Download as PDF, PPTX

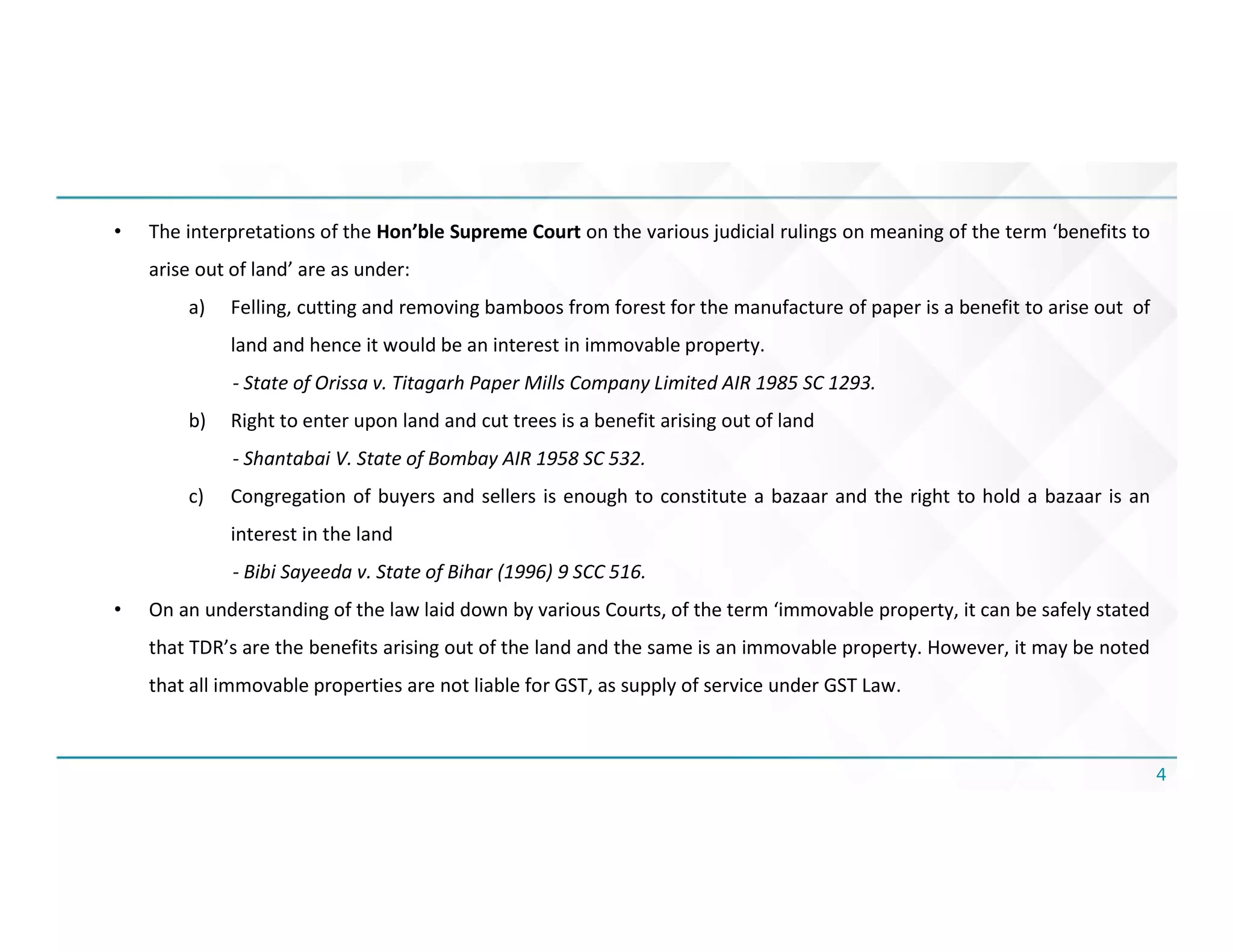

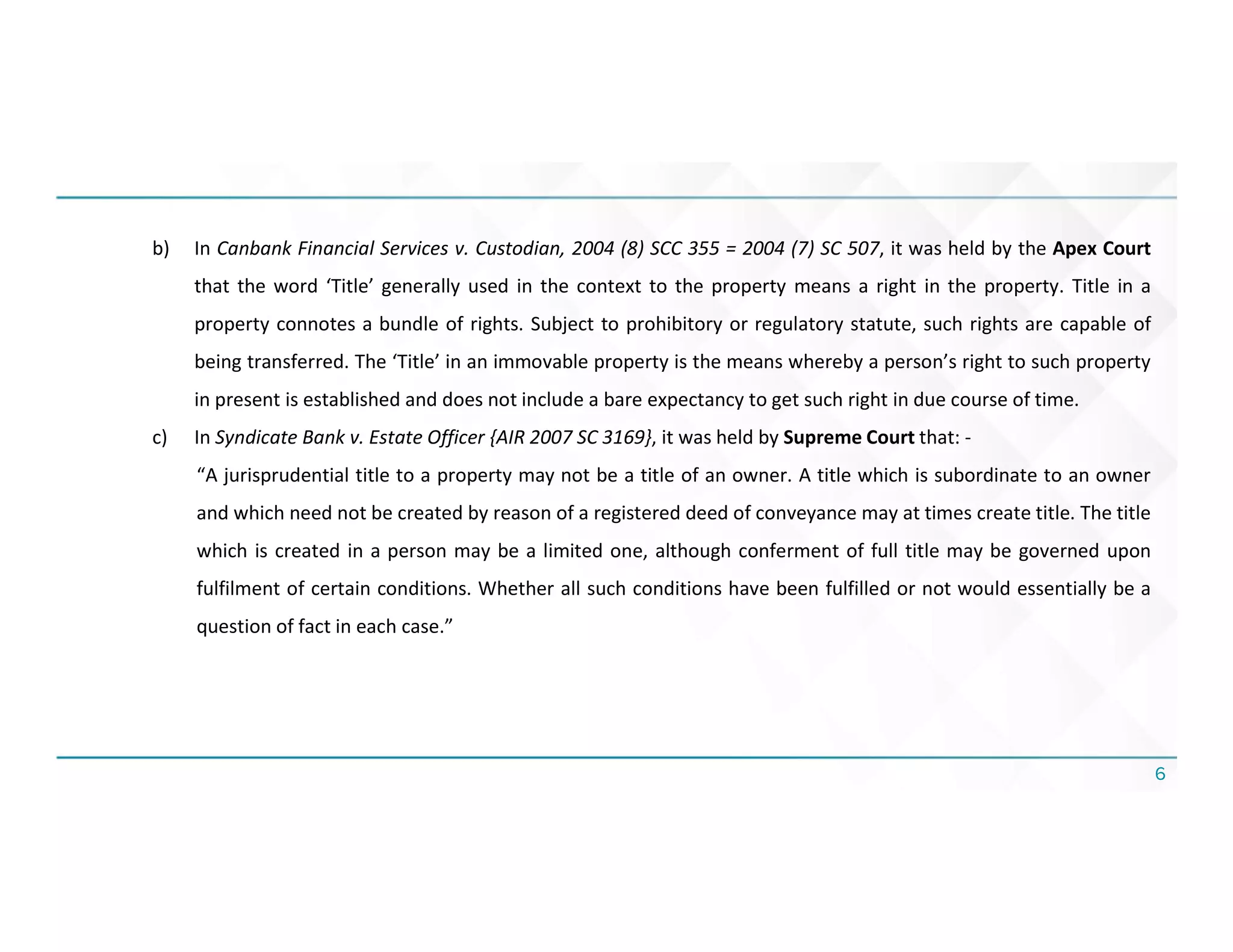

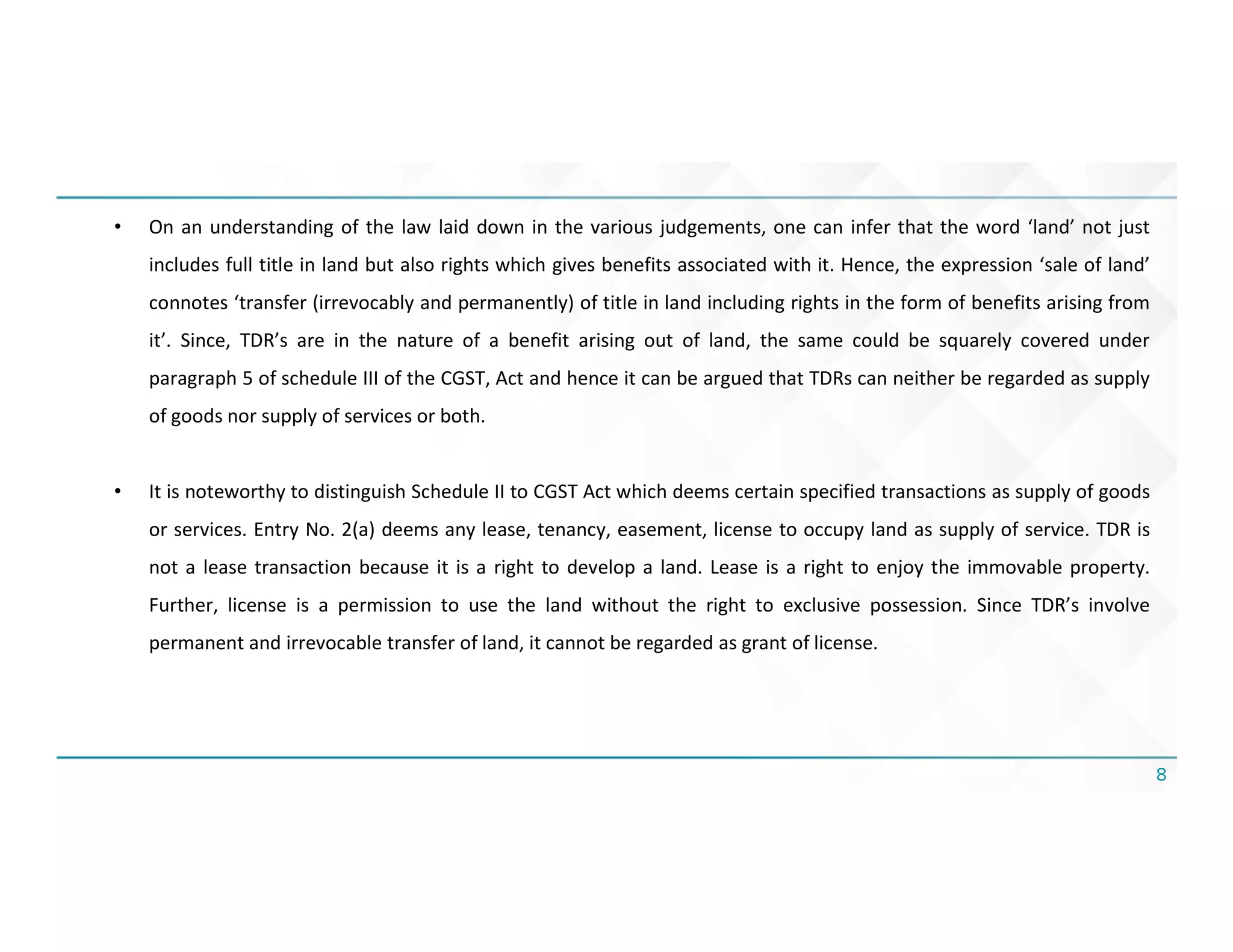

Transferable Development Rights (TDRs) allow land owners who surrender land for public projects to receive additional development rights that can be used or sold. There is debate around whether trading of TDRs is taxable under GST. TDRs have been considered a "benefit arising from land" by courts, making them immovable property. The sale of land is excluded from GST under Schedule III. Since TDRs are a benefit of land, their trading could be considered outside the scope of GST. However, due to conflicting judgments, developers are advised to pay GST on TDR trades and apply for refund until the tax treatment is clarified.