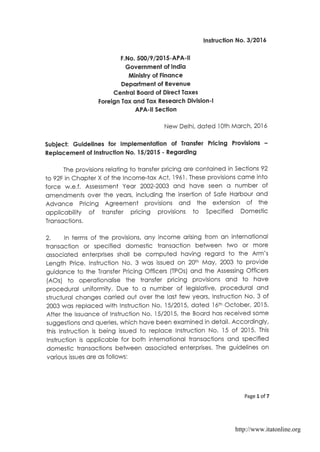

CBDT guidelines for implementation of transfer pricing provisions

•

0 likes•187 views

Income Tax Notifications and Circulars

Report

Share

Report

Share

Download to read offline

Recommended

PS16 from Rage Mobiles

Introducing "PS16" By Rage Mobiles, with Exciting Features.

Now be Smart with Smart Colors of "PS16" By Rage Mobiles.

Shop here: http://www.rage-mobile.com/Rage-Feature-Phones/PowerSlim-Series/Rage-PS16

Rapid from Rage Mobiles

The All-New Rapid.

Carry Your World in Your Pocket!

Introducing the all-new Rapid - the Android Kitkat IPS display smartphone at the smartest possible price.

Shop Here: http://goo.gl/6w8ith

Bravo+ from Rage Mobiles

The All-New Rage Bravo+. Now Bravo+ gives you more features than you expected: a bigger battery and a 16GB expandable memory slot.

A great value for price!

This new model has all the features that you expected. Plus more!

Rage Mobiles are available at multiple price points to cater to a wide spectrum of its customer needs.

Shop Now:

http://www.rage-mobile.com/Bravo-Plus

Rapid presentation

Carry Your World in Your Pocket!

Introducing the all-new Rapid - the Android Kitkat IPS display smartphone at the smartest possible price.

Notification 11 of 2016

The notification amends the Income Tax Rules of 1962. It substitutes rule 45 regarding the form of appeal to the Commissioner (Appeals). Appeals must now be filed using Form 35, which must be electronically filed and verified depending on how the taxpayer files their return. Form 35 collects personal information, details of the appealed order, pending appeals, appeal details, tax payments, statement of facts/grounds for appeal and additional evidence. The amended rules also specify the procedure for electronic filing and verification of Form 35.

U.S. Gandhi Budget 2015 - 2016 Analysis

The document provides information about a multi-disciplinary chartered accountancy firm, including details about its founding, vision, services offered, and team members.

It discusses the firm's founding in 1983 with a vision to provide advisory and support services to domestic and international businesses and organizations. It explains how the firm blends knowledge, analytics, quality assurance, and high-quality professionals to meet client needs.

Biographies are provided for the founder and managing partner and another partner, outlining their specializations, experience, and roles within the firm.

Budget 2014 15 - An analysis

This document provides a summary of key proposals in the Indian Budget 2014-2015 relating to direct taxes, transfer pricing, international taxation, indirect taxes, and other proposals. Some of the key points included are:

- No change in individual or corporate tax rates. Basic exemption limit increased for individuals and senior citizens. Deductions under section 80C and for housing loans increased.

- New investment allowance introduced for manufacturing companies investing over Rs. 25 crores.

- Changes introduced to alternate minimum tax calculations and restrictions on certain expense disallowances.

- Presumptive taxation amounts increased for certain businesses.

- Clarifications provided on taxation of foreign dividends, CSR contributions, and trading losses for

U.S.Gandhi Budget 2016 2017 analysis - Finance Bill 2016

U.S.Gandhi Budget 2016 2017 analysis Presentation - Finance Bill 2016 decoded, Budget Highlights & Flash

Recommended

PS16 from Rage Mobiles

Introducing "PS16" By Rage Mobiles, with Exciting Features.

Now be Smart with Smart Colors of "PS16" By Rage Mobiles.

Shop here: http://www.rage-mobile.com/Rage-Feature-Phones/PowerSlim-Series/Rage-PS16

Rapid from Rage Mobiles

The All-New Rapid.

Carry Your World in Your Pocket!

Introducing the all-new Rapid - the Android Kitkat IPS display smartphone at the smartest possible price.

Shop Here: http://goo.gl/6w8ith

Bravo+ from Rage Mobiles

The All-New Rage Bravo+. Now Bravo+ gives you more features than you expected: a bigger battery and a 16GB expandable memory slot.

A great value for price!

This new model has all the features that you expected. Plus more!

Rage Mobiles are available at multiple price points to cater to a wide spectrum of its customer needs.

Shop Now:

http://www.rage-mobile.com/Bravo-Plus

Rapid presentation

Carry Your World in Your Pocket!

Introducing the all-new Rapid - the Android Kitkat IPS display smartphone at the smartest possible price.

Notification 11 of 2016

The notification amends the Income Tax Rules of 1962. It substitutes rule 45 regarding the form of appeal to the Commissioner (Appeals). Appeals must now be filed using Form 35, which must be electronically filed and verified depending on how the taxpayer files their return. Form 35 collects personal information, details of the appealed order, pending appeals, appeal details, tax payments, statement of facts/grounds for appeal and additional evidence. The amended rules also specify the procedure for electronic filing and verification of Form 35.

U.S. Gandhi Budget 2015 - 2016 Analysis

The document provides information about a multi-disciplinary chartered accountancy firm, including details about its founding, vision, services offered, and team members.

It discusses the firm's founding in 1983 with a vision to provide advisory and support services to domestic and international businesses and organizations. It explains how the firm blends knowledge, analytics, quality assurance, and high-quality professionals to meet client needs.

Biographies are provided for the founder and managing partner and another partner, outlining their specializations, experience, and roles within the firm.

Budget 2014 15 - An analysis

This document provides a summary of key proposals in the Indian Budget 2014-2015 relating to direct taxes, transfer pricing, international taxation, indirect taxes, and other proposals. Some of the key points included are:

- No change in individual or corporate tax rates. Basic exemption limit increased for individuals and senior citizens. Deductions under section 80C and for housing loans increased.

- New investment allowance introduced for manufacturing companies investing over Rs. 25 crores.

- Changes introduced to alternate minimum tax calculations and restrictions on certain expense disallowances.

- Presumptive taxation amounts increased for certain businesses.

- Clarifications provided on taxation of foreign dividends, CSR contributions, and trading losses for

U.S.Gandhi Budget 2016 2017 analysis - Finance Bill 2016

U.S.Gandhi Budget 2016 2017 analysis Presentation - Finance Bill 2016 decoded, Budget Highlights & Flash

Controversies in taxation of real estate projects & ICDs for real estate deve...

The document discusses the appropriate method of revenue recognition for real estate developers under Indian tax laws. It provides an overview of the completed contract method and percentage of completion method and their tax implications. It also summarizes various judicial pronouncements related to the methods that can be followed by developers and the considerations of tax authorities. The key point discussed is that developers can follow either method for accounting but tax authorities prefer percentage of completion method and the accounting standards need to be considered for tax computation purposes.

STRESS URINARY INCONTINENCE

The document discusses urinary incontinence, specifically stress urinary incontinence (SUI). It defines SUI and describes its prevalence, types, grading, anatomical classification, and various pathophysiological theories. It discusses investigations for SUI including stress tests, urodynamic studies, and imaging. Management options covered include conservative approaches like pelvic floor exercises, medical therapies, intraurethral devices, and surgical interventions for SUI like anterior colporrhaphy and Burch colposuspension. The document also presents the Unani perspective on SUI, including causes, diagnosis, and treatments focused on addressing coldness, weakness of the bladder and its sphincters.

Simplification in Overseas Direct Investment Reporting

The Reserve Bank of India (RBI) has issued a circular rationalizing and revising the reporting of Overseas Direct Investment (ODI) forms. Key points:

1) Form ODI will now have 5 parts instead of 6 by subsuming Part II within Part I to capture all data pertaining to the Indian party undertaking ODI and related transactions.

2) New reporting formats have been introduced for venture capital funds, portfolio investments by mutual funds and alternate investment funds.

3) Online reporting of ODI forms has been introduced to reduce paper-based filing and allow faster reference and monitoring of overseas investment flows.

4) Strict timelines and processes have been established for online submission and

DIPP issues FAQ's on Start-up India Schemes

The document contains frequently asked questions and responses about registering as a startup in India.

It provides definitions for what qualifies as a startup and outlines the process for registration and obtaining recognition. Startups can register through the Startup India portal and mobile app and will receive a certificate of recognition. To receive additional tax and IP benefits, startups must obtain certification from an Inter-Ministerial Board.

The document also addresses questions for incubators and funding bodies about providing recommendation letters to support startup applications. Incubators and funds must meet certain criteria, and letters must validate the innovative nature and commercial potential of the startup's business.

20 key suggestions of Tax Reform Panel to Simplify tax provisions

The Tax Reform Panel provided 20 key suggestions to simplify India's tax provisions:

1. Provide legislative guidance on characterizing investments as capital assets or stock-in-trade to reduce litigation. Surplus on shares held over 1 year as capital assets would always be taxed as long-term capital gains.

2. Introduce a presumptive taxation scheme for professionals estimating income at 33.33% of receipts up to 1 crore rupees to simplify compliance.

3. Defer implementation of Income Computation and Disclosure Standards (ICDS) to allow further study of implications as they generate legal debates and increase compliance burden.

CBEC Clarifies 15 instances for service tax liability on services provided by...

This document provides clarification on issues regarding the levy of service tax on services provided by the government or a local authority to business entities. It addresses 15 issues, providing clarification on topics such as services provided between governments, services to individuals, taxes/fees/duties, fines/penalties, eligibility for service tax exemption based on the amount charged, CENVAT credit eligibility and documents required to claim the credit. Illustrations are provided on how CENVAT credit can be claimed over 3 years for service tax paid on one-time charges for assignment of rights to use natural resources.

Mca notifies-caro-2016-applicable-for-fy-beginning-on-or-after-april-1-2015

- The document is an order from the Ministry of Corporate Affairs in India establishing the Companies (Auditor's Report) Order, 2016, which specifies matters that must be addressed in audit reports for certain types of companies.

- It supersedes the previous Companies (Auditor's Report) Order from 2015 and applies to most types of companies except for things like banking, insurance, and some smaller private companies.

- The order lists 16 matters that must be included in the auditor's report, covering issues like maintenance of asset records, loans to other parties, statutory dues, fraud, and transactions with related parties.

Reputational risk in india

Reputational risk has become more prominent globally. In India, reputational risks in financial and other sectors have led to significant losses that are often much higher than direct financial losses. Events that can damage corporate and individual reputations in India include financial frauds, auditor or director resignations, loan defaults, transactions with politically exposed persons or involving conflicts of interest, and notices from government investigative agencies. Case studies found market capitalization declines after reputational events were much greater than direct financial losses, showing the high costs of reputational risk. Global investors, companies doing business in India, and others should monitor Indian corporations and individuals to detect early signs of potential reputational damage.

Amendments to rules for online process for lower/nil deduction certificate no...

This document provides details on proposed amendments to Form 13 and relevant rules in the Income Tax Rules, 1962 to rationalize and make the process of issuing certificates for no/lower tax deduction or collection electronic. Key points:

- The existing process for obtaining certificates is being amended to make it fully electronic by requiring Form 13 to be filed digitally.

- Several rules including rules 28, 28AA, 28AB, 37G and 37H are being amended to incorporate the electronic process and rationalize requirements.

- A draft of the proposed amendments detailing changes to each rule is provided.

- Stakeholder comments on the draft are invited by September 4th, 2018.

Amendments to rules for online process for lower/nil deduction certificate no...

The document is a draft notification from the Central Board of Direct Taxes in India proposing amendments to the Income Tax Rules of 1962 regarding making the process of issuing certificates for no or lower tax deduction/collection electronic. Key points:

- It proposes replacing the existing paper Form 13 with an electronic version to rationalize and streamline the process.

- It outlines amendments to various rules including 28, 28AA, 28AB, 37G and 37H to incorporate the electronic process and specify procedures for secure submission and processing.

- If approved, the changes would mandate electronic filing of Form 13 applications for tax deduction/collection certificates under a digital signature or verification code.

GST on TDR

Transferable Development Rights (TDRs) allow land owners who surrender land for public projects to receive additional development rights that can be used or sold. There is debate around whether trading of TDRs is taxable under GST. TDRs have been considered a "benefit arising from land" by courts, making them immovable property. The sale of land is excluded from GST under Schedule III. Since TDRs are a benefit of land, their trading could be considered outside the scope of GST. However, due to conflicting judgments, developers are advised to pay GST on TDR trades and apply for refund until the tax treatment is clarified.

GST Paper - GST on TDR

Transferable Development Rights (TDRs) allow land owners who surrender land for public projects to receive additional development rights that can be used or sold. There is debate around whether trading TDRs is taxable under GST. TDRs are considered a "benefit arising from land" and immovable property. However, the sale of land is excluded from GST. Judicial precedents indicate "land" includes rights associated with it. Since TDRs are a land benefit, their transfer may not be liable for GST. Until clarified, paying GST on TDR transfers is advisable to avoid potential non-compliance issues.

Gst Update - Draft New Simplified GST returns

The document summarizes key highlights of the new simplified GST returns approved by the GST Council. It outlines features of monthly and quarterly returns such as filing due dates, nil returns, invoices, input tax credit claims, amendments, and payments. It also describes simplified "Sahaj" and "Sugam" quarterly returns for small businesses with annual turnover up to Rs. 5 Cr dealing primarily in domestic supplies. Control measures are proposed for newly registered taxpayers and defaulters regarding invoice uploading.

Summary of Key Changes in ITR Form for FY 2017-18 (AY 2018 19)

The document summarizes key changes to Indian income tax return (ITR) forms for the 2018-19 assessment year. Some of the major changes include:

- ITR-1 can now only be filed by individuals with income up to Rs. 50 lakh instead of Rs. 5 lakh. Non-resident Indians must now use ITR-2.

- Additional details must be provided for deductions, allowances, perquisites, capital gains, foreign income and assets, GST payments, and donations.

- Companies must provide more details on accounting, CSR spending, foreign transactions, and beneficial owners.

- Political parties must disclose any cash donations over Rs. 2,000. Charitable trusts face

Taxation on Share Premium

The issue of taxation on share premium has been of major tax controversy over the past few years and has rightly taxed money launderers and unearthed sham transactions. At the same time it has created hardships for start-ups and corporates in their fund raising and restructuring transactions.

Union Budget Analysis 2017-18 | U.S.Gandhi & Co

The document provides an overview of key proposals in India's Union Budget for 2017-18. Some highlights include:

- Personal income tax rates remain largely unchanged, except the 5-10% slab is reduced to 5%. A rebate of Rs. 2,500 is available for income up to Rs. 3.5 lakhs.

- Corporate tax rate is reduced to 25% for companies with turnover up to Rs. 50 crores.

- Capital gains holding period for immovable property is reduced to 2 years from 3 years.

- Presumptive income scheme threshold increased and cash transaction limits introduced.

- Changes introduced for start-ups, MAT credits, and international taxation provisions.

Acceptance of Cash Over the Counter

The Reserve Bank of India (RBI) issued a circular to all scheduled commercial banks regarding accepting cash deposits over the counter from declarants of the Income Declaration Scheme 2016. The circular instructs banks to accept cash deposits of any amount over the counter from declarants paying their tax dues in cash under the Scheme. Banks must comply with Know Your Customer requirements but cannot refuse large cash deposits for this purpose. The RBI advises banks to immediately inform branches to accept cash from declarants without difficulty to deposit their tax dues under the Scheme.

Q&A on the income declaration scheme, 2016

The document is a circular from the Central Board of Direct Taxes clarifying questions about India's Income Declaration Scheme 2016. It provides answers to 14 questions on various aspects of the scheme, such as eligibility, capital gains tax treatment of declared assets, consequences of failing to declare income, and confidentiality of declarations. Key points addressed include that declarants will pay a total of 45% tax on declared income, capital gains will be computed from fair market value of declared assets as of June 1, 2016, and declarations will remain confidential like tax returns.

RBI permits foreign venture capital investors to invest in startups

This document contains amendments made to the Foreign Exchange Management (Transfer or Issue of Security by a Person Resident outside India) Regulations, 2000 by the Reserve Bank of India. The key amendments include inserting new definitions for Category I Alternative Investment Fund and startup, substituting provisions related to investment by registered Foreign Venture Capital Investors, and substituting Schedule 6 which outlines the terms of investment by registered Foreign Venture Capital Investors. The amendments allow Foreign Venture Capital Investors greater flexibility in investing in startups and Category I Alternative Investment Funds in India.

Government orders investigation against 187 companies involved in collection ...

The Ministry of Corporate Affairs has ordered investigations through the Serious Fraud Investigation Office (SFIO) into 187 companies accused of collecting funds through illegal Ponzi schemes. The government is committed to tackling Ponzi schemes and protecting investors. Measures taken include introducing 'fraud' as an offence under the Companies Act 2013, granting statutory status to SFIO, and increasing technology use to identify fraud cases. An annex lists the 187 companies under investigation.

Government constitutes SIT on Panama Papers Leaks

The government of India constituted a multi-agency group in April 2016 to investigate Indian persons named in the Panama Papers leaks regarding undisclosed foreign assets. The group includes officers from the Central Board of Direct Taxes, Enforcement Directorate, Financial Intelligence Unit, and Reserve Bank of India. The investigation team has been ordered to conduct a time-bound inquiry. The government has also taken steps to expedite the investigation through increased international cooperation. However, the investigation is still preliminary and the International Consortium of Investigative Journalists has noted that not everyone in the Panama Papers is necessarily involved in tax evasion. Further actions will depend on the outcome of the investigation.

Government permits 100% FDI in marketplace based model of e-commerce

Income Tax Notifications and Circulars

More Related Content

Viewers also liked

Controversies in taxation of real estate projects & ICDs for real estate deve...

The document discusses the appropriate method of revenue recognition for real estate developers under Indian tax laws. It provides an overview of the completed contract method and percentage of completion method and their tax implications. It also summarizes various judicial pronouncements related to the methods that can be followed by developers and the considerations of tax authorities. The key point discussed is that developers can follow either method for accounting but tax authorities prefer percentage of completion method and the accounting standards need to be considered for tax computation purposes.

STRESS URINARY INCONTINENCE

The document discusses urinary incontinence, specifically stress urinary incontinence (SUI). It defines SUI and describes its prevalence, types, grading, anatomical classification, and various pathophysiological theories. It discusses investigations for SUI including stress tests, urodynamic studies, and imaging. Management options covered include conservative approaches like pelvic floor exercises, medical therapies, intraurethral devices, and surgical interventions for SUI like anterior colporrhaphy and Burch colposuspension. The document also presents the Unani perspective on SUI, including causes, diagnosis, and treatments focused on addressing coldness, weakness of the bladder and its sphincters.

Simplification in Overseas Direct Investment Reporting

The Reserve Bank of India (RBI) has issued a circular rationalizing and revising the reporting of Overseas Direct Investment (ODI) forms. Key points:

1) Form ODI will now have 5 parts instead of 6 by subsuming Part II within Part I to capture all data pertaining to the Indian party undertaking ODI and related transactions.

2) New reporting formats have been introduced for venture capital funds, portfolio investments by mutual funds and alternate investment funds.

3) Online reporting of ODI forms has been introduced to reduce paper-based filing and allow faster reference and monitoring of overseas investment flows.

4) Strict timelines and processes have been established for online submission and

DIPP issues FAQ's on Start-up India Schemes

The document contains frequently asked questions and responses about registering as a startup in India.

It provides definitions for what qualifies as a startup and outlines the process for registration and obtaining recognition. Startups can register through the Startup India portal and mobile app and will receive a certificate of recognition. To receive additional tax and IP benefits, startups must obtain certification from an Inter-Ministerial Board.

The document also addresses questions for incubators and funding bodies about providing recommendation letters to support startup applications. Incubators and funds must meet certain criteria, and letters must validate the innovative nature and commercial potential of the startup's business.

20 key suggestions of Tax Reform Panel to Simplify tax provisions

The Tax Reform Panel provided 20 key suggestions to simplify India's tax provisions:

1. Provide legislative guidance on characterizing investments as capital assets or stock-in-trade to reduce litigation. Surplus on shares held over 1 year as capital assets would always be taxed as long-term capital gains.

2. Introduce a presumptive taxation scheme for professionals estimating income at 33.33% of receipts up to 1 crore rupees to simplify compliance.

3. Defer implementation of Income Computation and Disclosure Standards (ICDS) to allow further study of implications as they generate legal debates and increase compliance burden.

CBEC Clarifies 15 instances for service tax liability on services provided by...

This document provides clarification on issues regarding the levy of service tax on services provided by the government or a local authority to business entities. It addresses 15 issues, providing clarification on topics such as services provided between governments, services to individuals, taxes/fees/duties, fines/penalties, eligibility for service tax exemption based on the amount charged, CENVAT credit eligibility and documents required to claim the credit. Illustrations are provided on how CENVAT credit can be claimed over 3 years for service tax paid on one-time charges for assignment of rights to use natural resources.

Mca notifies-caro-2016-applicable-for-fy-beginning-on-or-after-april-1-2015

- The document is an order from the Ministry of Corporate Affairs in India establishing the Companies (Auditor's Report) Order, 2016, which specifies matters that must be addressed in audit reports for certain types of companies.

- It supersedes the previous Companies (Auditor's Report) Order from 2015 and applies to most types of companies except for things like banking, insurance, and some smaller private companies.

- The order lists 16 matters that must be included in the auditor's report, covering issues like maintenance of asset records, loans to other parties, statutory dues, fraud, and transactions with related parties.

Viewers also liked (7)

Controversies in taxation of real estate projects & ICDs for real estate deve...

Controversies in taxation of real estate projects & ICDs for real estate deve...

Simplification in Overseas Direct Investment Reporting

Simplification in Overseas Direct Investment Reporting

20 key suggestions of Tax Reform Panel to Simplify tax provisions

20 key suggestions of Tax Reform Panel to Simplify tax provisions

CBEC Clarifies 15 instances for service tax liability on services provided by...

CBEC Clarifies 15 instances for service tax liability on services provided by...

Mca notifies-caro-2016-applicable-for-fy-beginning-on-or-after-april-1-2015

Mca notifies-caro-2016-applicable-for-fy-beginning-on-or-after-april-1-2015

More from Kunal Gandhi

Reputational risk in india

Reputational risk has become more prominent globally. In India, reputational risks in financial and other sectors have led to significant losses that are often much higher than direct financial losses. Events that can damage corporate and individual reputations in India include financial frauds, auditor or director resignations, loan defaults, transactions with politically exposed persons or involving conflicts of interest, and notices from government investigative agencies. Case studies found market capitalization declines after reputational events were much greater than direct financial losses, showing the high costs of reputational risk. Global investors, companies doing business in India, and others should monitor Indian corporations and individuals to detect early signs of potential reputational damage.

Amendments to rules for online process for lower/nil deduction certificate no...

This document provides details on proposed amendments to Form 13 and relevant rules in the Income Tax Rules, 1962 to rationalize and make the process of issuing certificates for no/lower tax deduction or collection electronic. Key points:

- The existing process for obtaining certificates is being amended to make it fully electronic by requiring Form 13 to be filed digitally.

- Several rules including rules 28, 28AA, 28AB, 37G and 37H are being amended to incorporate the electronic process and rationalize requirements.

- A draft of the proposed amendments detailing changes to each rule is provided.

- Stakeholder comments on the draft are invited by September 4th, 2018.

Amendments to rules for online process for lower/nil deduction certificate no...

The document is a draft notification from the Central Board of Direct Taxes in India proposing amendments to the Income Tax Rules of 1962 regarding making the process of issuing certificates for no or lower tax deduction/collection electronic. Key points:

- It proposes replacing the existing paper Form 13 with an electronic version to rationalize and streamline the process.

- It outlines amendments to various rules including 28, 28AA, 28AB, 37G and 37H to incorporate the electronic process and specify procedures for secure submission and processing.

- If approved, the changes would mandate electronic filing of Form 13 applications for tax deduction/collection certificates under a digital signature or verification code.

GST on TDR

Transferable Development Rights (TDRs) allow land owners who surrender land for public projects to receive additional development rights that can be used or sold. There is debate around whether trading of TDRs is taxable under GST. TDRs have been considered a "benefit arising from land" by courts, making them immovable property. The sale of land is excluded from GST under Schedule III. Since TDRs are a benefit of land, their trading could be considered outside the scope of GST. However, due to conflicting judgments, developers are advised to pay GST on TDR trades and apply for refund until the tax treatment is clarified.

GST Paper - GST on TDR

Transferable Development Rights (TDRs) allow land owners who surrender land for public projects to receive additional development rights that can be used or sold. There is debate around whether trading TDRs is taxable under GST. TDRs are considered a "benefit arising from land" and immovable property. However, the sale of land is excluded from GST. Judicial precedents indicate "land" includes rights associated with it. Since TDRs are a land benefit, their transfer may not be liable for GST. Until clarified, paying GST on TDR transfers is advisable to avoid potential non-compliance issues.

Gst Update - Draft New Simplified GST returns

The document summarizes key highlights of the new simplified GST returns approved by the GST Council. It outlines features of monthly and quarterly returns such as filing due dates, nil returns, invoices, input tax credit claims, amendments, and payments. It also describes simplified "Sahaj" and "Sugam" quarterly returns for small businesses with annual turnover up to Rs. 5 Cr dealing primarily in domestic supplies. Control measures are proposed for newly registered taxpayers and defaulters regarding invoice uploading.

Summary of Key Changes in ITR Form for FY 2017-18 (AY 2018 19)

The document summarizes key changes to Indian income tax return (ITR) forms for the 2018-19 assessment year. Some of the major changes include:

- ITR-1 can now only be filed by individuals with income up to Rs. 50 lakh instead of Rs. 5 lakh. Non-resident Indians must now use ITR-2.

- Additional details must be provided for deductions, allowances, perquisites, capital gains, foreign income and assets, GST payments, and donations.

- Companies must provide more details on accounting, CSR spending, foreign transactions, and beneficial owners.

- Political parties must disclose any cash donations over Rs. 2,000. Charitable trusts face

Taxation on Share Premium

The issue of taxation on share premium has been of major tax controversy over the past few years and has rightly taxed money launderers and unearthed sham transactions. At the same time it has created hardships for start-ups and corporates in their fund raising and restructuring transactions.

Union Budget Analysis 2017-18 | U.S.Gandhi & Co

The document provides an overview of key proposals in India's Union Budget for 2017-18. Some highlights include:

- Personal income tax rates remain largely unchanged, except the 5-10% slab is reduced to 5%. A rebate of Rs. 2,500 is available for income up to Rs. 3.5 lakhs.

- Corporate tax rate is reduced to 25% for companies with turnover up to Rs. 50 crores.

- Capital gains holding period for immovable property is reduced to 2 years from 3 years.

- Presumptive income scheme threshold increased and cash transaction limits introduced.

- Changes introduced for start-ups, MAT credits, and international taxation provisions.

Acceptance of Cash Over the Counter

The Reserve Bank of India (RBI) issued a circular to all scheduled commercial banks regarding accepting cash deposits over the counter from declarants of the Income Declaration Scheme 2016. The circular instructs banks to accept cash deposits of any amount over the counter from declarants paying their tax dues in cash under the Scheme. Banks must comply with Know Your Customer requirements but cannot refuse large cash deposits for this purpose. The RBI advises banks to immediately inform branches to accept cash from declarants without difficulty to deposit their tax dues under the Scheme.

Q&A on the income declaration scheme, 2016

The document is a circular from the Central Board of Direct Taxes clarifying questions about India's Income Declaration Scheme 2016. It provides answers to 14 questions on various aspects of the scheme, such as eligibility, capital gains tax treatment of declared assets, consequences of failing to declare income, and confidentiality of declarations. Key points addressed include that declarants will pay a total of 45% tax on declared income, capital gains will be computed from fair market value of declared assets as of June 1, 2016, and declarations will remain confidential like tax returns.

RBI permits foreign venture capital investors to invest in startups

This document contains amendments made to the Foreign Exchange Management (Transfer or Issue of Security by a Person Resident outside India) Regulations, 2000 by the Reserve Bank of India. The key amendments include inserting new definitions for Category I Alternative Investment Fund and startup, substituting provisions related to investment by registered Foreign Venture Capital Investors, and substituting Schedule 6 which outlines the terms of investment by registered Foreign Venture Capital Investors. The amendments allow Foreign Venture Capital Investors greater flexibility in investing in startups and Category I Alternative Investment Funds in India.

Government orders investigation against 187 companies involved in collection ...

The Ministry of Corporate Affairs has ordered investigations through the Serious Fraud Investigation Office (SFIO) into 187 companies accused of collecting funds through illegal Ponzi schemes. The government is committed to tackling Ponzi schemes and protecting investors. Measures taken include introducing 'fraud' as an offence under the Companies Act 2013, granting statutory status to SFIO, and increasing technology use to identify fraud cases. An annex lists the 187 companies under investigation.

Government constitutes SIT on Panama Papers Leaks

The government of India constituted a multi-agency group in April 2016 to investigate Indian persons named in the Panama Papers leaks regarding undisclosed foreign assets. The group includes officers from the Central Board of Direct Taxes, Enforcement Directorate, Financial Intelligence Unit, and Reserve Bank of India. The investigation team has been ordered to conduct a time-bound inquiry. The government has also taken steps to expedite the investigation through increased international cooperation. However, the investigation is still preliminary and the International Consortium of Investigative Journalists has noted that not everyone in the Panama Papers is necessarily involved in tax evasion. Further actions will depend on the outcome of the investigation.

Government permits 100% FDI in marketplace based model of e-commerce

Income Tax Notifications and Circulars

Proposal For Equalization Levy On Specified Transactions

This document proposes an "Equalization Levy" on specified digital transactions to address tax challenges arising from new digital business models. It summarizes the work of a committee examining taxation of the digital economy. The committee noted that existing international tax rules based on physical presence are outdated for digital businesses. It recommends adopting an Equalization Levy of 6-8% on large digital transactions over Rs. 1 lakh to source jurisdictions, to be imposed separately from income tax. This would help address unfair tax avoidance by digital multinationals and their competitive advantage over Indian businesses.

Taxman gets platform to track manipulation in penny stocks

The document discusses a new functionality added to the Individual Transaction Screen (ITS) for assessing officers. The functionality displays information related to transactions in penny stocks that were artificially manipulated. The Kolkata Investigation Directorate conducted an investigation into several penny stock companies and identified cases of bogus long term capital gains and short term capital losses claimed by taxpayers. Based on this investigation, details of taxpayers involved in such manipulative transactions have now been uploaded for assessing officers to examine when finalizing assessments or considering reopening past cases. Assessing officers are directed to access this new "Penny Stock" functionality and consider the available information.

CBDT issues guidelines for stay of demand at the first appeal stage

This document modifies guidelines for granting stays of tax demands during the first appeal stage. It provides that assessing officers shall grant a stay of demand until the disposal of the first appeal if the assessee pays 15% of the disputed demand. It allows assessing officers to require higher or lower payments if certain conditions are met, and establishes a process for administrative review. Assessing officers must dispose of stay petitions within 2 weeks and attach conditions like cooperating in the appeal and reserving the right to review or adjust refunds against the demand.

More from Kunal Gandhi (19)

Amendments to rules for online process for lower/nil deduction certificate no...

Amendments to rules for online process for lower/nil deduction certificate no...

Amendments to rules for online process for lower/nil deduction certificate no...

Amendments to rules for online process for lower/nil deduction certificate no...

Summary of Key Changes in ITR Form for FY 2017-18 (AY 2018 19)

Summary of Key Changes in ITR Form for FY 2017-18 (AY 2018 19)

RBI permits foreign venture capital investors to invest in startups

RBI permits foreign venture capital investors to invest in startups

Government orders investigation against 187 companies involved in collection ...

Government orders investigation against 187 companies involved in collection ...

Government permits 100% FDI in marketplace based model of e-commerce

Government permits 100% FDI in marketplace based model of e-commerce

Proposal For Equalization Levy On Specified Transactions

Proposal For Equalization Levy On Specified Transactions

Taxman gets platform to track manipulation in penny stocks

Taxman gets platform to track manipulation in penny stocks

CBDT issues guidelines for stay of demand at the first appeal stage

CBDT issues guidelines for stay of demand at the first appeal stage