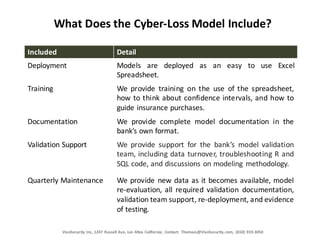

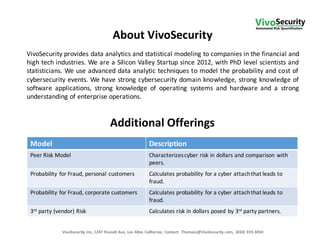

Vivosecurity Inc. specializes in providing statistical modeling and analysis for operational risk related to cybersecurity events, particularly focusing on banks' compliance with Federal Reserve guidance. They offer a cyber-loss model that quantifies breach costs and aids in insurance adequacy while ensuring SR 11-7 and SR 15-18 compliance. The company's services include model validation support, documentation, and training, leveraging advanced data analytic techniques and cross-company data to enhance risk management culture in financial institutions.

![제 23회 보아즈(BOAZ) 빅데이터 컨퍼런스 - [MBOAX] : ABSA를 활용한 소비자 반응 분석 기반 운영 효율화 대시보드 설계](https://cdn.slidesharecdn.com/ss_thumbnails/3-1boaz23rdconferencemboax-260203102709-9d519923-thumbnail.jpg?width=640&height=640&fit=bounds)