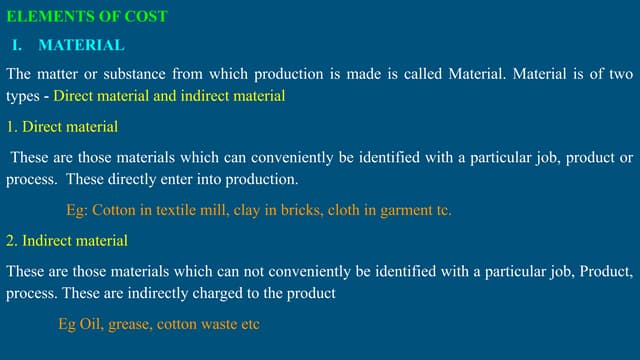

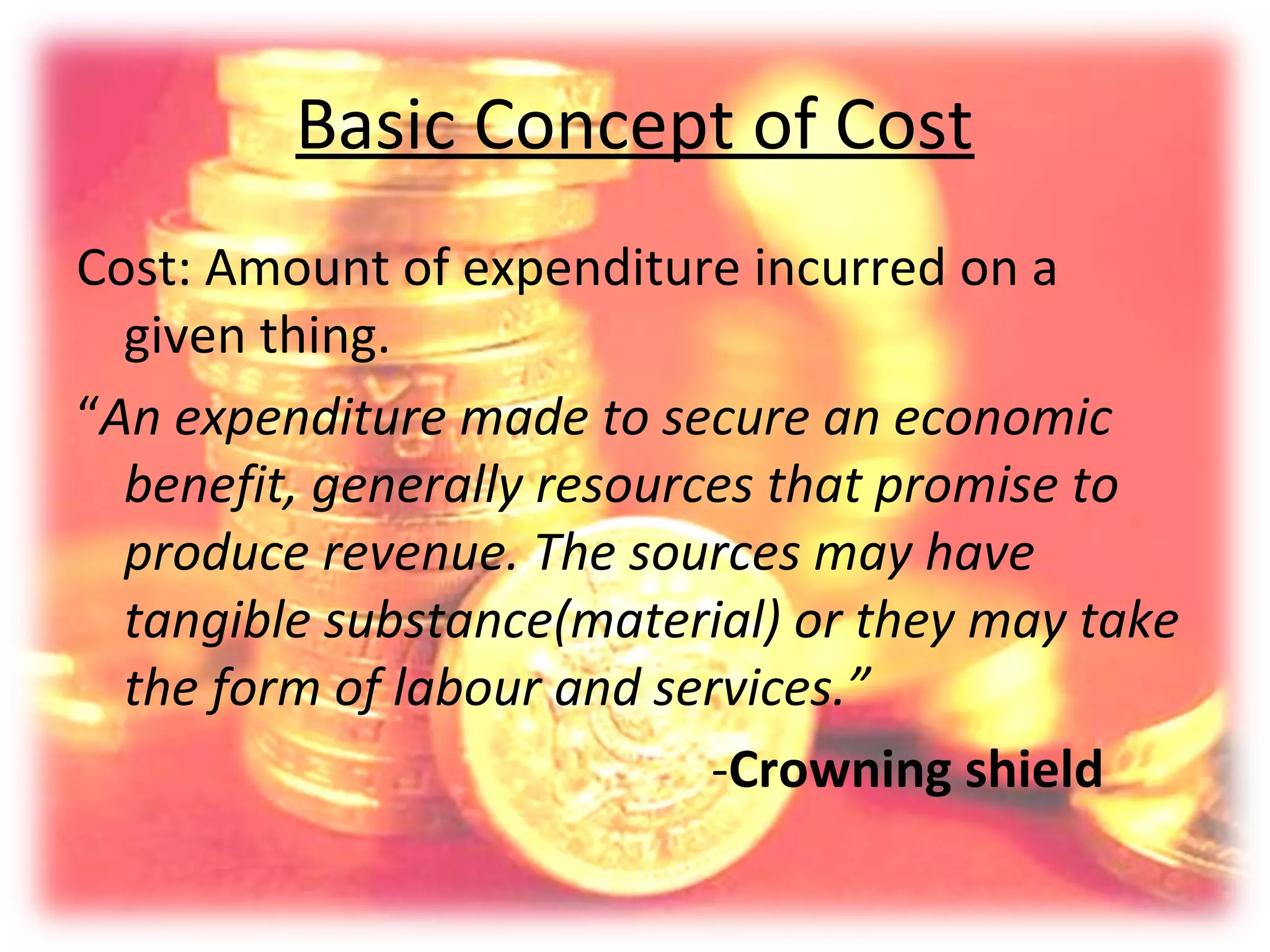

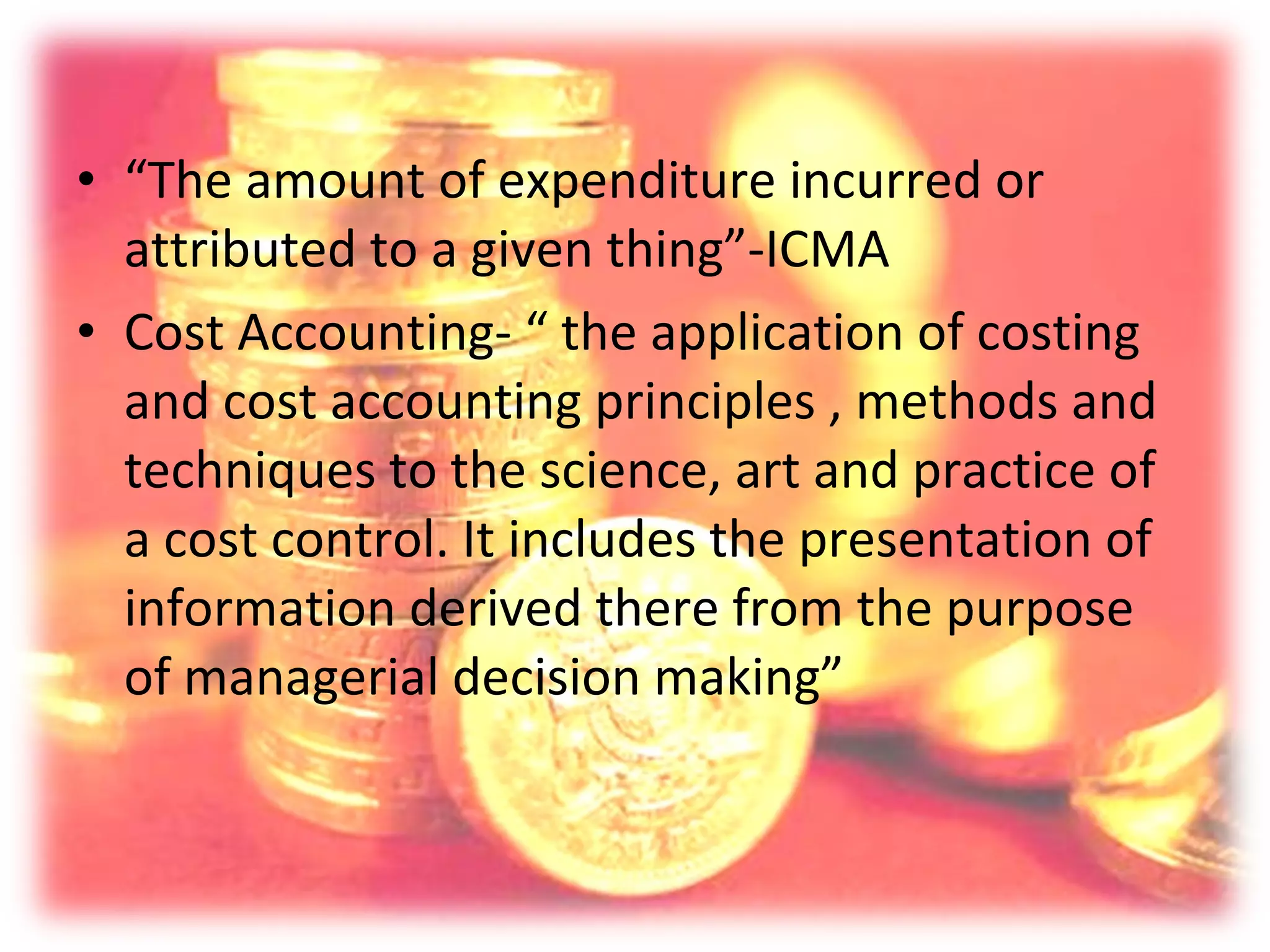

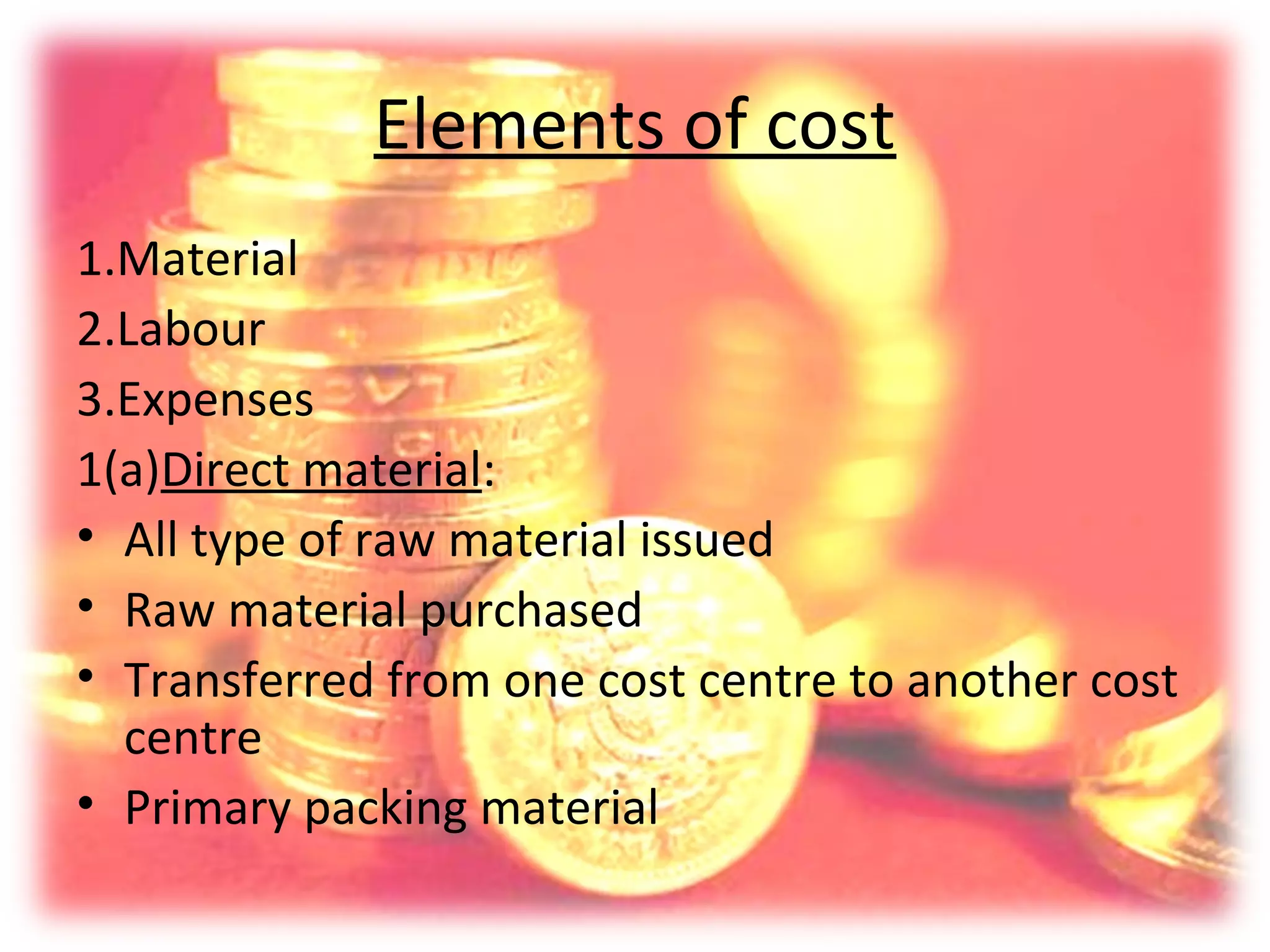

This document discusses the basic concepts of cost and cost elements. It defines cost as the amount of expenditure incurred on a given thing. There are three main elements of cost: material, labor, and expenses. Material includes direct materials like raw materials and indirect materials used for maintenance. Labor includes direct labor involved in production and indirect labor. Expenses include direct expenses for a product and indirect expenses like rent and utilities. Overhead includes the indirect costs of materials, labor, and other expenses. Costs also vary in their nature between being fixed, variable, controllable, and non-controllable.

![7_C's_OF_COMMUNIOCATION[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/7csofcommuniocation1-230801063320-9af405b3-thumbnail.jpg?width=640&height=640&fit=bounds)