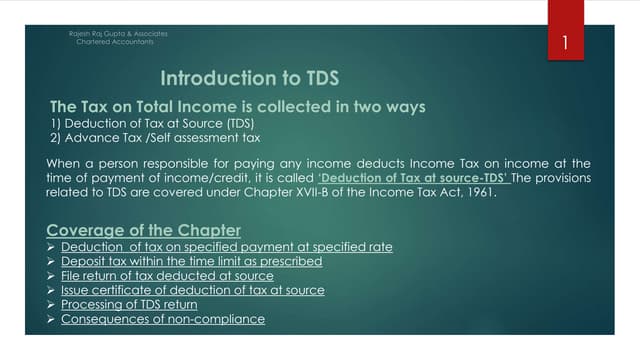

The document provides an overview of tax filings and compliance services related to TDS returns, ESI returns, and professional tax registration in India. It details the responsibilities of deductors and deductees, the different types of payments subject to TDS, applicable rates, and the consequences of late filing or non-filing. Additionally, it emphasizes the importance of timely compliance to avoid penalties and outlines the registration requirements for professional tax.

![Tds provisions [income tax act, 1961]](https://cdn.slidesharecdn.com/ss_thumbnails/tdsprovisionsincometaxact1961-140709044039-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)