Download as PDF, PPTX

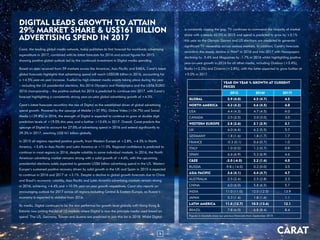

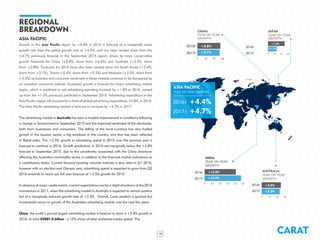

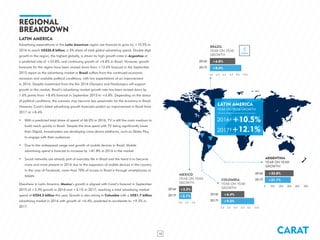

Carat's latest global advertising expenditure forecasts show that advertising spend will increase 4.5% in 2016 to reach $538 billion, driven by major events like the US elections. The growth rate is expected to continue into 2017. Digital advertising continues to be the fastest growing segment and will account for 29.3% of total advertising spend in 2017. While economic uncertainties lowered forecasts for some regions, most markets are still expected to see growth in 2016 and 2017, led by a strong US market and recovery in Western Europe. Digital media, especially mobile, online video and social media, will continue fueling the global expansion of advertising expenditures.