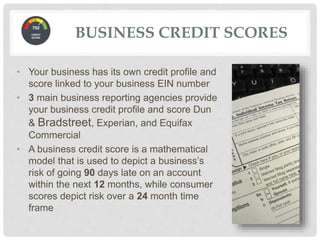

The document provides an overview of business credit scores, explaining how they are generated by major reporting agencies like Dun & Bradstreet, Experian, and Equifax, and their significance for business financing and risk assessment. It outlines different scoring models such as Paydex scores, Intelliscore, and FICO SBSS scores, detailing how they reflect a business's creditworthiness based on payment history and financial data. The absence of regulations similar to the Fair Credit Reporting Act in the consumer sector means business credit profiles are accessible to anyone without permission.