Uploaded byMaryam Hidayatallah CPFA,MIPA,MA,CICA

CREDIT RISK MODEL

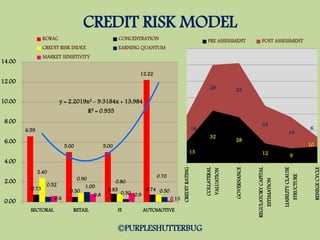

This document presents the results of a credit risk model. It includes credit risk index scores for various sectors, with automotive and retail having the highest risk. A quadratic regression equation is shown with an R2 value of 0.955 to model the relationship between credit risk concentration and return on risk-adjusted capital. Various credit risk assessment factors are listed and ranked in order of importance, with credit rating, collateral valuation, and governance being the top three factors.

CREDIT RISK MODEL

- 1. CREDIT RISK MODEL 6.59 5.005.00 12.22 0.73 0.50 0.83 0.74 2.40 0.90 0.80 0.70 0.52 1.00 0.30 0.50 0.6 0.8 0.9 0.13 y = 2.2019x2 - 9.3184x + 13.984 R² = 0.955 0.00 2.00 4.00 6.00 8.00 10.00 12.00 14.00 SECTORAL RETAIL FI AUTOMOTIVE RORAC CONCENTRATION CREDIT RISK INDEX EARNING QUANTUM MARKET SENSITIVITY 13 32 28 12 9 10 16 28 33 23 19 6 CREDITRATING COLLATERAL VALUATION GOVERNANCE REGULATORYCAPITAL ESTIMATION LIABILITYCLAUSE STRUCTURE RENEGECYCLE PRE ASSESSMENT POST ASSESSMENT ©PURPLESHUTTERBUG