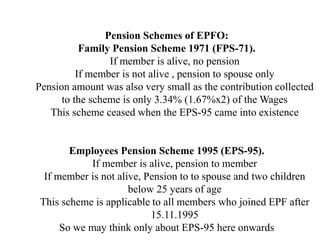

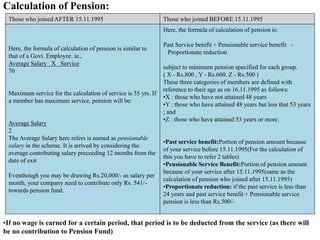

The document summarizes the pension schemes of the Employees' Provident Fund Organization (EPFO) in India. It discusses the Family Pension Scheme 1971 and the Employees Pension Scheme 1995. It provides details on how the pension is funded, the situations when pension can be applied for, how pension is calculated for those who joined before and after November 15, 1995, and options for commuting or capitalizing the pension. Key details covered include the funding source for pensions, eligibility criteria for receiving a pension, and formulas used to calculate pension amounts.

![Two Pension Capitalising Options are available:

1. Commutation

You can opt for commutation of pension and percentage of commutation. maximum% of

commutation is 33.33%. In this case, the pension will be reduced by 33.33% and you gets 100

times of commuted value as lump sum. eg. If original Pension is Rs.1000/-, if opted for 33.33%

commutation, the pension will be Rs. 667 and the lump sum amount is Rs. 333 x 100 = 33300.

The commutation will not cease and the original pension will not be restored.

If commuted, the pension after commutation will be taken as ORIGINAL Pension for the

calculation of lumpsum amounts related to Capital Return.

2. Capital Return

Three type of Capital Return Options are there:(The Capital Return Amounts are ADDITIONAL to

all other usual benefits)

Option No. 1 [under para 13(1)(1)]

If opted, 10% of pension

will be reduced. If original

Pension is Rs. 1000/-, you

get monthly pension of Rs.

900/-.

On Member Pensioner's

Death, Rs. 1000 x 100

(hundred times of pension)

as lump sum will be paid to

nominee (Nominee can be

anyone including spouse).

Widow pension & 2

Children Pension will be

paid as usual.](https://image.slidesharecdn.com/epsscheme1995495-230315093921-3c1d5df2/85/eps_scheme1995_495-ppt-4-320.jpg)

![Option No. 2 [under para 13(1)(2)]

If opted, 10% of pension

will be reduced. If

original Pension is Rs.

1000/-, you get monthly

pension of Rs. 900/-.

On Member Pensioner's

Death, 80% of pension

will be given to Widow

additional to her entitled

widow pension

and on the death or

remarriage of widow,

Rs. 1000 x 90 (ninety

times of pension) to

nominee as lump sum

(nominee can not be

spouse)

Widow pension & 2

Children Pension will be

paid as usual.

Option No. 3 [under para 13(1)(3)]

If opted, 12.5% of

pension will be reduced.

If original Pension is Rs.

1000/-, you get monthly

pension of Rs. 875/-.

This amount will be

paid for a fixed period

of 20 years only.

In case the member dies

before 20 years, the

pension will be paid to

his nominee for the

balance period.

On attaining this 20

years, Rs. 1000 x 100

(hundred times of

pension) will be given to

the member if he is

alive, otherwise to his

nominee.

Widow pension & 2

Children Pension will be

paid as usual.](https://image.slidesharecdn.com/epsscheme1995495-230315093921-3c1d5df2/85/eps_scheme1995_495-ppt-5-320.jpg)

![Talent Engine- Discussion Guide [Autosaved].ppt](https://cdn.slidesharecdn.com/ss_thumbnails/talentengine-discussionguideautosaved-230315094501-ba4f38ea-thumbnail.jpg?width=640&height=640&fit=bounds)