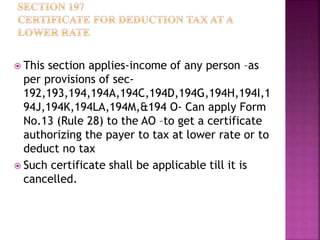

1) This section outlines the process for applying for a lower tax deduction certificate using Form 13. Such a certificate applies until cancelled.

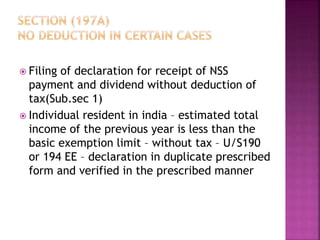

2) Individual residents in India whose estimated total income is less than the basic exemption limit can file a declaration in the prescribed form and manner to receive payments without tax deduction under Sections 190 or 194EE.

3) Filing a declaration in writing that the estimated total income for the previous year will be nil allows for non-deduction of tax under certain sections for persons other than companies and firms.

![Tds provisions [income tax act, 1961]](https://cdn.slidesharecdn.com/ss_thumbnails/tdsprovisionsincometaxact1961-140709044039-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)