Download to read offline

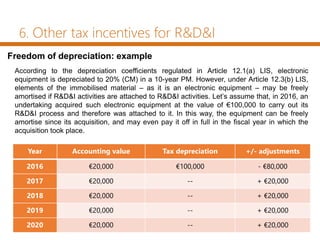

This document summarizes tax incentives for research and entrepreneurship in Spain. It discusses direct and indirect tax incentives for R&D, including a tax credit for R&D expenses up to 25% and the patent box regime which provides a 60% reduction in taxable income from certain intangible assets. The document also outlines other incentives like accelerated depreciation for R&D assets and a tax credit for entrepreneurs who invest in startups. Finally, it discusses an allowance for social security contributions for companies' research staff.

![[1999][r&d][eee extended engineeringenterprise]](https://cdn.slidesharecdn.com/ss_thumbnails/1999rdeeeextendedengineeringenterprise-130323071819-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)