Download to read offline

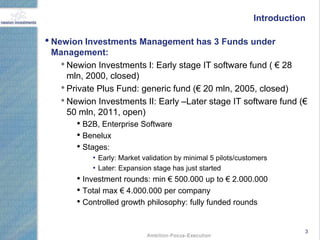

Newion Investments Management has three funds under management focused on early and later stage IT software companies in the Benelux region. The presentation outlines lessons learned from failures, including staying focused on building a sustainable company rather than quick exits, carefully planning acquisitions and integrations, and ensuring all shareholders remain aligned. Key takeaways emphasized understanding the business thoroughly, building minimal viable products, focusing on growth and proof over assumptions, and listening to intuition over being impressed by experts.