The document discusses valuation of bonds and stocks. It provides information on bond features such as coupon payments, face value, maturity date, and default. It also discusses how to value pure discount bonds, level-coupon bonds, and how bond prices relate to market interest rates for discount, premium, and par bonds. Examples are provided on calculating bond values, yields to maturity, and the yield curve using a financial calculator.

![5

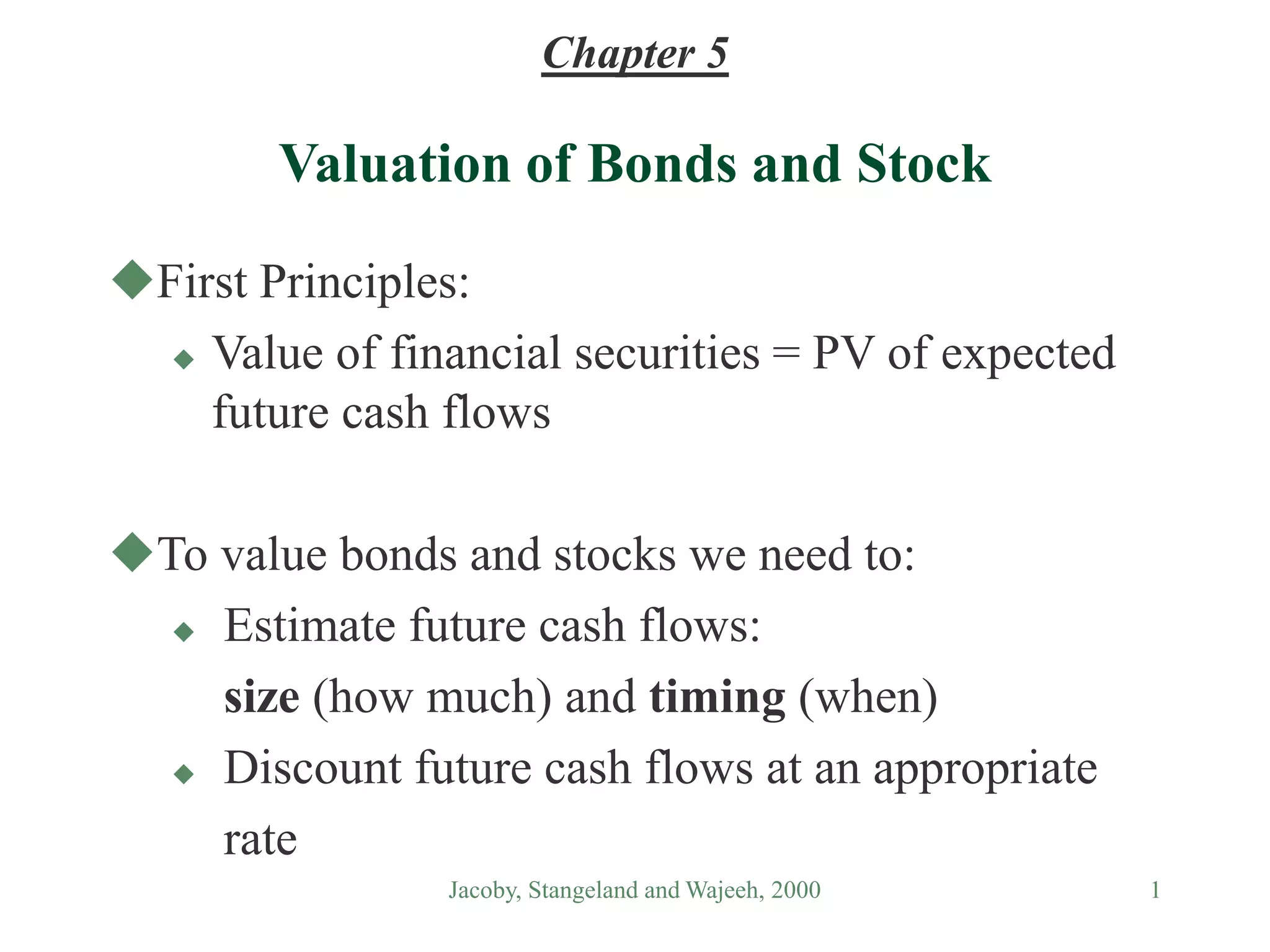

Level-Coupon Bonds

Information needed to value level-coupon bonds:

Coupon payment dates and Time to maturity (T)

Coupon (C) per payment period and Face value (F)

Discount rate

0 1 2 … T

|----------------|------------------|------- … ------|

Coupon Coupon Coupon + F

Value of a Level-coupon bond:

PV= C/(1+r) + C/(1+r)2 + .. + C/(1+r)T + F/(1+r)T

= C (1/r){1 - [1 / (1 + r)T]} + F/(1 + r)T

= PV of coupon payments + PV of face value](https://image.slidesharecdn.com/bondvaluation-221114085657-ee88e1bd/75/bond-valuation-ppt-5-2048.jpg)

![6

Example - Coupon Bonds

Q1. Consider a coupon bond paying a 4% coupon rate annually, with a

face value of $1,000, maturing in 10 years. Suppose that the

appropriate discount rate is 6%. What is the current value of the bond?

A1. The time line:

Define:

c = annual coupon rate (%)

C = dollar periodic coupon payment = c%F

In the above example:

c = % C = c%F = = $

F = $ T = years r = %

Use the above PV equation to solve:

PV= C (1/r){1 - [1 / (1 + r)T]} + F/(1 + r)T

= 40(1/0.06){1 - [1 / (1.06)10]} + 1,000/(1.06)10 = $

0 1 2 9 10 (Years)

(r = 6%)

…](https://image.slidesharecdn.com/bondvaluation-221114085657-ee88e1bd/75/bond-valuation-ppt-6-2048.jpg)

![8

Example - Discount, Premium and Par Bonds

Q2. For the above coupon bond: when discount rate is 6% and

coupon rate is 4% (c < r), the value of the bond is $852.80, less

than its face value (PV < F). In this case we say that the bond is

priced at discount. Recalculate the PV of the above bond with

discount rates of 2% and 4%.

A2. r = 2%

We have: r = 2% < 4% = c.

Use the above PV equation to solve:

PV= C (1/r){1 - [1 / (1 + r)T]} + F/(1 + r)T

= 40(1/0.02){1 - [1 / (1.02)10]} + 1,000/(1.02)10 = $1,179.65

We see that when c > r, the bond is priced at premium (PV > F).

r = 4%

We have: r = c = 4%.

Use the above PV equation to solve:

PV= 40(1/0.04){1 - [1 / (1.04)10]} + 1,000/(1.04)10 = $1,000

We say that when c = r, the bond is priced at par (PV = F).](https://image.slidesharecdn.com/bondvaluation-221114085657-ee88e1bd/75/bond-valuation-ppt-8-2048.jpg)

![22

Example - Using the Term Structure

Q1. You observe the above spot rates for GofC zero-coupon bonds for

different maturities: 0r1 = 8%, 0r2 = 10%, and 0r3 = 12%. A zero-

coupon bond has a face value of $1,000 and maturity of 2 years.

What must be its price today?

A1. Since: (1+0r2)2 = (1+0r1)(1+1f2), we can use either spot rates or

forward rates (same result) to find B:

Q2. Assume that the Pure Expectations Hypothesis (PEH) holds, what do

you expect the bond price to be one year from today?

A2. One year from today, the bond will have one year remaining to

maturity. Based on the PEH:

expected spot rate for second year = 1f2

Thus, the expected bond price in a year is:

45

.

826

$

:

:

or

,

45

.

826

$

:

12037

.

1

08

.

1

000

,

1

)

1

)(

1

(

000

,

1

)

1

.

1

(

000

,

1

)

1

(

000

,

1

2

1

1

0

2

0

2

2

f

r

r

B

Forward

B

Spot

56

.

892

$

]

[ 12037

.

1

000

,

1

)

1

(

000

,

1

1 2

1

f

B

E

2

1r

E](https://image.slidesharecdn.com/bondvaluation-221114085657-ee88e1bd/75/bond-valuation-ppt-22-2048.jpg)

![23

II. Liquidity Premium Theory

If you invest for (t+1) years, you commit to reinvest in every

year after the 1st year, and thereby lose liquidity and ask

for a liquidity premium:

III. Augmented Expectations Theory

Combines the pure expectations theory with the liquidity premium theory:

Example - Suppose: 0r1 = 8% and 0r2 = 9%. By the Expectations Theory:

By the Liquidity Premium Theory, when L2 =1%, we get:

1f2= E[1r2] + L2. = E[1r2] + 1%

Both theories together, give:

1

1

1

1 )

1

(

over year

expected

rate

spot

t

t

t

t

t

t

L

r

E

L

t

f

2

1

2

1 r

E

f

)

1

(

08

.

1

09

.

1 2

1

2

f

)

01

.

0

1

(

08

.

1

09

.

1 2

1

2

r

E](https://image.slidesharecdn.com/bondvaluation-221114085657-ee88e1bd/75/bond-valuation-ppt-23-2048.jpg)

![Jacoby, Stangeland and Wajeeh, 2000 24

Shapes of the Term Structure under the Liquidity Premium Theory & the

Augmented Expectations Theory

The shape of the term structure depends on the magnitude of the premium:

when there exist constant expectations:

when there exist decreasing expectations:

%

t

f ``

f `

t

% f

E[trt+1]

L

E[trt+1]](https://image.slidesharecdn.com/bondvaluation-221114085657-ee88e1bd/75/bond-valuation-ppt-24-2048.jpg)

![Jacoby, Stangeland and Wajeeh, 2000 40

With the above data:

141.75 = 9.9/1.1 + 10.89/(11)2 + 11.979/(11)3 + P3/(1.1)3

Thus, the expected stock price in three years is P3 = 152.73225

Since, this price is given by:

P3 = D4/(r-g*) = [D3(1+g*)]/(r-g*)

We have

152.73225 =

Rearranging, we get:

g* = %](https://image.slidesharecdn.com/bondvaluation-221114085657-ee88e1bd/75/bond-valuation-ppt-40-2048.jpg)