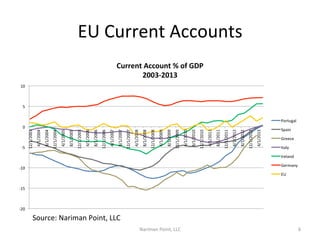

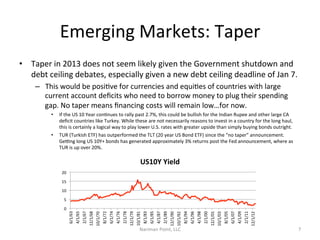

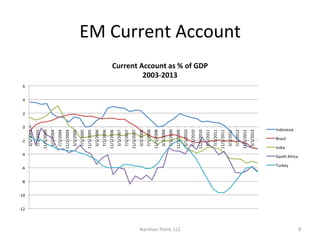

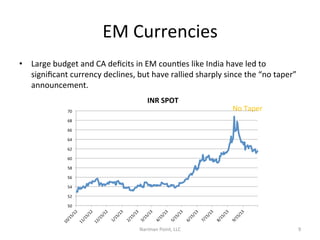

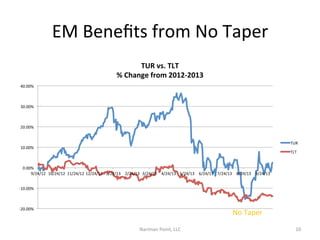

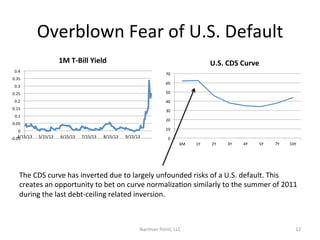

The report discusses ongoing U.S. government shutdown and debt ceiling negotiations with expectations for a resolution within 48 hours, alongside concerns about global economic impacts, particularly from European banks and Germany's economic policies. It highlights the strength of the euro, largely driven by Germany's contributions to the current account surplus, and the implications for emerging markets amid expectations of no tapering of U.S. monetary policy. The analysis suggests that markets remain stable despite political risks, with U.S. equities facing potential volatility based on earnings reports.