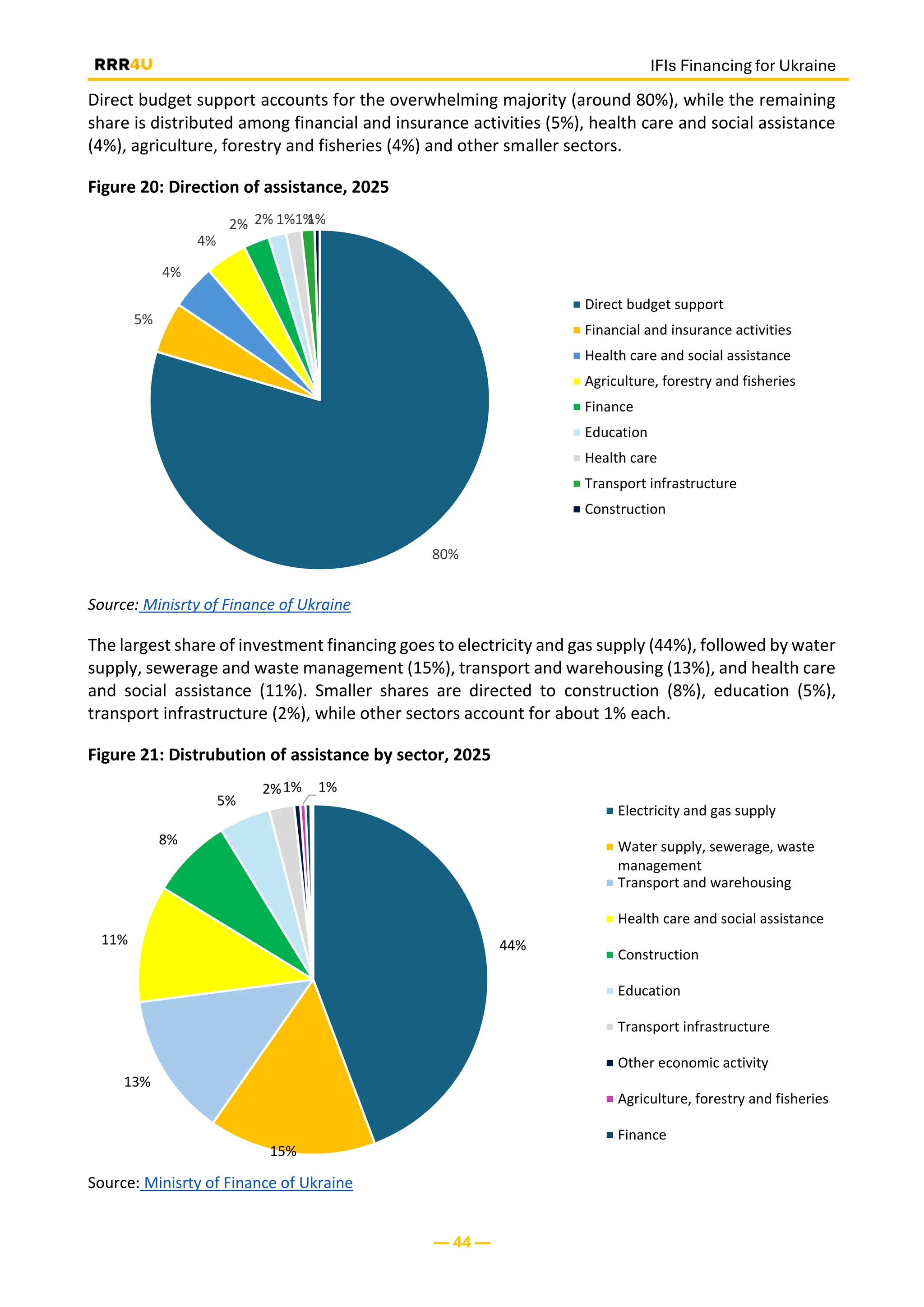

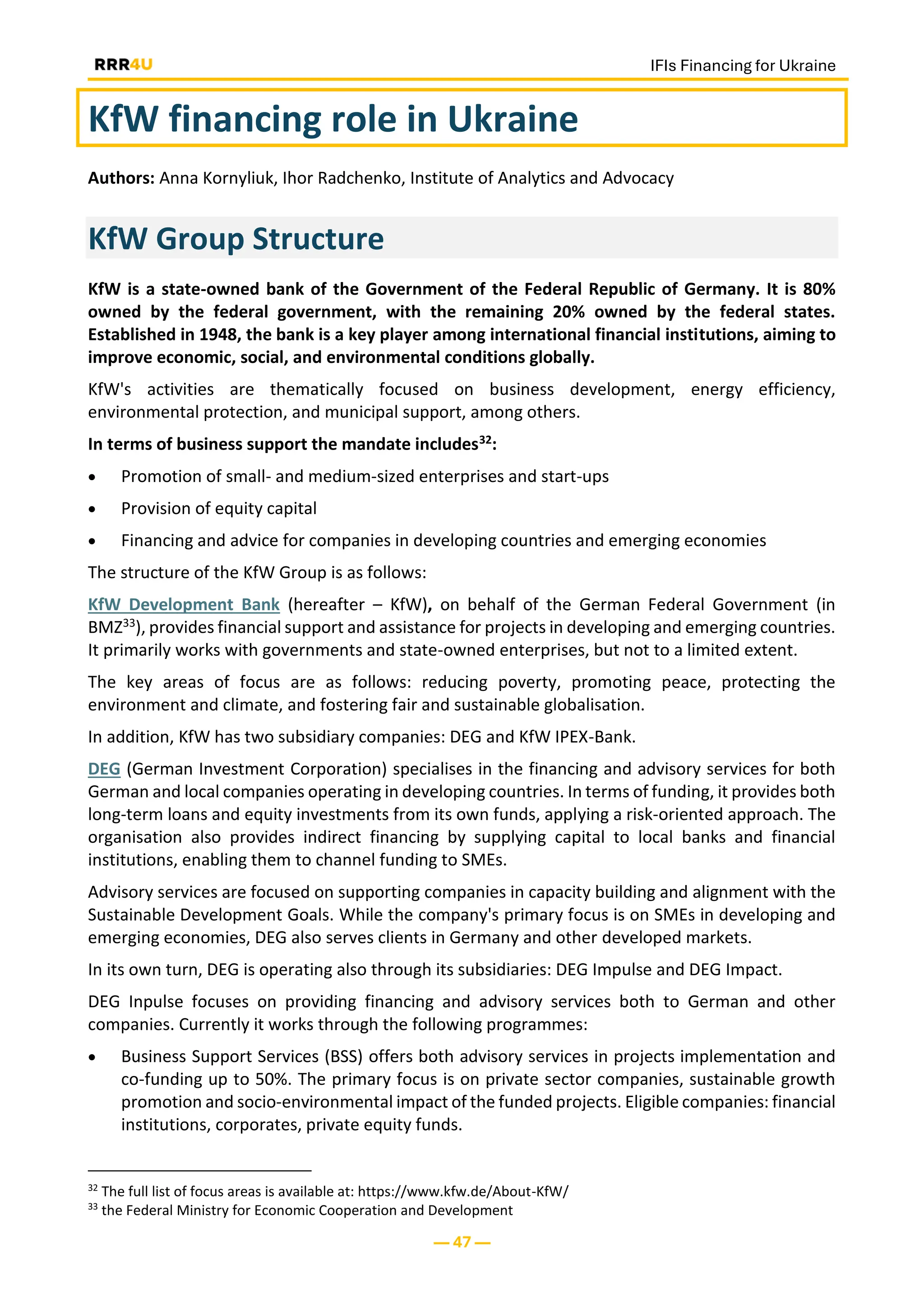

Download to read offline

Після повномасштабного вторгнення роль міжнародних фінансових організацій (МФО) змістилася в бік надзвичайного реагування та забезпечення стійкості. Вони стали ще важливішими партнерами для забезпечення стійкості України та екстреного відновлення, надаючи фінансові ресурси, консультації з реформ та технічну допомогу. Цей звіт узагальнює висновки щодо ролі міжнародних фінансових організацій у відновленні України – Групи Світового банку, ЄБРР, ЄІБ та KfW – підготовлені консорціумом RRR4U. Вступний розділ викладає, як інструменти МФО працюють в Україні, чому інвестиційні потоки повільніші, ніж потрібно, і що має змінитися для прискорення пріоритетного фінансування, особливо для стійкої інфраструктури та зростання приватного сектору. Він оснований на чотирьох окремих есе про роль МФО, які представлені в звіті повністю. Есе описують мандати, процедури, портфелі та обмеження; визначають вузькі місця та перешкоди для розподілу та виплати фінансування. Звіт містить рекомендації щодо зміни підходів та політики для різних зацікавлених сторін, включаючи уряд України, Європейську Комісію та МФО. Звертаємо увагу! Матеріал доступний англійською мовою