Compensation Design

Compensation Design

Moneythat is received under

Money that is received under Employer-Employee

Employer-Employee

relationship

relationship is called

is called Salary.

Salary. If one is freelancer or are hired

If one is freelancer or are hired

by an organization on contract basis, their income would not

by an organization on contract basis, their income would not

be treated as salary income.( In such case your income would

be treated as salary income.( In such case your income would

be treated as income from business and profession).

be treated as income from business and profession).

The salary consists of following parts:

The salary consists of following parts:

Basic Salary

Basic Salary: This is the core of salary, and many other components may

: This is the core of salary, and many other components may

be calculated based on this amount. It usually depends on one’s grade

be calculated based on this amount. It usually depends on one’s grade

within the company’s salary structure. It is a

within the company’s salary structure. It is a fixed

fixed part of one’s

part of one’s

compensation structure.

compensation structure.

2.

Allowance

Allowance: It isthe amount received by an individual paid by his/her

: It is the amount received by an individual paid by his/her

employer in addition to salary to meet some service requirements such

employer in addition to salary to meet some service requirements such

as

as Dearness Allowance(DA), House Rent Allowance (HRA), Leave Travel

Dearness Allowance(DA), House Rent Allowance (HRA), Leave Travel

Assistance(LTA)/Leave Fair Assistance (LFA), Leave Travel Concessions

Assistance(LTA)/Leave Fair Assistance (LFA), Leave Travel Concessions

(LTC), Lunch Allowance/Lunch Coupon, Conveyance Allowance , Children’s

(LTC), Lunch Allowance/Lunch Coupon, Conveyance Allowance , Children’s

Education Allowance, City compensatory Allowance etc

Education Allowance, City compensatory Allowance etc. Allowance can be

. Allowance can be

fully taxable, partly or non taxable.

fully taxable, partly or non taxable.

Perquisites/Benefits:

Perquisites/Benefits: Is any benefit or amenity granted or provided

Is any benefit or amenity granted or provided

free of cost or at concessional rate such as

free of cost or at concessional rate such as Rent free unfurnished house,

Rent free unfurnished house,

Rent free furnished house, Motor car facility, Reimbursement of Gas, Electricity &

Rent free furnished house, Motor car facility, Reimbursement of Gas, Electricity &

Water, Club facility, Domestic Servant Facility, Interest Subsidy on Loan,

Water, Club facility, Domestic Servant Facility, Interest Subsidy on Loan,

Reimbursement of medical bills, Reimbursement of Hospital bills, Reimbursement

Reimbursement of medical bills, Reimbursement of Hospital bills, Reimbursement

of telephone bills, Benefits derived by employee stock options

of telephone bills, Benefits derived by employee stock options, and so on.

, and so on.

3.

How are perquisitestaxed?

How are perquisites taxed?

Since these are non-cash components, they cannot be taxed directly. So the

Since these are non-cash components, they cannot be taxed directly. So the

income tax laws attach a certain value to each of these components and charges a

income tax laws attach a certain value to each of these components and charges a

tax on them. The calculation of this value varies from category to category.

tax on them. The calculation of this value varies from category to category.

Nevertheless, the thumb rule across all categories is that only those benefits that

Nevertheless, the thumb rule across all categories is that only those benefits that

you use for personal purpose will be considered as perquisites.

you use for personal purpose will be considered as perquisites.

• Deductions:

Deductions: Two type of deduction are made from salary

Two type of deduction are made from salary

Compulsory deduction such as Provident Fund, Income tax, Professional Tax

Compulsory deduction such as Provident Fund, Income tax, Professional Tax

(where applicable) .

(where applicable) .

Optional deduction such as recovery for advance or loan if taken, voluntary

Optional deduction such as recovery for advance or loan if taken, voluntary

contribution to P.F etc

contribution to P.F etc

Provident Fund Contribution

Provident Fund Contribution

Provident fund contribution has two sides – the employer’s contribution

Provident fund contribution has two sides – the employer’s contribution

and employee’s contribution

and employee’s contribution.

. This is usually

This is usually 12 per cent

12 per cent of the basic salary

of the basic salary.

.

However, this contribution is not paid out. It is directly deposited in Provident

However, this contribution is not paid out. It is directly deposited in Provident

Fund (PF) account and paid to employee when he/she retires or resigns. There is

Fund (PF) account and paid to employee when he/she retires or resigns. There is

also employee’s contribution to PF. This amount is deducted from his monthly

also employee’s contribution to PF. This amount is deducted from his monthly

salary and deposited in his PF account.

salary and deposited in his PF account.

4.

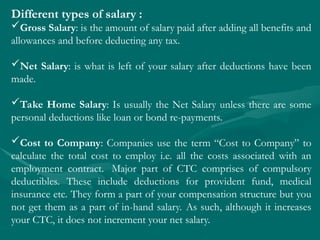

Different types ofsalary :

Gross Salary: is the amount of salary paid after adding all benefits and

allowances and before deducting any tax.

Net Salary: is what is left of your salary after deductions have been

made.

Take Home Salary: Is usually the Net Salary unless there are some

personal deductions like loan or bond re-payments.

Cost to Company: Companies use the term “Cost to Company” to

calculate the total cost to employ i.e. all the costs associated with an

employment contract. Major part of CTC comprises of compulsory

deductibles. These include deductions for provident fund, medical

insurance etc. They form a part of your compensation structure but you

not get them as a part of in-hand salary. As such, although it increases

your CTC, it does not increment your net salary.

5.

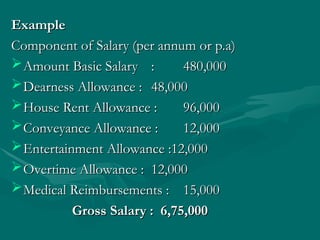

Example

Example

Component of Salary(per annum or p.a)

Component of Salary (per annum or p.a)

Amount Basic Salary

Amount Basic Salary :

: 480,000

480,000

Dearness Allowance :

Dearness Allowance : 48,000

48,000

House Rent Allowance :

House Rent Allowance : 96,000

96,000

Conveyance Allowance :

Conveyance Allowance : 12,000

12,000

Entertainment Allowance :12,000

Entertainment Allowance :12,000

Overtime Allowance :

Overtime Allowance : 12,000

12,000

Medical Reimbursements :

Medical Reimbursements : 15,000

15,000

Gross Salary : 6,75,000

Gross Salary : 6,75,000

6.

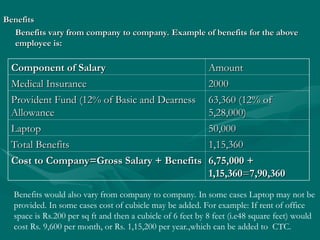

Benefits

Benefits

Benefits vary fromcompany to company. Example of benefits for the above

Benefits vary from company to company. Example of benefits for the above

employee is:

employee is:

Component of Salary

Component of Salary Amount

Amount

Medical Insurance

Medical Insurance 2000

2000

Provident Fund (12% of Basic and Dearness

Provident Fund (12% of Basic and Dearness

Allowance

Allowance

63,360 (12% of

63,360 (12% of

5,28,000)

5,28,000)

Laptop

Laptop 50,000

50,000

Total Benefits

Total Benefits 1,15,360

1,15,360

Cost to Company=Gross Salary + Benefits

Cost to Company=Gross Salary + Benefits 6,75,000 +

6,75,000 +

1,15,360

1,15,360=

=7,90,360

7,90,360

Benefits would also vary from company to company. In some cases Laptop may not be

provided. In some cases cost of cubicle may be added. For example: If rent of office

space is Rs.200 per sq ft and then a cubicle of 6 feet by 8 feet (i.e48 square feet) would

cost Rs. 9,600 per month, or Rs. 1,15,200 per year.,which can be added to CTC.

7.

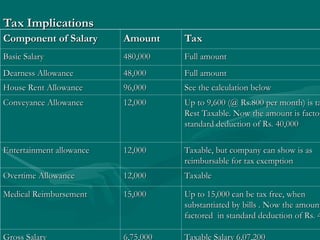

Tax Implications

Tax Implications

Componentof Salary

Component of Salary Amount

Amount Tax

Tax

Basic Salary

Basic Salary 480,000

480,000 Full amount

Full amount

Dearness Allowance

Dearness Allowance 48,000

48,000 Full amount

Full amount

House Rent Allowance

House Rent Allowance 96,000

96,000 See the calculation below

See the calculation below

Conveyance Allowance

Conveyance Allowance 12,000

12,000 Up to 9,600 (@ Rs.800 per month) is ta

Up to 9,600 (@ Rs.800 per month) is ta

Rest Taxable. Now the amount is factor

Rest Taxable. Now the amount is factor

standard deduction of Rs. 40,000

standard deduction of Rs. 40,000

Entertainment allowance

Entertainment allowance 12,000

12,000 Taxable, but company can show is as

Taxable, but company can show is as

reimbursable for tax exemption

reimbursable for tax exemption

Overtime Allowance

Overtime Allowance 12,000

12,000 Taxable

Taxable

Medical Reimbursement

Medical Reimbursement 15,000

15,000 Up to 15,000 can be tax free, when

Up to 15,000 can be tax free, when

substantiated by bills . Now the amount

substantiated by bills . Now the amount

factored in standard deduction of Rs. 4

factored in standard deduction of Rs. 4

Gross Salary 6,75,000 Taxable Salary 6,07,200

8.

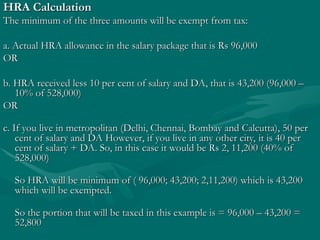

HRA Calculation

HRA Calculation

Theminimum of the three amounts will be exempt from tax:

The minimum of the three amounts will be exempt from tax:

a. Actual HRA allowance in the salary package that is Rs 96,000

a. Actual HRA allowance in the salary package that is Rs 96,000

OR

OR

b. HRA received less 10 per cent of salary and DA, that is 43,200 (96,000 –

b. HRA received less 10 per cent of salary and DA, that is 43,200 (96,000 –

10% of 528,000)

10% of 528,000)

OR

OR

c. If you live in metropolitan (Delhi, Chennai, Bombay and Calcutta), 50 per

c. If you live in metropolitan (Delhi, Chennai, Bombay and Calcutta), 50 per

cent of salary and DA However, if you live in any other city, it is 40 per

cent of salary and DA However, if you live in any other city, it is 40 per

cent of salary + DA. So, in this case it would be Rs 2, 11,200 (40% of

cent of salary + DA. So, in this case it would be Rs 2, 11,200 (40% of

528,000)

528,000)

So HRA will be minimum of ( 96,000; 43,200; 2,11,200) which is 43,200

So HRA will be minimum of ( 96,000; 43,200; 2,11,200) which is 43,200

which will be exempted.

which will be exempted.

So the portion that will be taxed in this example is = 96,000 – 43,200 =

So the portion that will be taxed in this example is = 96,000 – 43,200 =

52,800

52,800

9.

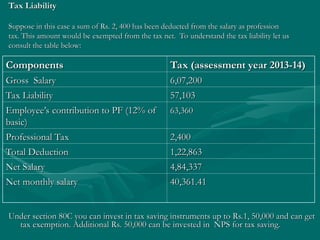

Tax Liability

Tax Liability

Supposein this case a sum of Rs. 2, 400 has been deducted from the salary as profession

Suppose in this case a sum of Rs. 2, 400 has been deducted from the salary as profession

tax. This amount would be exempted from the tax net. To understand the tax liability let us

tax. This amount would be exempted from the tax net. To understand the tax liability let us

consult the table below:

consult the table below:

Under section 80C you can invest in tax saving instruments up to Rs.1, 50,000 and can get

Under section 80C you can invest in tax saving instruments up to Rs.1, 50,000 and can get

tax exemption. Additional Rs. 50,000 can be invested in NPS for tax saving.

tax exemption. Additional Rs. 50,000 can be invested in NPS for tax saving.

Components

Components Tax (assessment year 2013-14)

Tax (assessment year 2013-14)

Gross Salary

Gross Salary 6,07,200

6,07,200

Tax Liability

Tax Liability 57,103

57,103

Employee’s contribution to PF (12% of

Employee’s contribution to PF (12% of

basic)

basic)

63,360

63,360

Professional Tax

Professional Tax 2,400

2,400

Total Deduction

Total Deduction 1,22,863

1,22,863

Net Salary

Net Salary 4,84,337

4,84,337

Net monthly salary

Net monthly salary 40,361.41

40,361.41