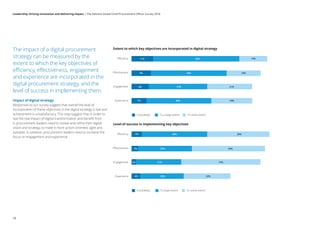

Downloaded 32 times

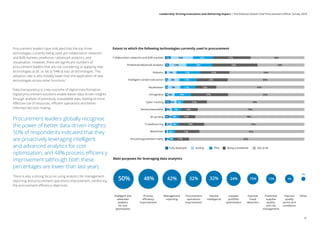

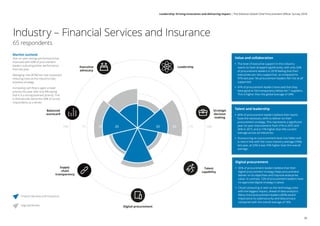

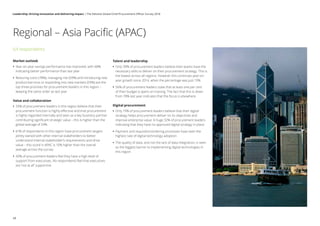

1) The survey found that procurement leaders are primarily focused on cost reduction, new product/market development, and managing risks over the next 12 months. However, supplier collaboration is being used less as a strategy to drive value compared to last year. 2) Overall supply chain transparency is poor, with most procurement leaders only having visibility into their direct/Tier 1 suppliers. Improving transparency could help deliver more value while mitigating risks. 3) While most procurement leaders believe they have executive support, only a quarter see themselves as "excellent" business partners contributing significant strategic value. Greater alignment with business strategies and priorities is needed.