Downloaded 45 times

![

Every trading company has an implied power to borrow, as borrowing is implied in

the object for which it is incorporated. A trading company can exercise this power

even if it is not included in the Memorandum. However non-trading company has no

implied power to borrow and such power can be taken by it implied power to borrow

and such power can be taken by it by including a clause to that effect in the

Memorandum.

Restrictions on borrowing power : A public company can borrow only after

the receipt of Commencement Certificate. [Section 149(1)]. But a private company

can borrow immediately after the incorporation](https://image.slidesharecdn.com/companysact1956part-2-140125035227-phpapp01/85/Company-s-act-1956-part-2-17-320.jpg)

![

The Board of Directors may borrow moneys by passing a resolution passed at the

meetings of the Board. The board may delegate its borrowing powers to a Committee

of Directors. Such a resolution should specifically mention the aggregate amount upto

which the moneys can be borrowed by the Committee, the Managing Director,

Manager or any other principal officer of the company on such conditions as it

may prescribe [Section292 (1) (c)]

The moneys borrowed together with the moneys already borrowed by the company

(excluding loans obtained from banks i.e. working capital) shall not exceed

the aggregate of the paid up capital and the free reserves.[Section 293(1)(d)]

It may be noted that a company may borrow in excess of its paid up capital and free

reserves if it is so consented and authorized by the shareholders at a general meeting.](https://image.slidesharecdn.com/companysact1956part-2-140125035227-phpapp01/85/Company-s-act-1956-part-2-18-320.jpg)

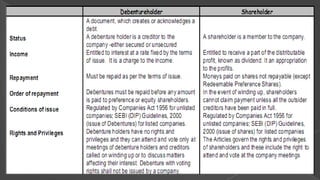

![Debenture includes debentures stock, bonds, and any other securities of a

company, whether constituting a charge on the assets of the company or not.

FEATURES OF A DEBENTURE SEC 2(12)] :

(i) In the form of a certificate (like a share certificate) issued under the common seal

of the company. The certificate is an acknowledgement by the company of

indebtedness to a holder.

(ii) Provides for the payment of a specified principal sum at a specified date with

contracted rate of interest.](https://image.slidesharecdn.com/companysact1956part-2-140125035227-phpapp01/85/Company-s-act-1956-part-2-19-320.jpg)

![Issued in series

(v) Secured by a charge on the undertaking of the company, or on some class of its

assets or on some part of its profits. [Unsecured debenture is a deposit with the

meaning of the Companies (Acceptance of Deposits)Rules 1975].

(iv)

DEBENTURE STOCK :

Debenture stock is of the same nature as debentures but instead of each lender

having separate debenture bond he gets a certificate entitling him to a specified portion

one large loan. It is borrowed capital consolidated into one mass for the sake of

convenience.](https://image.slidesharecdn.com/companysact1956part-2-140125035227-phpapp01/85/Company-s-act-1956-part-2-20-320.jpg)

![REGISTRATION OF CHARGES [SECTION 125] :

The security created and charged for the following purposes must be registered with the ROC within 30 days(or

further period of 30 days with additional fees) after the date of their creation.

Securing any issue of debentures;

Uncalled share capital of the company;

Any immovable property;

Book debts, stock in trade or other current assets of the company;

Any movable property (not being a pledge);

Calls made but not paid;

IPRs of the company.

The ROC shall with respect to each company maintain a Register of charges containing all the specified

particulars. Upon registration of charge by the company, ROC shall issue a Certificate of charges, which shall be

conclusive evidence.](https://image.slidesharecdn.com/companysact1956part-2-140125035227-phpapp01/85/Company-s-act-1956-part-2-26-320.jpg)

The document discusses various aspects of a company's membership, shares, management, meetings, borrowings, accounts, and winding up. It defines members/shareholders as the persons who collectively form the company. Shares represent a unit of ownership and come in two types - ordinary shares and preference shares. Company management follows a hierarchy and involves planning, organizing, and other functions. Statutory meetings and annual general meetings must be held, with requirements around notice periods, quorum, and minutes. A company has implied borrowing powers but some restrictions apply, and debentures are a form of secured debt instrument that a company can issue.

![Sample Silicon Valley Series A Term Sheet from DLA Piper [SVNewTech]](https://cdn.slidesharecdn.com/ss_thumbnails/svnewtech-series-a-termsheet-100108184114-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)