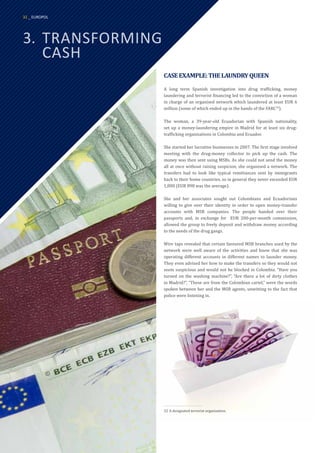

This document summarizes key questions around the use of cash, particularly by criminal groups for money laundering purposes. While cash usage is declining slightly for regular payments, the total value of euro banknotes in circulation continues to rise beyond inflation levels. A significant proportion of cash in circulation, including high denomination notes, is not used for payments and its purpose is unknown. Law enforcement investigations still find that cash remains the primary method for placing, layering and integrating illegal profits. Criminals use cash to facilitate money laundering as it allows them to conceal profits and maintain control over funds in an anonymous manner.

![Anti Money Laundering training [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/antimoneylaunderingautosaved-240728064239-49bf3fa4-thumbnail.jpg?width=640&height=640&fit=bounds)

![제 23회 보아즈(BOAZ) 빅데이터 컨퍼런스 - [MBOAX] : ABSA를 활용한 소비자 반응 분석 기반 운영 효율화 대시보드 설계](https://cdn.slidesharecdn.com/ss_thumbnails/3-1boaz23rdconferencemboax-260203102709-9d519923-thumbnail.jpg?width=640&height=640&fit=bounds)

![7.__Developing_a_Research_Proposal[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/7-260131073037-df92dd7d-thumbnail.jpg?width=640&height=640&fit=bounds)

![Hacking-Uncovered-How-People-Get-Hacked-and-How-to-Stay-Safe[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/hacking-uncovered-how-people-get-hacked-and-how-to-stay-safe1-260130170011-4883a9c7-thumbnail.jpg?width=640&height=640&fit=bounds)