Here are the income tax rates for financial year 2018-19 for individuals, Hindu undivided family, association of persons, body of individuals, artificial juridical person post Union Budget 2018.

Here are the income tax rates for financial year 2018-19 for individuals, Hindu undivided family, association of persons, body of individuals, artificial juridical person post Union Budget 2018.

Used Motorcycle - bike 2I bought my first used motorcycle while I was in college. It was a Honda 750. I road it around town and I took it on long trips. One summer I took it from my home state of Minnesota out to Wyoming, Montana and even up into Canada. The next summer I road it out to New Hampshire and eventually to Boston where I sold it and bought an old Jeep.

Onsite Motorcycle Inspection and Verification - Sample ReportGoose & Gander

WeGoLook.com is a nationwide service with over 7,400 agents who provide custom tasking, reporting, inspections, field services and more. Here is a sample motorcycle inspection report.

We completed an analysis of Indian Motorcycle's current situation since being acquired by Polaris. We completed market research, conducted interviews with Indian fanatics, collectors, dealers, etc., competitive analysis, and watched "The World's Fastest Indian", starring Anthony Hopkins.

Indian Motorcycle has a fantastic legacy, and our research proved that they are in a unique position to capitalize on their brand and position themselves into a market that allows them to regain an identity that has been lost, modified, and adjusted over the past 100 years.

This presentation is a simple and visual aid we used to tell the story of Indian Motorcycle and to make our recommendation.

Please note that there is a proposal for reduction of nigeria custom duty on imported car 2021 from 35% to 5% by the government to boost and reduce the transportation cost. As at the time of writing this report, it’s not clear whether this has been enforced by the customs. But once it’s implemented, the cost of imported vehicle will be greatly reduced.

Used Motorcycle - bike 2I bought my first used motorcycle while I was in college. It was a Honda 750. I road it around town and I took it on long trips. One summer I took it from my home state of Minnesota out to Wyoming, Montana and even up into Canada. The next summer I road it out to New Hampshire and eventually to Boston where I sold it and bought an old Jeep.

Onsite Motorcycle Inspection and Verification - Sample ReportGoose & Gander

WeGoLook.com is a nationwide service with over 7,400 agents who provide custom tasking, reporting, inspections, field services and more. Here is a sample motorcycle inspection report.

We completed an analysis of Indian Motorcycle's current situation since being acquired by Polaris. We completed market research, conducted interviews with Indian fanatics, collectors, dealers, etc., competitive analysis, and watched "The World's Fastest Indian", starring Anthony Hopkins.

Indian Motorcycle has a fantastic legacy, and our research proved that they are in a unique position to capitalize on their brand and position themselves into a market that allows them to regain an identity that has been lost, modified, and adjusted over the past 100 years.

This presentation is a simple and visual aid we used to tell the story of Indian Motorcycle and to make our recommendation.

Please note that there is a proposal for reduction of nigeria custom duty on imported car 2021 from 35% to 5% by the government to boost and reduce the transportation cost. As at the time of writing this report, it’s not clear whether this has been enforced by the customs. But once it’s implemented, the cost of imported vehicle will be greatly reduced.

2. VALUATION OF USED VEHICLES

For the purpose of levying taxes the value of a vehicle shall

be deemed to be the Home Delivery Value depreciated as

below plus the Freight and Insurance as stipulated under

section 90 of PNDC LAW 330, 1993.

A. Where the age of a used motor

vehicle does not exceed six

- The price shall be deemed to

be the first Purchase Price

months.

B. Where the age exceeds six

months but does not exceed

one and a half years.

- Eighty five per centum of the

first Purchase Price

C. Where the age exceeds one and

a half years but does not

exceed two and a half years.

- Seventy per centum of the

first Purchase Price

D. Where the age exceeds two

and a half years but does not

exceed five years.

- Sixty per centum of the first

Purchase Price

E. Where the age exceeds five years - Fifty per centum of Purchase

Price

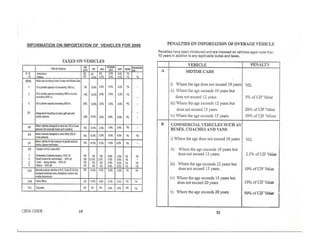

VEHICLE

NIL

5% of CIF Value

10% of CIF Value

30% of CIF Value

COMMERCIAL VEHICLES SUCH

AS TRUCKS, LORRIES AND

TIPPER TRUCKS

i) Where the age does not exceed 10 years

ii) Where the age exceeds 10 years but does

not exceed 12 years.

iii) Where the age exceeds 12 years but does

not exceed 22 years.

iv) Where the age exceeds 22 years.

C

PENALTY

PLEASE NOTE THAT:

• The age of a motor vehicle shall be calculated from the year in which

the vehicle was first manufactured.

• No person shall import a right-hand steering motor vehicle into the

country unless otherwise authorized by the Minister of Finance.

• Under the current Law (Act 634) any vehicle that remains unentered

and uncleared within 60 days after discharge or in the case of overland

vehicle, from the date it crossed the national border into Ghana shall still

be forfeited to the state.

12