Downloaded 37 times

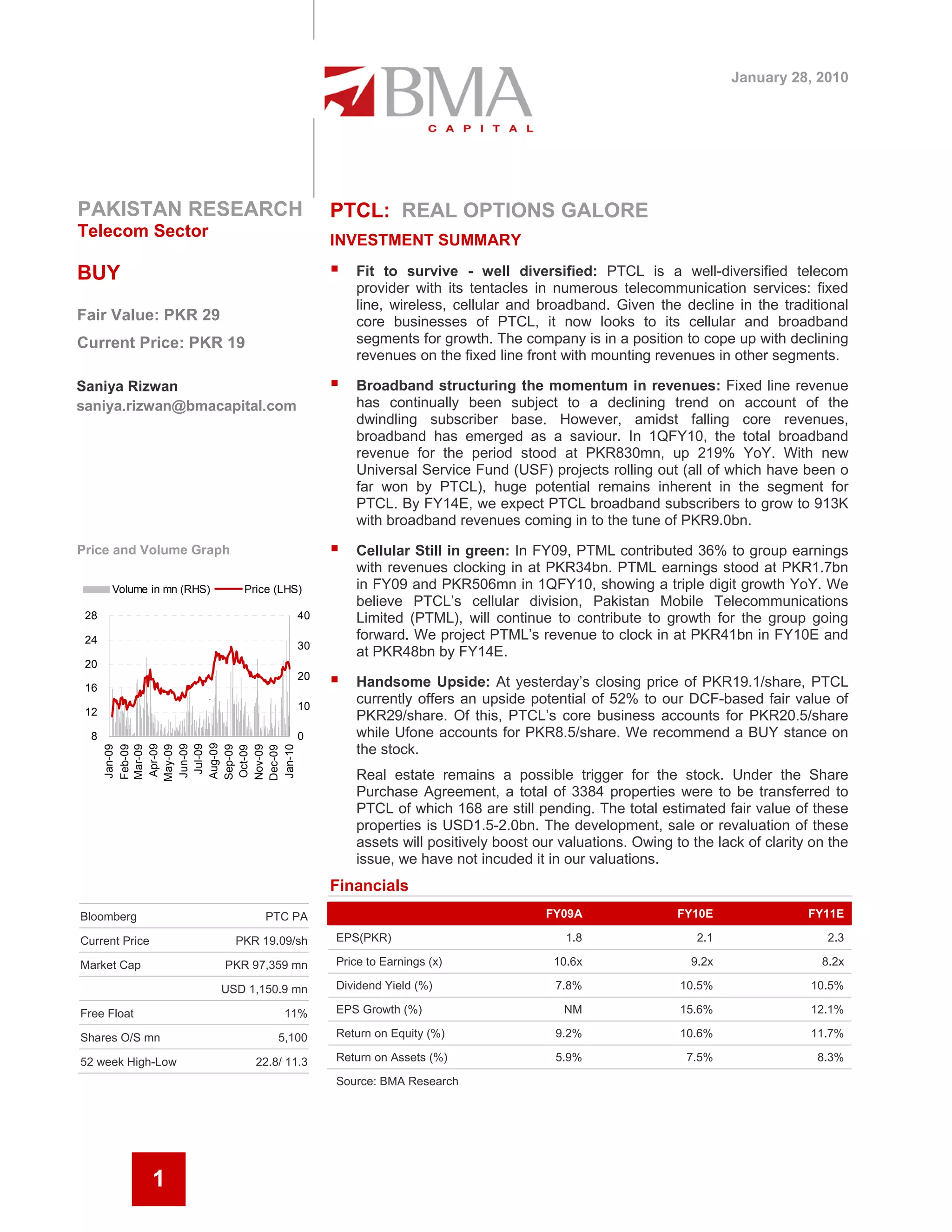

PTCL is a well-diversified telecom provider in Pakistan with operations in fixed line, wireless, cellular, and broadband services. While PTCL's traditional fixed line business is declining, its cellular and broadband segments are growing and contributing more to revenues. PTCL's broadband revenues have increased significantly, up 219% in 1QFY10, and broadband is expected to be a major driver of growth going forward. PTCL's cellular division PTML continues to be profitable and its revenues are projected to increase substantially through FY14E. At its current price, PTCL offers upside potential of 52% based on the analyst's fair value estimate, and is recommended as a buy.