Diam Infographic 2013

•

0 likes•126 views

May is Disability Insurance Awareness Month, a time when the insurance industry comes together to do something about the enormous gap that exists between Americans’ need for disability insurance and the actual coverage they have.

Report

Share

Report

Share

Download to read offline

Recommended

Insurance Secrets

The document discusses various types of liability insurance that nonprofits should consider purchasing, including general liability insurance, directors and officers liability insurance, professional liability insurance, and other specialized coverage. It provides details on what each type covers, differences between certificates of insurance and additional insureds, how to evaluate current coverage and risk management, and tips for selecting brokers and insurers.

Insurance Secrets

The document discusses various types of liability insurance that nonprofits should consider purchasing, including general liability insurance, directors and officers liability insurance, professional liability insurance, and other specialized coverages. It provides details on what each type covers, and recommends that nonprofits regularly evaluate their insurance needs, shop for better rates if their current coverage is too expensive or inadequate, and work with brokers to implement new insurance programs.

Principal Financial Slideshow Life Happens

This document discusses the importance of life insurance, especially during challenging economic times. It notes that many households admit they need more life insurance but may not purchase it. The document recommends having life insurance that is 7-10 times one's annual salary and provides an online calculator to help determine insurance needs. It closes by thanking the reader and providing contact information for further assistance.

The need for Disability

This document summarizes the need for disability insurance. It notes that one in five people will become disabled before age 65, yet many do not plan for this possibility. Disability insurance can replace lost income, which is important as over 40% of workers live paycheck to paycheck. While group disability insurance only costs around $218 per year on average, most employees do not have access to such coverage through their employers. This presents a risk if someone is unable to work due to disability.

Unsurance document bayzat

Get best health insurance policy in Dubai UAE with the help of Bayzat.com. Bayzat will help you out to keep awat from Unsurance.

Future Shock: The Retirement Loan Default Crisis

Attendees at the 2016 SPARK Forum heard from ERISA expert Tom Schendt (Alston & Bird) and CEO Tod Ruble (Custodia Financial) about three major reasons to implement simple, affordable protection against loan defaults and related cash outs in a 401(k) plan: 1) To reduce fiduciary risk, 2) To improve participant retirement outcomes, and 3) To increase plan assets. Click to view their presentation.

DI Assesment

The document is an assessment for disability insurance that encourages the reader to evaluate their need for coverage. It asks a series of questions about income dependence, likelihood of disability, and current insurance coverage. It then prompts the reader to calculate their potential monthly income shortage in the event of disability. The assessment emphasizes that disability is a real risk and that savings and existing coverage may not be sufficient to support living expenses if one is unable to work due to illness or injury. It encourages contacting an agent to review disability insurance options.

Who needs insurance preparation for the generations

This document provides insurance statistics by generation to help sales representatives discuss coverage needs with customers. It finds that a 35-year-old blue collar worker has a 34% chance of a long-term disability, and the average length is nearly 6 years. Most people will develop cancer or a chronic illness in their lifetime. The leading cause of death for Gen Xers and Millennials is unintentional injury. Many lack adequate emergency savings or life insurance to cover expenses, with Gen Xers having the largest coverage gap. Proper insurance can help prepare for unexpected disabilities, illnesses, or death.

Recommended

Insurance Secrets

The document discusses various types of liability insurance that nonprofits should consider purchasing, including general liability insurance, directors and officers liability insurance, professional liability insurance, and other specialized coverage. It provides details on what each type covers, differences between certificates of insurance and additional insureds, how to evaluate current coverage and risk management, and tips for selecting brokers and insurers.

Insurance Secrets

The document discusses various types of liability insurance that nonprofits should consider purchasing, including general liability insurance, directors and officers liability insurance, professional liability insurance, and other specialized coverages. It provides details on what each type covers, and recommends that nonprofits regularly evaluate their insurance needs, shop for better rates if their current coverage is too expensive or inadequate, and work with brokers to implement new insurance programs.

Principal Financial Slideshow Life Happens

This document discusses the importance of life insurance, especially during challenging economic times. It notes that many households admit they need more life insurance but may not purchase it. The document recommends having life insurance that is 7-10 times one's annual salary and provides an online calculator to help determine insurance needs. It closes by thanking the reader and providing contact information for further assistance.

The need for Disability

This document summarizes the need for disability insurance. It notes that one in five people will become disabled before age 65, yet many do not plan for this possibility. Disability insurance can replace lost income, which is important as over 40% of workers live paycheck to paycheck. While group disability insurance only costs around $218 per year on average, most employees do not have access to such coverage through their employers. This presents a risk if someone is unable to work due to disability.

Unsurance document bayzat

Get best health insurance policy in Dubai UAE with the help of Bayzat.com. Bayzat will help you out to keep awat from Unsurance.

Future Shock: The Retirement Loan Default Crisis

Attendees at the 2016 SPARK Forum heard from ERISA expert Tom Schendt (Alston & Bird) and CEO Tod Ruble (Custodia Financial) about three major reasons to implement simple, affordable protection against loan defaults and related cash outs in a 401(k) plan: 1) To reduce fiduciary risk, 2) To improve participant retirement outcomes, and 3) To increase plan assets. Click to view their presentation.

DI Assesment

The document is an assessment for disability insurance that encourages the reader to evaluate their need for coverage. It asks a series of questions about income dependence, likelihood of disability, and current insurance coverage. It then prompts the reader to calculate their potential monthly income shortage in the event of disability. The assessment emphasizes that disability is a real risk and that savings and existing coverage may not be sufficient to support living expenses if one is unable to work due to illness or injury. It encourages contacting an agent to review disability insurance options.

Who needs insurance preparation for the generations

This document provides insurance statistics by generation to help sales representatives discuss coverage needs with customers. It finds that a 35-year-old blue collar worker has a 34% chance of a long-term disability, and the average length is nearly 6 years. Most people will develop cancer or a chronic illness in their lifetime. The leading cause of death for Gen Xers and Millennials is unintentional injury. Many lack adequate emergency savings or life insurance to cover expenses, with Gen Xers having the largest coverage gap. Proper insurance can help prepare for unexpected disabilities, illnesses, or death.

Ten Tips for Safe Summer Barbecues: Learn the Dos and Don'ts of Grilling

1) The document provides 10 tips for safely using backyard barbecue grills, with 7,000 Americans injured each year from misusing grills.

2) Key safety tips include keeping grills at least 10 feet from any structure, cleaning grills regularly to prevent grease buildup and fires, and checking gas hoses and connections for leaks.

3) Dangerous practices to avoid are turning on gas with the lid closed, leaving grills unattended as fires double in size every minute, and using grills indoors which poses fire and carbon monoxide hazards.

Prysmian Metering Link Disconnect Box & Mini Pillar

This document describes a metering link disconnect box and mini pillar product that allows independent distribution network operators to connect to distribution network operator networks and monitor private network power consumption. The product consists of an underground metering link disconnect box connected to a surface-mounted mini pillar. Key components include link chambers, fuse carriers, current transformers, and pre-wired connections. The product has undergone electrical and component testing and is patented for use as a DNO/IDNO linking disconnecting unit.

Essay

The document compares and contrasts the science fiction films The Hunger Games and Divergent. Both are based on popular young adult novels and feature teenage female protagonists, but have different plots, characters, and themes. The Hunger Games is set in a dystopian future where young people must fight to the death on television. Katniss volunteers to take her sister's place. Divergent takes place in a society divided into factions; Beatrice discovers she is Divergent and does not fit into one group. While both depict dystopian futures, The Hunger Games focuses on violence and inequality, while Divergent's theme is identity and choice. Overall, the document analyzes the similarities and differences between the two

Uso del portafolio 2 (1)

El documento describe los portafolios como una colección de documentos que muestran el progreso y logros de un estudiante. Los portafolios permiten al profesor y al estudiante monitorear el aprendizaje y realizar cambios. También permiten evaluar las habilidades y logros de los estudiantes a través de cómo piensan, analizan y crean. Los estudiantes pueden participar en la selección de contenidos y criterios de evaluación de su propio trabajo.

Yue the pearl

Kino, Juana, and their baby Coyotito lived in a small village in Mexico. One day, Coyotito was stung by a scorpion and became ill. Kino took Coyotito to the doctor, who treated the baby by putting white powder in his mouth.

Identidad latinoamerica

Este documento discute la identidad latinoamericana desde dos perspectivas: histórico-cultural y psicológica. Desde la perspectiva histórico-cultural, la identidad latinoamericana fue determinada principalmente por la herencia española, incluyendo la religión católica, el idioma español, la historia común y el urbanismo. La perspectiva psicológica enfatiza el mestizaje resultante de la mezcla de culturas indígenas, españolas y africanas, el cual se refleja en la

Advantages & disadvantages of social networkings

This document lists and compares the advantages and disadvantages of using social media platforms like Facebook and Twitter. Some key advantages mentioned include staying connected with others, sharing content easily, and using social media for business purposes. However, the document also notes potential disadvantages such as privacy issues, overuse leading to addiction, fake profiles, and performance problems. Both Facebook and Twitter are assessed as generally easy to use but raising concerns around privacy controls and anonymous or fake accounts.

Life and Disability White Paper (1)

This document discusses the importance of life and disability insurance. It begins by noting that many employees are underinsured or lack insurance, leaving them vulnerable if the primary wage earner dies or becomes disabled. Specifically, only around half of workers have short or long-term disability coverage, and 41% of adults lack any life insurance. It then examines reasons for this, such as financial priorities, lack of knowledge, and procrastination. The document emphasizes that disability is more common than most people assume, with a 33% chance of a 6-month disability, and that disabilities usually stem from common illnesses not covered by workers' compensation. Finally, it notes the high financial toll of disabilities, with costs potentially totaling around $1 million

Ovation - Services & Supplemental

Brief slide show on Ovation's services with a focus on the need for supplemental insurance - like Aflac, Assurant, or Colonial.

Future Assist EBook Insurance

This document provides an overview of different types of personal insurance products and tips to help avoid common mistakes. It discusses life insurance, total and permanent disability insurance, income protection insurance, trauma insurance, and business expenses insurance. It emphasizes the importance of having adequate insurance coverage to protect your family's livelihood in case of illness, injury, or death. It warns against direct marketing insurance due to higher costs, lack of features, and uncertainty of payouts. It recommends seeking independent financial advice to help determine the right insurance coverage tailored to individual needs and circumstances.

Life and Disability Insurance: What 20-and-30 Somethings Think.

Young adults understand the importance of life and disability insurance but have gaps in their knowledge about different types of policies. Many do not fully understand their own coverage or their partner's coverage. While they want insurance to provide for things like debts, mortgages, and dependents' expenses if something were to happen to them, the reality is that many are likely underinsured due to a lack of understanding about their policies. Younger generations value protecting their earning potential but have not taken full steps to do so through insurance.

Dignity For Life

1. Long term care insurance pays for long term care services such as help with daily activities like eating, bathing, and dressing. It can cover care at home or in facilities like nursing homes.

2. Some key things to know before buying long term care insurance are getting the right amount of coverage, choosing a company unlikely to raise premiums, understanding rejection doesn't mean you can never get coverage, and getting advice from a specialist.

3. Long term care is an important issue for women as they are often caregivers, live longer, and make up a large portion of nursing home residents.

Voluntary Disability

The document discusses voluntary disability insurance and its benefits. It notes that disability causes nearly 50% of mortgage foreclosures compared to 2% from death. It also states that group voluntary long-term disability insurance through an employer provides affordable protection for employees and growth opportunities for insurance providers. The annual premium for group voluntary LTD through Assurant Employee Benefits is on average $321, much lower than the $1,856 average for individual LTD policies.

Group Voluntary Disability

The document discusses the risks of disability and importance of disability insurance. Some key points:

- 12% of Americans suffer long-term disabilities each year, and the chances of becoming disabled by age 35 are 50%

- Most disabilities (64%) are not work-related and therefore not covered by workers' compensation

- Losing income due to disability is a major risk, as it could result in losing one's home or draining savings within a year

- Group voluntary disability insurance can provide an affordable way to protect one's income through tax-free benefits and guaranteed acceptance during open enrollment periods.

Protection Strategies

The document discusses the importance of protecting your family's financial security through life insurance, disability insurance, and long-term care insurance. It notes that your future earnings are typically your most valuable asset but can be at risk if you die prematurely, become disabled, or require long-term care. It highlights that many families are underinsured for these risks. The document urges planning now to choose appropriate insurance coverage to safeguard your loved ones' financial well-being and independence.

How Can I Qualify for Maryland Medicaid

Medicaid is a government health insurance program that can become quite important to people who were never poor, because it pays for long-term care. The Medicare program will not pay for custodial care. Learn more about Maryland medicaid in this presentation.

Disability Income Insurance

The document discusses the importance of disability income insurance. It notes that the probability of becoming disabled before age 65 is quite high. It also discusses how most disabilities are caused by illness rather than accidents. The document emphasizes that disability insurance can help replace lost income that results from being unable to work due to injury or illness. It highlights some limitations of relying solely on savings, employer-provided insurance, Social Security, or workers compensation.

Kfs disability 2

The document discusses the importance of disability income planning and insurance. It notes that most people do not realize how much income they are expected to earn over their careers. It then highlights the risks of disability and average durations. The rest of the document provides examples of sources of funds during a disability, and suggests that disability income insurance can help replace income and maintain lifestyle. It includes a checklist for evaluating disability income policy features and benefits. The final pages provide a disability income action plan.

More Related Content

Viewers also liked

Ten Tips for Safe Summer Barbecues: Learn the Dos and Don'ts of Grilling

1) The document provides 10 tips for safely using backyard barbecue grills, with 7,000 Americans injured each year from misusing grills.

2) Key safety tips include keeping grills at least 10 feet from any structure, cleaning grills regularly to prevent grease buildup and fires, and checking gas hoses and connections for leaks.

3) Dangerous practices to avoid are turning on gas with the lid closed, leaving grills unattended as fires double in size every minute, and using grills indoors which poses fire and carbon monoxide hazards.

Prysmian Metering Link Disconnect Box & Mini Pillar

This document describes a metering link disconnect box and mini pillar product that allows independent distribution network operators to connect to distribution network operator networks and monitor private network power consumption. The product consists of an underground metering link disconnect box connected to a surface-mounted mini pillar. Key components include link chambers, fuse carriers, current transformers, and pre-wired connections. The product has undergone electrical and component testing and is patented for use as a DNO/IDNO linking disconnecting unit.

Essay

The document compares and contrasts the science fiction films The Hunger Games and Divergent. Both are based on popular young adult novels and feature teenage female protagonists, but have different plots, characters, and themes. The Hunger Games is set in a dystopian future where young people must fight to the death on television. Katniss volunteers to take her sister's place. Divergent takes place in a society divided into factions; Beatrice discovers she is Divergent and does not fit into one group. While both depict dystopian futures, The Hunger Games focuses on violence and inequality, while Divergent's theme is identity and choice. Overall, the document analyzes the similarities and differences between the two

Uso del portafolio 2 (1)

El documento describe los portafolios como una colección de documentos que muestran el progreso y logros de un estudiante. Los portafolios permiten al profesor y al estudiante monitorear el aprendizaje y realizar cambios. También permiten evaluar las habilidades y logros de los estudiantes a través de cómo piensan, analizan y crean. Los estudiantes pueden participar en la selección de contenidos y criterios de evaluación de su propio trabajo.

Yue the pearl

Kino, Juana, and their baby Coyotito lived in a small village in Mexico. One day, Coyotito was stung by a scorpion and became ill. Kino took Coyotito to the doctor, who treated the baby by putting white powder in his mouth.

Identidad latinoamerica

Este documento discute la identidad latinoamericana desde dos perspectivas: histórico-cultural y psicológica. Desde la perspectiva histórico-cultural, la identidad latinoamericana fue determinada principalmente por la herencia española, incluyendo la religión católica, el idioma español, la historia común y el urbanismo. La perspectiva psicológica enfatiza el mestizaje resultante de la mezcla de culturas indígenas, españolas y africanas, el cual se refleja en la

Advantages & disadvantages of social networkings

This document lists and compares the advantages and disadvantages of using social media platforms like Facebook and Twitter. Some key advantages mentioned include staying connected with others, sharing content easily, and using social media for business purposes. However, the document also notes potential disadvantages such as privacy issues, overuse leading to addiction, fake profiles, and performance problems. Both Facebook and Twitter are assessed as generally easy to use but raising concerns around privacy controls and anonymous or fake accounts.

Viewers also liked (11)

Ten Tips for Safe Summer Barbecues: Learn the Dos and Don'ts of Grilling

Ten Tips for Safe Summer Barbecues: Learn the Dos and Don'ts of Grilling

Prysmian Metering Link Disconnect Box & Mini Pillar

Prysmian Metering Link Disconnect Box & Mini Pillar

Similar to Diam Infographic 2013

Life and Disability White Paper (1)

This document discusses the importance of life and disability insurance. It begins by noting that many employees are underinsured or lack insurance, leaving them vulnerable if the primary wage earner dies or becomes disabled. Specifically, only around half of workers have short or long-term disability coverage, and 41% of adults lack any life insurance. It then examines reasons for this, such as financial priorities, lack of knowledge, and procrastination. The document emphasizes that disability is more common than most people assume, with a 33% chance of a 6-month disability, and that disabilities usually stem from common illnesses not covered by workers' compensation. Finally, it notes the high financial toll of disabilities, with costs potentially totaling around $1 million

Ovation - Services & Supplemental

Brief slide show on Ovation's services with a focus on the need for supplemental insurance - like Aflac, Assurant, or Colonial.

Future Assist EBook Insurance

This document provides an overview of different types of personal insurance products and tips to help avoid common mistakes. It discusses life insurance, total and permanent disability insurance, income protection insurance, trauma insurance, and business expenses insurance. It emphasizes the importance of having adequate insurance coverage to protect your family's livelihood in case of illness, injury, or death. It warns against direct marketing insurance due to higher costs, lack of features, and uncertainty of payouts. It recommends seeking independent financial advice to help determine the right insurance coverage tailored to individual needs and circumstances.

Life and Disability Insurance: What 20-and-30 Somethings Think.

Young adults understand the importance of life and disability insurance but have gaps in their knowledge about different types of policies. Many do not fully understand their own coverage or their partner's coverage. While they want insurance to provide for things like debts, mortgages, and dependents' expenses if something were to happen to them, the reality is that many are likely underinsured due to a lack of understanding about their policies. Younger generations value protecting their earning potential but have not taken full steps to do so through insurance.

Dignity For Life

1. Long term care insurance pays for long term care services such as help with daily activities like eating, bathing, and dressing. It can cover care at home or in facilities like nursing homes.

2. Some key things to know before buying long term care insurance are getting the right amount of coverage, choosing a company unlikely to raise premiums, understanding rejection doesn't mean you can never get coverage, and getting advice from a specialist.

3. Long term care is an important issue for women as they are often caregivers, live longer, and make up a large portion of nursing home residents.

Voluntary Disability

The document discusses voluntary disability insurance and its benefits. It notes that disability causes nearly 50% of mortgage foreclosures compared to 2% from death. It also states that group voluntary long-term disability insurance through an employer provides affordable protection for employees and growth opportunities for insurance providers. The annual premium for group voluntary LTD through Assurant Employee Benefits is on average $321, much lower than the $1,856 average for individual LTD policies.

Group Voluntary Disability

The document discusses the risks of disability and importance of disability insurance. Some key points:

- 12% of Americans suffer long-term disabilities each year, and the chances of becoming disabled by age 35 are 50%

- Most disabilities (64%) are not work-related and therefore not covered by workers' compensation

- Losing income due to disability is a major risk, as it could result in losing one's home or draining savings within a year

- Group voluntary disability insurance can provide an affordable way to protect one's income through tax-free benefits and guaranteed acceptance during open enrollment periods.

Protection Strategies

The document discusses the importance of protecting your family's financial security through life insurance, disability insurance, and long-term care insurance. It notes that your future earnings are typically your most valuable asset but can be at risk if you die prematurely, become disabled, or require long-term care. It highlights that many families are underinsured for these risks. The document urges planning now to choose appropriate insurance coverage to safeguard your loved ones' financial well-being and independence.

How Can I Qualify for Maryland Medicaid

Medicaid is a government health insurance program that can become quite important to people who were never poor, because it pays for long-term care. The Medicare program will not pay for custodial care. Learn more about Maryland medicaid in this presentation.

Disability Income Insurance

The document discusses the importance of disability income insurance. It notes that the probability of becoming disabled before age 65 is quite high. It also discusses how most disabilities are caused by illness rather than accidents. The document emphasizes that disability insurance can help replace lost income that results from being unable to work due to injury or illness. It highlights some limitations of relying solely on savings, employer-provided insurance, Social Security, or workers compensation.

Kfs disability 2

The document discusses the importance of disability income planning and insurance. It notes that most people do not realize how much income they are expected to earn over their careers. It then highlights the risks of disability and average durations. The rest of the document provides examples of sources of funds during a disability, and suggests that disability income insurance can help replace income and maintain lifestyle. It includes a checklist for evaluating disability income policy features and benefits. The final pages provide a disability income action plan.

Protecting your income

Income protection is for everyone. If you’re earning an income and can’t afford to retire tomorrow, you need disability insurance. Contact me today.

NEW PPT 3.18.2015 FINAL

Most of the country's retirement savings are held in banks, precious metals, real estate, stocks, and retirement accounts like IRAs and 401(k)s. However, a large percentage of these savings could be lost due to risks, fees, and taxes. Additionally, most consumers do not understand how these three factors—risks, fees, and taxes—affect their retirement accounts. Freedom Equity Group presents an alternative strategy that aims to protect retirement savings from these potential losses.

5 Insurance-Buying Mistakes to Avoid

Buying insurance can be confusing, but when the unexpected happens – a house fire, a fender bender or a broken bone – it's a relief to know that some of those financial losses will be covered. But how do you know how much coverage you need? And what questions should you ask before buying a policy? Many consumers aren't sure. Insurance coverage is far from one size fits all, so here's a look at mistakes some consumers make when buying insurance.

More info:

https://foursquare.com/westhillconsult

http://westhillconsultinginsurance.tumblr.com/

Are Your Assets Protected Hany Salib

The document discusses the importance of protecting one's assets and income through insurance policies. It notes that only about 10% of the working population has income protection and over a third of Australians risk becoming disabled for over 3 months before retirement. Various types of insurance like income protection, critical illness coverage, life insurance, and trauma insurance are presented as ways to financially protect oneself and one's family from risks relating to health issues, death, or disability. The document advocates lessening the financial impact of such risks through insurance rather than taking on the risks oneself.

Does Medicare Pay for Long-Term Care in New York

Medicare does not pay for long-term custodial care like that received in nursing homes. Such care can cost over $160,000 per year in New York. While Medicare helps with medical costs, 7 in 10 seniors will require long-term care assistance that Medicare does not cover. Medicaid may pay for long-term care for those with limited assets who qualify through a spend-down process. Planning is needed to qualify for Medicaid assistance with long-term care costs that Medicare does not cover.

Is No Exam Life Insurance For You?

No exam life insurance policies provide coverage without a medical exam, though applicants must answer health questions. Term policies offer up to $250,000 coverage for a limited time, while whole life policies provide lifetime coverage up to $40,000. Guaranteed issue policies offer up to $10,000 forever but only refund premiums initially. An independent agent can help applicants choose the best no exam option and obtain the most competitive quote based on their needs and health profile.

Disability Benefits Attorneys

Most of us believe in the saying that ‘work is life’. To a great extent this statement stands valid. We work in order to survive and derive the basic necessities of our lives.

What does it mean to protect your family?

In life insurance, you insure yourself to protect your loved ones. It's as if by putting on a helmet yourself, your child would be safe if he or she fell off the bike. It sounds illogical and yet it's not only true but it's very effective!

You probably guessed it, but your life insurance will pay a death benefit when you're gone. So you'll never really benefit from it. Instead, your spouse, children, parents or loved ones will be the real people protected by your life insurance. Since they would be the people most affected by your death, they are the ones you really protect by taking out your insurance.

WHITE PAPER: The Real Story About Life Settlements

The truth is that life settlements are simply another powerful

tool in an advisor’s toolbox. They can be used skillfully to put

a client’s money in motion, helping create important liquidity events for them. Research from the London Business School indicates that life settlements provide an average of four times as much money as the cash surrender value offered by insurers.1 In cases where a client risks defaulting on his or her life insurance premiums, life settlements can be a way to find benefit in a policy that has become burdensome.

Similar to Diam Infographic 2013 (20)

Life and Disability Insurance: What 20-and-30 Somethings Think.

Life and Disability Insurance: What 20-and-30 Somethings Think.

WHITE PAPER: The Real Story About Life Settlements

WHITE PAPER: The Real Story About Life Settlements

Recently uploaded

Independent Study - College of Wooster Research (2023-2024) FDI, Culture, Glo...

Independent Study - College of Wooster Research (2023-2024) FDI, Culture, Glo...AntoniaOwensDetwiler

"Does Foreign Direct Investment Negatively Affect Preservation of Culture in the Global South? Case Studies in Thailand and Cambodia."

Do elements of globalization, such as Foreign Direct Investment (FDI), negatively affect the ability of countries in the Global South to preserve their culture? This research aims to answer this question by employing a cross-sectional comparative case study analysis utilizing methods of difference. Thailand and Cambodia are compared as they are in the same region and have a similar culture. The metric of difference between Thailand and Cambodia is their ability to preserve their culture. This ability is operationalized by their respective attitudes towards FDI; Thailand imposes stringent regulations and limitations on FDI while Cambodia does not hesitate to accept most FDI and imposes fewer limitations. The evidence from this study suggests that FDI from globally influential countries with high gross domestic products (GDPs) (e.g. China, U.S.) challenges the ability of countries with lower GDPs (e.g. Cambodia) to protect their culture. Furthermore, the ability, or lack thereof, of the receiving countries to protect their culture is amplified by the existence and implementation of restrictive FDI policies imposed by their governments.

My study abroad in Bali, Indonesia, inspired this research topic as I noticed how globalization is changing the culture of its people. I learned their language and way of life which helped me understand the beauty and importance of cultural preservation. I believe we could all benefit from learning new perspectives as they could help us ideate solutions to contemporary issues and empathize with others.1比1复刻(ksu毕业证书)美国堪萨斯州立大学毕业证本科文凭证书原版一模一样

原版定制【微信:bwp0011】《(ksu毕业证书)美国堪萨斯州立大学毕业证本科文凭证书》【微信:bwp0011】成绩单 、雅思、外壳、留信学历认证永久存档查询,采用学校原版纸张、特殊工艺完全按照原版一比一制作(包括:隐形水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠,文字图案浮雕,激光镭射,紫外荧光,温感,复印防伪)行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备,十五年致力于帮助留学生解决难题,业务范围有加拿大、英国、澳洲、韩国、美国、新加坡,新西兰等学历材料,包您满意。

【业务选择办理准则】

一、工作未确定,回国需先给父母、亲戚朋友看下文凭的情况,办理一份就读学校的毕业证【微信bwp0011】文凭即可

二、回国进私企、外企、自己做生意的情况,这些单位是不查询毕业证真伪的,而且国内没有渠道去查询国外文凭的真假,也不需要提供真实教育部认证。鉴于此,办理一份毕业证【微信bwp0011】即可

三、进国企,银行,事业单位,考公务员等等,这些单位是必需要提供真实教育部认证的,办理教育部认证所需资料众多且烦琐,所有材料您都必须提供原件,我们凭借丰富的经验,快捷的绿色通道帮您快速整合材料,让您少走弯路。

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

【关于价格问题(保证一手价格)】

我们所定的价格是非常合理的,而且我们现在做得单子大多数都是代理和回头客户介绍的所以一般现在有新的单子 我给客户的都是第一手的代理价格,因为我想坦诚对待大家 不想跟大家在价格方面浪费时间

对于老客户或者被老客户介绍过来的朋友,我们都会适当给一些优惠。

Who Is Abhay Bhutada, MD of Poonawalla Fincorp

Abhay Bhutada, the Managing Director of Poonawalla Fincorp Limited, is an accomplished leader with over 15 years of experience in commercial and retail lending. A Qualified Chartered Accountant, he has been pivotal in leveraging technology to enhance financial services. Starting his career at Bank of India, he later founded TAB Capital Limited and co-founded Poonawalla Finance Private Limited, emphasizing digital lending. Under his leadership, Poonawalla Fincorp achieved a 'AAA' credit rating, integrating acquisitions and emphasizing corporate governance. Actively involved in industry forums and CSR initiatives, Abhay has been recognized with awards like "Young Entrepreneur of India 2017" and "40 under 40 Most Influential Leader for 2020-21." Personally, he values mindfulness, enjoys gardening, yoga, and sees every day as an opportunity for growth and improvement.

Using Online job postings and survey data to understand labour market trends

Using Online job postings and survey data to understand labour market trendsLabour Market Information Council | Conseil de l’information sur le marché du travail

[4:55 p.m.] Bryan Oates

OJPs are becoming a critical resource for policy-makers and researchers who study the labour market. LMIC continues to work with Vicinity Jobs’ data on OJPs, which can be explored in our Canadian Job Trends Dashboard. Valuable insights have been gained through our analysis of OJP data, including LMIC research lead

Suzanne Spiteri’s recent report on improving the quality and accessibility of job postings to reduce employment barriers for neurodivergent people.

Decoding job postings: Improving accessibility for neurodivergent job seekers

Improving the quality and accessibility of job postings is one way to reduce employment barriers for neurodivergent people.一比一原版美国新罕布什尔大学(unh)毕业证学历认证真实可查

永久可查学历认证【微信:A575476】【美国新罕布什尔大学(unh)毕业证成绩单Offer】【微信:A575476】(留信学历认证永久存档查询)采用学校原版纸张、特殊工艺完全按照原版一比一制作(包括:隐形水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠,文字图案浮雕,激光镭射,紫外荧光,温感,复印防伪)行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备,十五年致力于帮助留学生解决难题,业务范围有加拿大、英国、澳洲、韩国、美国、新加坡,新西兰等学历材料,包您满意。

【业务选择办理准则】

一、工作未确定,回国需先给父母、亲戚朋友看下文凭的情况,办理一份就读学校的毕业证【微信:A575476】文凭即可

二、回国进私企、外企、自己做生意的情况,这些单位是不查询毕业证真伪的,而且国内没有渠道去查询国外文凭的真假,也不需要提供真实教育部认证。鉴于此,办理一份毕业证【微信:A575476】即可

三、进国企,银行,事业单位,考公务员等等,这些单位是必需要提供真实教育部认证的,办理教育部认证所需资料众多且烦琐,所有材料您都必须提供原件,我们凭借丰富的经验,快捷的绿色通道帮您快速整合材料,让您少走弯路。

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

→ 【关于价格问题(保证一手价格)

我们所定的价格是非常合理的,而且我们现在做得单子大多数都是代理和回头客户介绍的所以一般现在有新的单子 我给客户的都是第一手的代理价格,因为我想坦诚对待大家 不想跟大家在价格方面浪费时间

对于老客户或者被老客户介绍过来的朋友,我们都会适当给一些优惠。

选择实体注册公司办理,更放心,更安全!我们的承诺:可来公司面谈,可签订合同,会陪同客户一起到教育部认证窗口递交认证材料,客户在教育部官方认证查询网站查询到认证通过结果后付款,不成功不收费!

真实可查(nwu毕业证书)美国西北大学毕业证学位证书范本原版一模一样

原版定制【微信:bwp0011】《(nwu毕业证书)美国西北大学毕业证学位证书》【微信:bwp0011】成绩单 、雅思、外壳、留信学历认证永久存档查询,采用学校原版纸张、特殊工艺完全按照原版一比一制作(包括:隐形水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠,文字图案浮雕,激光镭射,紫外荧光,温感,复印防伪)行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备,十五年致力于帮助留学生解决难题,业务范围有加拿大、英国、澳洲、韩国、美国、新加坡,新西兰等学历材料,包您满意。

【业务选择办理准则】

一、工作未确定,回国需先给父母、亲戚朋友看下文凭的情况,办理一份就读学校的毕业证【微信bwp0011】文凭即可

二、回国进私企、外企、自己做生意的情况,这些单位是不查询毕业证真伪的,而且国内没有渠道去查询国外文凭的真假,也不需要提供真实教育部认证。鉴于此,办理一份毕业证【微信bwp0011】即可

三、进国企,银行,事业单位,考公务员等等,这些单位是必需要提供真实教育部认证的,办理教育部认证所需资料众多且烦琐,所有材料您都必须提供原件,我们凭借丰富的经验,快捷的绿色通道帮您快速整合材料,让您少走弯路。

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

【关于价格问题(保证一手价格)】

我们所定的价格是非常合理的,而且我们现在做得单子大多数都是代理和回头客户介绍的所以一般现在有新的单子 我给客户的都是第一手的代理价格,因为我想坦诚对待大家 不想跟大家在价格方面浪费时间

对于老客户或者被老客户介绍过来的朋友,我们都会适当给一些优惠。

快速制作美国迈阿密大学牛津分校毕业证文凭证书英文原版一模一样

原版一模一样【微信:741003700 】【美国迈阿密大学牛津分校毕业证文凭证书】【微信:741003700 】学位证,留信认证(真实可查,永久存档)offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原海外各大学 Bachelor Diploma degree, Master Degree Diploma

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

一比一原版(RMIT毕业证)皇家墨尔本理工大学毕业证如何办理

RMIT硕士学位证成绩单【微信95270640】《皇家墨尔本理工大学毕业证书》《QQ微信95270640》学位证书电子版:在线制作皇家墨尔本理工大学毕业证成绩单GPA修改(制作RMIT毕业证成绩单RMIT文凭证书样本)、皇家墨尔本理工大学毕业证书与成绩单样本图片、《RMIT学历证书学位证书》、皇家墨尔本理工大学毕业证案例毕业证书制作軟體、在线制作加拿大硕士学历证书真实可查.

【本科硕士】皇家墨尔本理工大学皇家墨尔本理工大学本科学位证成绩单(GPA修改);学历认证(教育部认证);大学Offer录取通知书留信认证使馆认证;雅思语言证书等高仿类证书。

办理流程:

1客户提供办理皇家墨尔本理工大学皇家墨尔本理工大学本科学位证成绩单信息:姓名生日专业学位毕业时间等(如信息不确定可以咨询顾问:我们有专业老师帮你查询);

2开始安排制作毕业证成绩单电子图;

3毕业证成绩单电子版做好以后发送给您确认;

4毕业证成绩单电子版您确认信息无误之后安排制作成品;

5成品做好拍照或者视频给您确认;

6快递给客户(国内顺丰国外DHLUPS等快读邮寄)

真实网上可查的证明材料

1教育部学历学位认证留服官网真实存档可查永久存档。

2留学回国人员证明(使馆认证)使馆网站真实存档可查。

我们对海外大学及学院的毕业证成绩单所使用的材料尺寸大小防伪结构(包括:皇家墨尔本理工大学皇家墨尔本理工大学本科学位证成绩单隐形水印阴影底纹钢印LOGO烫金烫银LOGO烫金烫银复合重叠。文字图案浮雕激光镭射紫外荧光温感复印防伪)都有原版本文凭对照。质量得到了广大海外客户群体的认可同时和海外学校留学中介做到与时俱进及时掌握各大院校的(毕业证成绩单资格证结业证录取通知书在读证明等相关材料)的版本更新信息能够在第一时间掌握最新的海外学历文凭的样版尺寸大小纸张材质防伪技术等等并在第一时间收集到原版实物以求达到客户的需求。

本公司还可以按照客户原版印刷制作且能够达到客户理想的要求。有需要办理证件的客户请联系我们在线客服中心微信:95270640 或咨询在线父亲的家很狭小除了一张单人床和一张小方桌几乎没有多余的空间山娃一下子就联想起学校的男小便处山娃很想笑却怎么也笑不出来山娃很迷惑父亲的家除了一扇小铁门连窗户也没有墓穴一般阴森森有些骇人父亲的城也便成了山娃的城父亲的家也便成了山娃的家父亲让山娃呆在屋里做作业看电视最多只能在门口透透气不能跟陌生人搭腔更不能乱跑一怕迷路二怕拐子拐人山娃很惊惧去年村里的田鸡就因为跟父亲进城一不小心被人拐跑了至今不见踪影害不

Accounting Information Systems (AIS).pptx

An accounting information system (AIS) refers to tools and systems designed for the collection and display of accounting information so accountants and executives can make informed decisions.

Bridging the gap: Online job postings, survey data and the assessment of job ...

Bridging the gap: Online job postings, survey data and the assessment of job ...Labour Market Information Council | Conseil de l’information sur le marché du travail

OJP data from firms like Vicinity Jobs have emerged as a complement to traditional sources of labour demand data, such as the Job Vacancy and Wages Survey (JVWS). Ibrahim Abuallail, PhD Candidate, University of Ottawa, presented research relating to bias in OJPs and a proposed approach to effectively adjust OJP data to complement existing official data (such as from the JVWS) and improve the measurement of labour demand.Detailed power point presentation on compound interest and how it is calculated

Detailed information about compund interest

The Rise and Fall of Ponzi Schemes in America.pptx

Ponzi schemes, a notorious form of financial fraud, have plagued America’s investment landscape for decades. Named after Charles Ponzi, who orchestrated one of the most infamous schemes in the early 20th century, these fraudulent operations promise high returns with little or no risk, only to collapse and leave investors with significant losses. This article explores the nature of Ponzi schemes, notable cases in American history, their impact on victims, and measures to prevent falling prey to such scams.

Understanding Ponzi Schemes

A Ponzi scheme is an investment scam where returns are paid to earlier investors using the capital from newer investors, rather than from legitimate profit earned. The scheme relies on a constant influx of new investments to continue paying the promised returns. Eventually, when the flow of new money slows down or stops, the scheme collapses, leaving the majority of investors with substantial financial losses.

Historical Context: Charles Ponzi and His Legacy

Charles Ponzi is the namesake of this deceptive practice. In the 1920s, Ponzi promised investors in Boston a 50% return within 45 days or 100% return in 90 days through arbitrage of international reply coupons. Initially, he paid returns as promised, not from profits, but from the investments of new participants. When his scheme unraveled, it resulted in losses exceeding $20 million (equivalent to about $270 million today).

Notable American Ponzi Schemes

1. Bernie Madoff: Perhaps the most notorious Ponzi scheme in recent history, Bernie Madoff’s fraud involved $65 billion. Madoff, a well-respected figure in the financial industry, promised steady, high returns through a secretive investment strategy. His scheme lasted for decades before collapsing in 2008, devastating thousands of investors, including individuals, charities, and institutional clients.

2. Allen Stanford: Through his company, Stanford Financial Group, Allen Stanford orchestrated a $7 billion Ponzi scheme, luring investors with fraudulent certificates of deposit issued by his offshore bank. Stanford promised high returns and lavish lifestyle benefits to his investors, which ultimately led to a 110-year prison sentence for the financier in 2012.

3. Tom Petters: In a scheme that lasted more than a decade, Tom Petters ran a $3.65 billion Ponzi scheme, using his company, Petters Group Worldwide. He claimed to buy and sell consumer electronics, but in reality, he used new investments to pay off old debts and fund his extravagant lifestyle. Petters was convicted in 2009 and sentenced to 50 years in prison.

4. Eric Dalius and Saivian: Eric Dalius, a prominent figure behind Saivian, a cashback program promising high returns, is under scrutiny for allegedly orchestrating a Ponzi scheme. Saivian enticed investors with promises of up to 20% cash back on everyday purchases. However, investigations suggest that the returns were paid using new investments rather than legitimate profits. The collapse of Saivian l

South Dakota State University degree offer diploma Transcript

办理美国SDSU毕业证书制作南达科他州立大学假文凭定制Q微168899991做SDSU留信网教留服认证海牙认证改SDSU成绩单GPA做SDSU假学位证假文凭高仿毕业证GRE代考如何申请南达科他州立大学South Dakota State University degree offer diploma Transcript

Discover the Future of Dogecoin with Our Comprehensive Guidance

Learn in-depth about Dogecoin's trajectory and stay informed with 36crypto's essential and up-to-date information about the crypto space.

Our presentation delves into Dogecoin's potential future, exploring whether it's destined to skyrocket to the moon or face a downward spiral. In addition, it highlights invaluable insights. Don't miss out on this opportunity to enhance your crypto understanding!

https://36crypto.com/the-future-of-dogecoin-how-high-can-this-cryptocurrency-reach/

New Visa Rules for Tourists and Students in Thailand | Amit Kakkar Easy Visa

Discover essential details about Thailand's recent visa policy changes, tailored for tourists and students. Amit Kakkar Easy Visa provides a comprehensive overview of new requirements, application processes, and tips to ensure a smooth transition for all travelers.

What's a worker’s market? Job quality and labour market tightness

What's a worker’s market? Job quality and labour market tightnessLabour Market Information Council | Conseil de l’information sur le marché du travail

In a tight labour market, job-seekers gain bargaining power and leverage it into greater job quality—at least, that’s the conventional wisdom.

Michael, LMIC Economist, presented findings that reveal a weakened relationship between labour market tightness and job quality indicators following the pandemic. Labour market tightness coincided with growth in real wages for only a portion of workers: those in low-wage jobs requiring little education. Several factors—including labour market composition, worker and employer behaviour, and labour market practices—have contributed to the absence of worker benefits. These will be investigated further in future work.Seeman_Fiintouch_LLP_Newsletter_Jun_2024.pdf

The Impact of the 2024 Indian

Election Beyond Borders

01. Investment Gyan

02. Market Update

03. Inspiration investment story

KYC Compliance: A Cornerstone of Global Crypto Regulatory Frameworks

This presentation explores the pivotal role of KYC compliance in shaping and enforcing global regulations within the dynamic landscape of cryptocurrencies. Dive into the intricate connection between KYC practices and the evolving legal frameworks governing the crypto industry.

Recently uploaded (20)

Independent Study - College of Wooster Research (2023-2024) FDI, Culture, Glo...

Independent Study - College of Wooster Research (2023-2024) FDI, Culture, Glo...

Using Online job postings and survey data to understand labour market trends

Using Online job postings and survey data to understand labour market trends

Power point analisis laporan keuangan chapter 7 subramanyam

Power point analisis laporan keuangan chapter 7 subramanyam

Bridging the gap: Online job postings, survey data and the assessment of job ...

Bridging the gap: Online job postings, survey data and the assessment of job ...

Detailed power point presentation on compound interest and how it is calculated

Detailed power point presentation on compound interest and how it is calculated

The Rise and Fall of Ponzi Schemes in America.pptx

The Rise and Fall of Ponzi Schemes in America.pptx

South Dakota State University degree offer diploma Transcript

South Dakota State University degree offer diploma Transcript

Discover the Future of Dogecoin with Our Comprehensive Guidance

Discover the Future of Dogecoin with Our Comprehensive Guidance

New Visa Rules for Tourists and Students in Thailand | Amit Kakkar Easy Visa

New Visa Rules for Tourists and Students in Thailand | Amit Kakkar Easy Visa

What's a worker’s market? Job quality and labour market tightness

What's a worker’s market? Job quality and labour market tightness

KYC Compliance: A Cornerstone of Global Crypto Regulatory Frameworks

KYC Compliance: A Cornerstone of Global Crypto Regulatory Frameworks

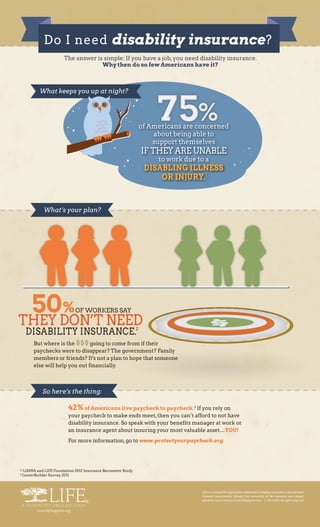

Diam Infographic 2013

- 1. 1,2 LIMRA and LIFE Foundation 2012 Insurance Barometer Study 3 CareerBuilder Survey,2011 What keeps you up at night? 42%of Americans live paycheck to paycheck.3 If you rely on your paycheck to make ends meet,then you can’t afford to not have disability insurance. So speak with your benefits manager at work or an insurance agent about insuring your most valuable asset…YOU! For more information,go to www.protectyourpaycheck.org. The answer is simple: If you have a job,you need disability insurance. Why then do so few Americans have it? LIFE is a nonprofit organization dedicated to helping consumers take personal financial responsibility through the ownership of life insurance and related products. Learn more at www.lifehappens.org © 2013 LIFE. All rights reserved. of Americans are concerned about being able to support themselves IF THEY ARE UNABLE to work due to a DISABLING ILLNESS OR INJURY.1 Do I need disability insurance? What’s your plan? 50%OF WORKERS SAY THEY DON’T NEED DISABILITY INSURANCE. So here’s the thing: 2 But where is the $$$ going to come from if their paychecks were to disappear? The government? Family members or friends? It's not a plan to hope that someone else will help you out financially.