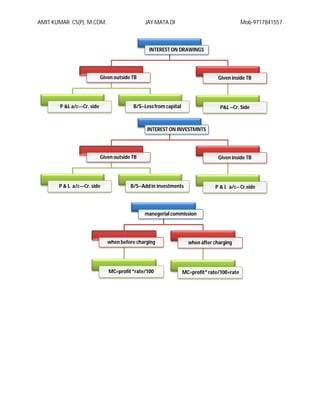

The document discusses various accounting adjustments that may be needed when preparing financial statements, such as adjusting closing stock, outstanding expenses, outstanding incomes, prepaid expenses, depreciation, bad debts, interest on capital, interest on drawings, interest on investments, and managerial commission. The adjustments are made either to asset, liability, or profit and loss accounts depending on whether they are given inside or outside the trial balance.