- Ellen Kullman, CEO of DuPont, presented at the 30th Annual Sanford C. Bernstein Strategic Decisions Conference on May 28, 2014.

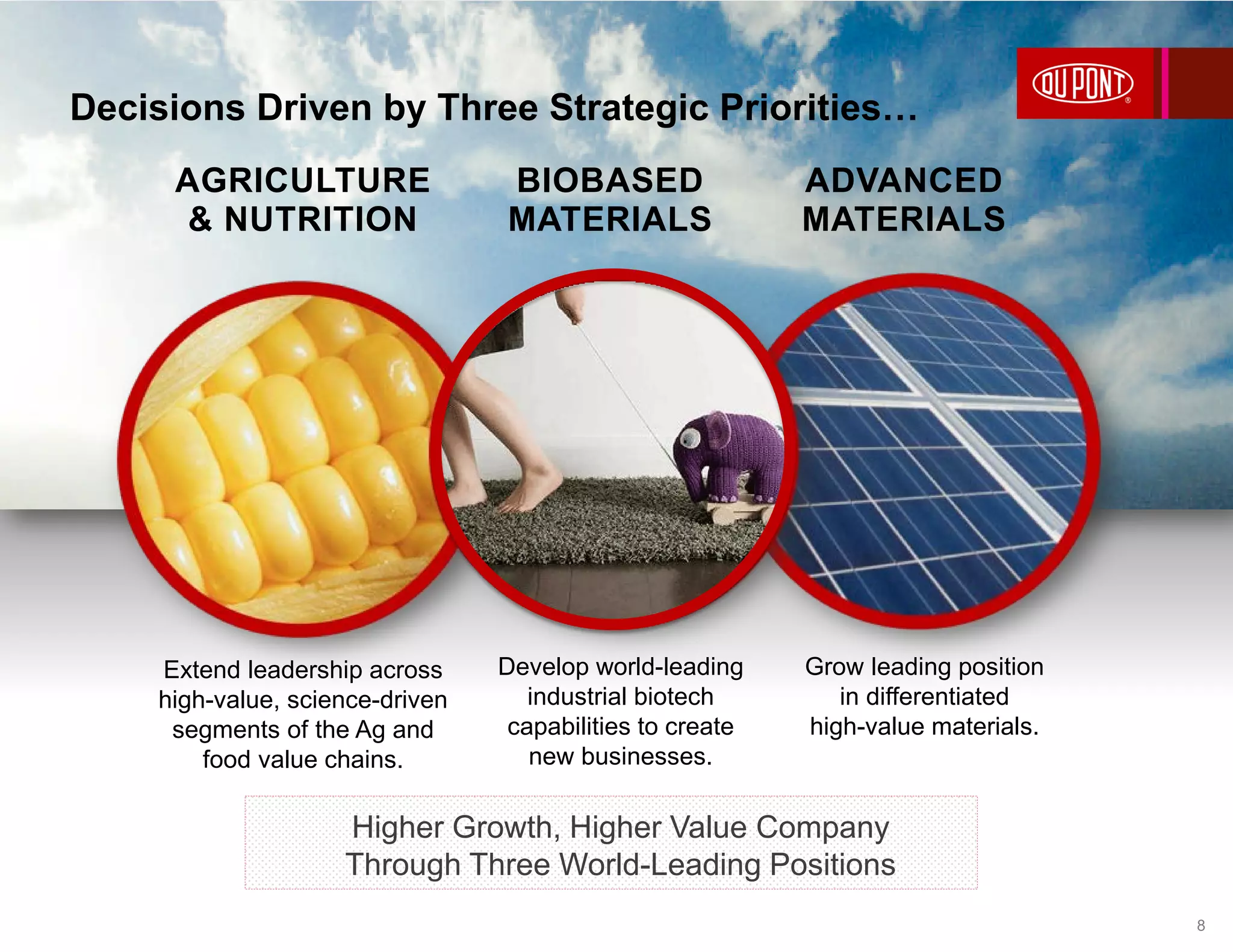

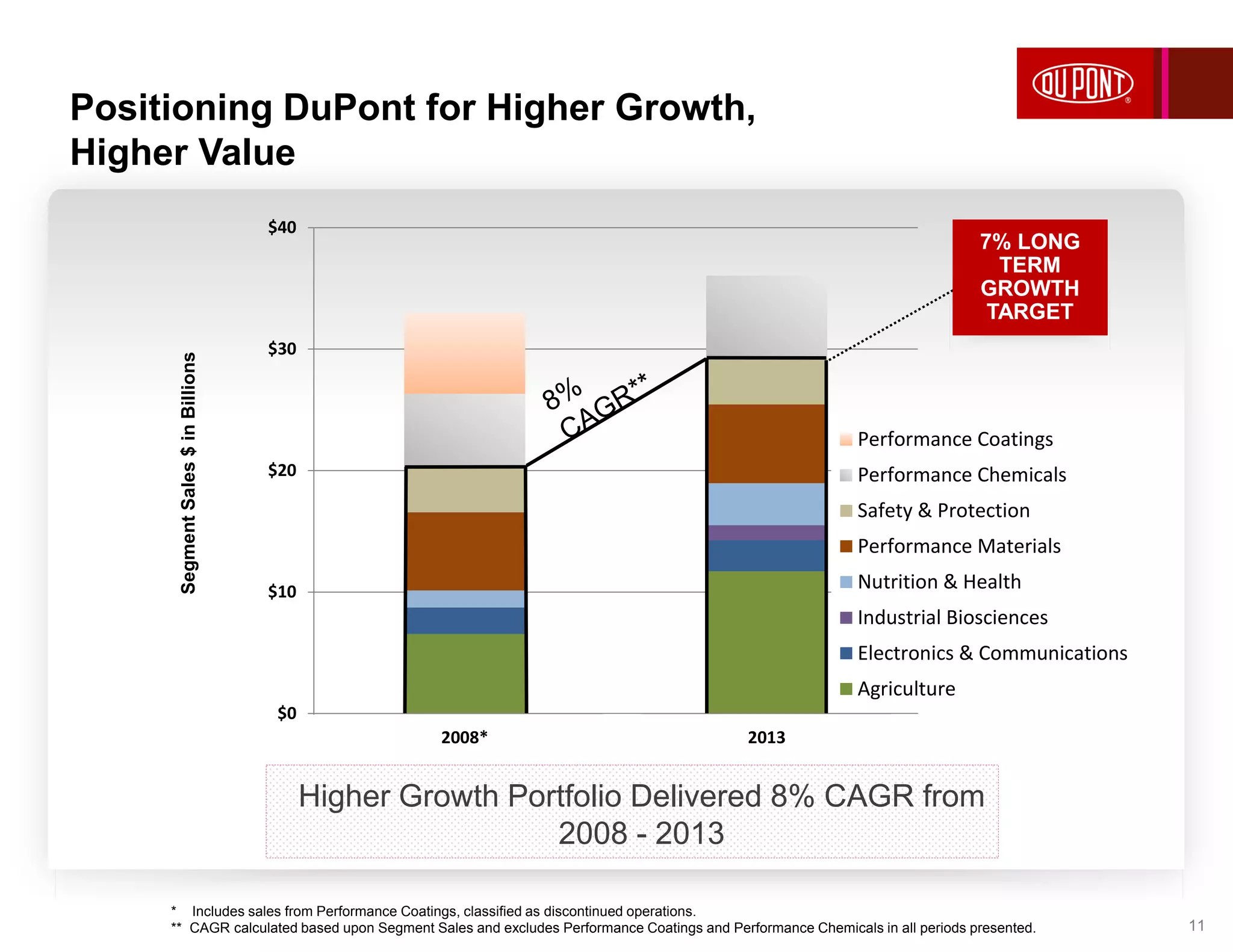

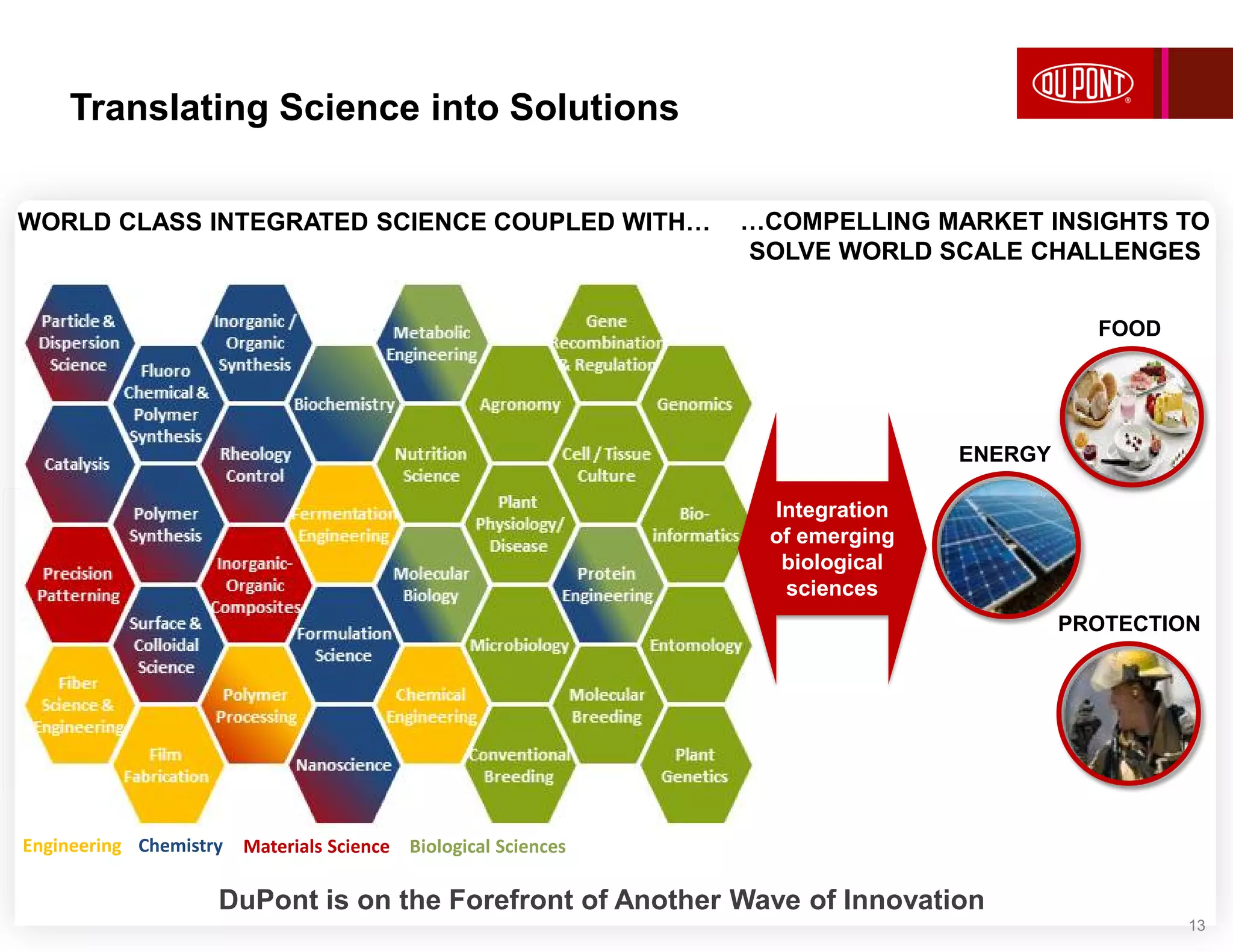

- She outlined DuPont's strategic priorities of extending leadership in agriculture and nutrition, developing biobased materials, and strengthening advanced materials to achieve 7% sales growth and 12% operating EPS growth.

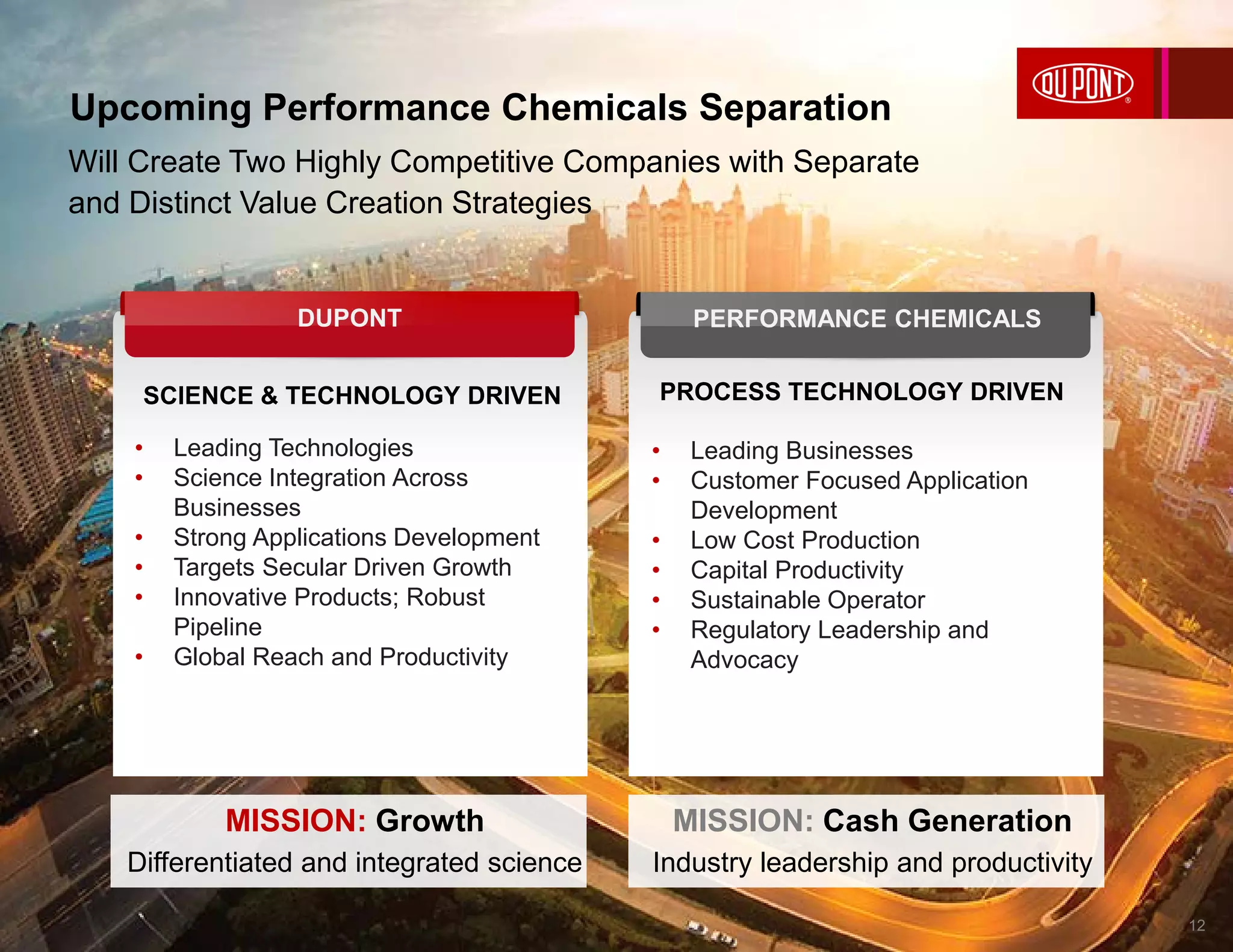

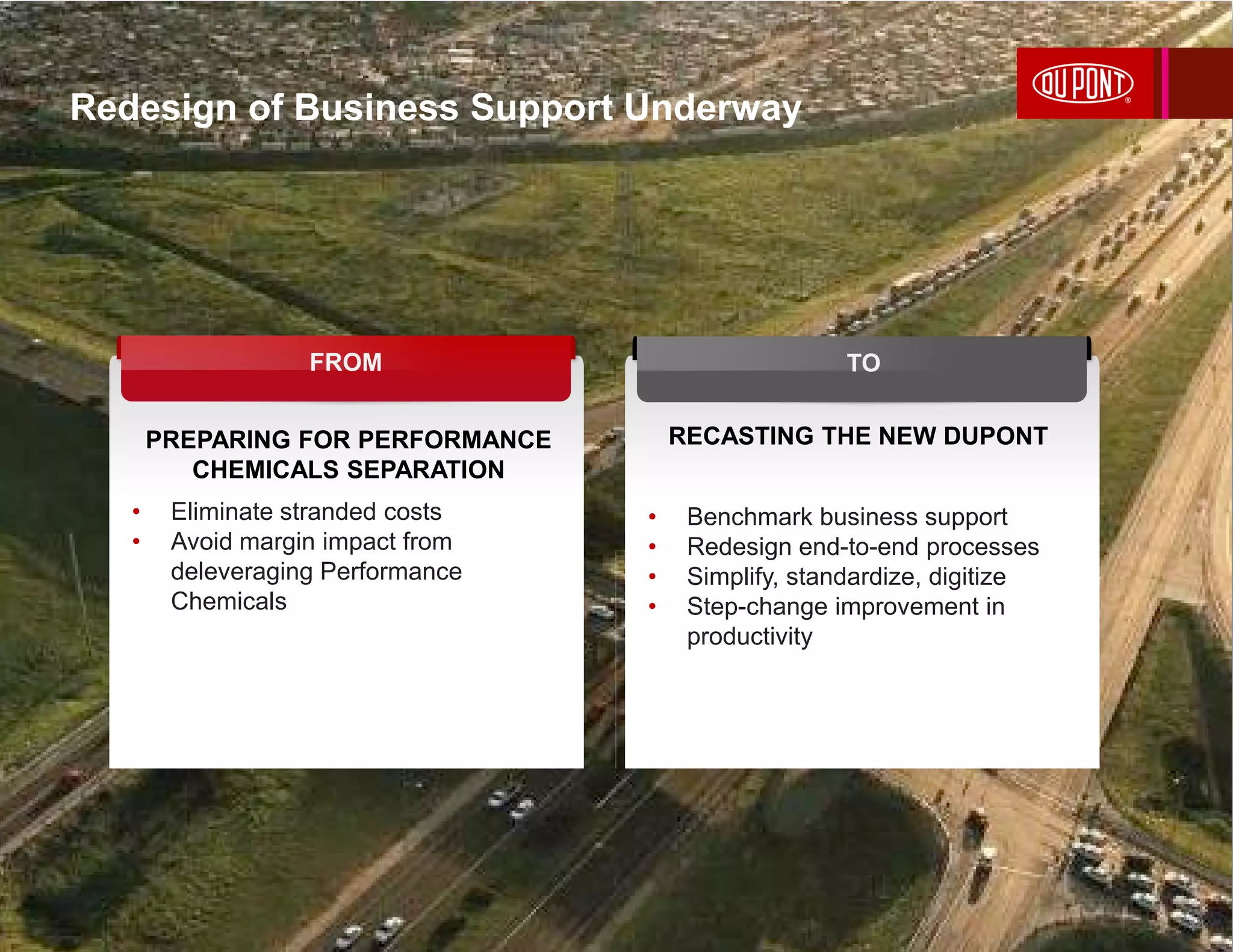

- DuPont is redesigning its business support processes and preparing to separate its Performance Chemicals segment to create two independent, focused companies pursuing different growth strategies.