Downloaded 30 times

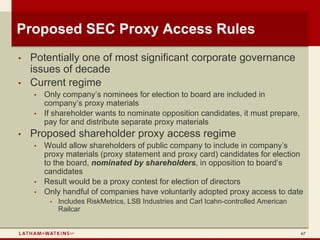

The document discusses critical issues for the 2010 proxy season, highlighting a significant rise in votes against director nominees and the increasing influence of proxy advisory firms. It emphasizes the shift in corporate governance activism, particularly among small and mid-cap companies, and the changing landscape due to regulatory initiatives like the SEC's elimination of broker discretionary voting. The overall trend indicates a growing demand for director accountability and changes in executive compensation practices.