Bizmanualz-CEO-Policies-and-Procedures-Series.pdf

•

0 likes•62 views

CEO Company Procedures Series This nine-manual set is a comprehensive set of procedures and forms that address every function of an organization and are essential to establish strong controls and manage your core processes. You will get nine MS-Word procedure manuals as listed below. Written by experts in the field, you will receive easily editable Microsoft Word format templates you can customize to fit your specific needs and you will enjoy a bundle discount of 45% off the list price... The newly updated CEO Procedure Manuals Series includes over 6,500 pages of content. It contains 373 prewritten procedures, 581 corresponding forms, Example Job Descriptions, sample policy manuals, and more.

Recommended

More Related Content

Similar to Bizmanualz-CEO-Policies-and-Procedures-Series.pdf

Similar to Bizmanualz-CEO-Policies-and-Procedures-Series.pdf (20)

Recently uploaded

Recently uploaded (10)

Bizmanualz-CEO-Policies-and-Procedures-Series.pdf

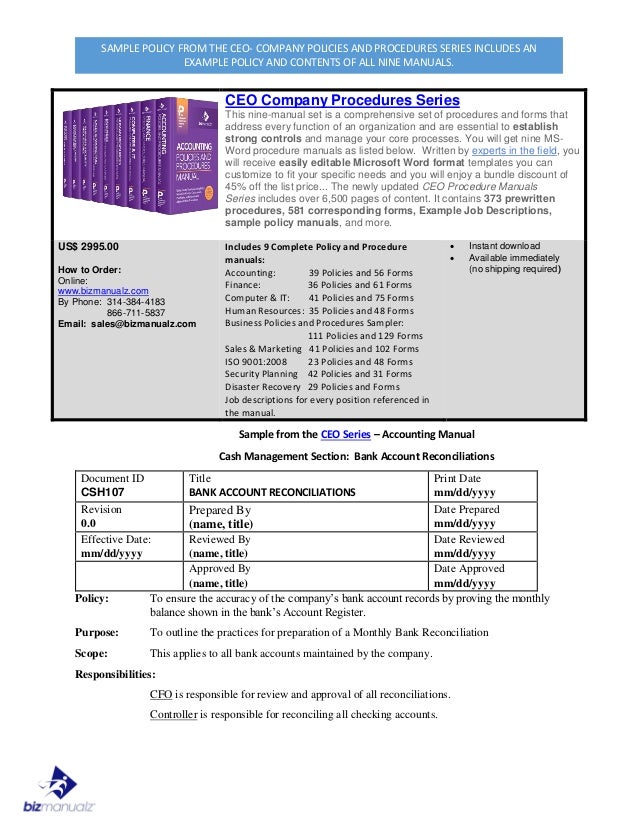

- 1. SAMPLE POLICY FROM THE CEO- COMPANY POLICIES AND PROCEDURES SERIES INCLUDES AN EXAMPLE POLICY AND CONTENTS OF ALL NINE MANUALS. CEO Company Procedures Series This nine-manual set is a comprehensive set of procedures and forms that address every function of an organization and are essential to establish strong controls and manage your core processes. You will get nine MS- Word procedure manuals as listed below. Written by experts in the field, you will receive easily editable Microsoft Word format templates you can customize to fit your specific needs and you will enjoy a bundle discount of 45% off the list price... The newly updated CEO Procedure Manuals Series includes over 6,500 pages of content. It contains 373 prewritten procedures, 581 corresponding forms, Example Job Descriptions, sample policy manuals, and more. US$ 2995.00 How to Order: Online: www.bizmanualz.com By Phone: 314-384-4183 866-711-5837 Email: sales@bizmanualz.com Includes 9 Complete Policy and Procedure manuals: Accounting: 39 Policies and 56 Forms Finance: 36 Policies and 61 Forms Computer & IT: 41 Policies and 75 Forms Human Resources: 35 Policies and 48 Forms Business Policies and Procedures Sampler: 111 Policies and 129 Forms Sales & Marketing 41 Policies and 102 Forms ISO 9001:2008 23 Policies and 48 Forms Security Planning 42 Policies and 31 Forms Disaster Recovery 29 Policies and Forms Job descriptions for every position referenced in the manual. Instant download Available immediately (no shipping required) Sample from the CEO Series – Accounting Manual Cash Management Section: Bank Account Reconciliations Document ID CSH107 Title BANK ACCOUNT RECONCILIATIONS Print Date mm/dd/yyyy Revision 0.0 Prepared By (name, title) Date Prepared mm/dd/yyyy Effective Date: mm/dd/yyyy Reviewed By (name, title) Date Reviewed mm/dd/yyyy Approved By (name, title) Date Approved mm/dd/yyyy Policy: To ensure the accuracy of the company’s bank account records by proving the monthly balance shown in the bank’s Account Register. Purpose: To outline the practices for preparation of a Monthly Bank Reconciliation Scope: This applies to all bank accounts maintained by the company. Responsibilities: CFO is responsible for review and approval of all reconciliations. Controller is responsible for reconciling all checking accounts.

- 2. SAMPLE POLICY FROM THE CEO- COMPANY POLICIES AND PROCEDURES SERIES INCLUDES AN EXAMPLE POLICY AND CONTENTS OF ALL NINE MANUALS. Background: Errors or omissions can be made to the company's bank account records due to the many cash transactions that occur. Therefore, it is necessary to prove the monthly balance shown in the bank account register. Cash on deposit with a bank is not available for count and is therefore proved through the preparation of a reconciliation of the company's record of cash in the bank and the bank's record of the company's cash that is on deposit. Definitions: Batch. All of the day’s credit card transactions are collected into a “batch” of transactions. The batch is closed, usually at the end of the day, and the result is submitted to the merchant processor as a single “batch”. Settlement. The processor clears the credit card transactions in the batch and the result is “settled” to the designated bank account. Settlement varies by Credit Card Company but usually occurs in 2-3 days after a batch is closed. Processor. The processor is responsible for authorizing credit card transactions and settling each batch. The processor is also the company that one must interface with on all discrepancies or “chargebacks”. Charge backs. A chargeback occurs when a customer (cardholder) disputes a charge that appears on their monthly credit card statement. If the dispute is unable to be resolved then the transaction is charged back to the merchant. The processor charges the merchant and returns the cardholder’s money. Procedure: 1.0 BANK STATEMENT PREPARATION 1.1 After receipt of the monthly bank statement, including cleared checks, deposit slips and any other transactions; the Controller should prepare the monthly bank reconciliation and have it carefully reviewed by the CFO. The CFO review is especially important if a bookkeeper is hired to perform other cash drawer or cash posting transactions. To preserve proper segregation of duties, no single employee, other than the owner, should perform both cash transaction functions and bank account reconciliations. 1.2 Prior to preparing the bank reconciliation, the accountant should review the bank statement for any interest credits, bank charges and other fees. These should all be posted to the checking account before reconciling. Note: some accounting systems allow for the entry of interest credits, bank charges and other fees during the reconciliation process. 2.0 COMPUTERIZED FORMAT 2.1 In the computerized environment, the accounting system may provide an automated bank reconciliation task. This task is generally selected once a month in conjunction with receiving the month end bank statement. Once selected, the screen shows a list of all items that have been posted to the cash account and that have not been cleared from the previous month's account reconciliation. The screen is usually divided into two segments: one half is a list of all checks and other charges reducing cash, and the other half is a list of all deposits and other items increasing cash. This screen would also have a field for entering the proper month end date and the balance at month end, per the bank. 2.2 After the account-reconciling task is successfully completed, a report is provided which shows the reconciliation process, including outstanding checks and deposits in transit. The actual format will vary depending on the accounting system, but in general, will

- 3. SAMPLE POLICY FROM THE CEO- COMPANY POLICIES AND PROCEDURES SERIES INCLUDES AN EXAMPLE POLICY AND CONTENTS OF ALL NINE MANUALS. contain the same information as shown on the manually prepared report in CSH107 Ex1 SAMPLE BANK AND BOOK BALANCES RECONCILIATION TO CORRECTED BALANCE. Note: Print out the full (not a summary) report, staple it to the applicable bank statement, and file the result as an important control feature. This will document that the bank statement has been successfully reconciled. 3.0 MANUAL PREPARATION AND RECONCILING ITEMS 3.1 A monthly bank reconciliation starts with the ending bank statement balance. List any deposits in transit that were made but were not yet recorded by the bank and add to the bank balance. Then, list any checks that were written on the account prior to month-end, but which have not yet cleared the bank and deducted from the bank balance. The ending balance should agree with the balance "per books", i.e.: the balance recorded in the checking account. 3.2 Now perform the same process with the monthly reconciliation of the ending balance per the company's books. Total deposits and total disbursements should be reconciled to the bank statement, then adjustments such as any interest or any other bank credit items should be listed and added to the balance. Then, any bank charges, transfer fees, etc. should be listed and deducted from the balance. From these steps, the "corrected" ending “book” balance is derived and should equal the "corrected" bank balance from the previous step. 3.3 Any discrepancies between the derived balance and the checkbook balance will require research to determine the cause, such as recording errors, omissions, incorrect postings, etc. In some cases, the discrepancy can be caused by not accurately entering all bank generated credits and charges; such as fees, interest, etc. If the balances still do not equal, the bank statement should be carefully reviewed for possible errors; such as, checks or deposits clearing for amounts that do not agree with those posted to the store's checking account. 4.0 COMPUTERIZED PREPARATION AND RECONCILING ITEMS 4.1 The same procedures as the manual tasks described above are followed in a computerized environment. The primary difference is in the ease of preparation. All transactions, which were not already cleared in the prior month’s reconciliation, are listed. 4.2 Start by checking or clicking off with the mouse or keyboard those transactions, (mainly checks and other debit memos, and deposits and other credit memos) that agree with the bank statement. Once all bank statement items have been found and clicked off on the screen, the remaining "un- cleared" entries on the screen are, in effect, the list of outstanding checks and deposits in transit. Furthermore, the screen typically provides a continually updating reconciled cash amount that should agree to the ending bank balance amount once all items are correctly accounted for and cleared. Usually the accounting system does the math and the screen displays both the ending bank balance and the reconciled cash amount with the remaining difference, if any. 4.3 Investigate all differences and enter any adjustments to the reconciliation or post to the cash account in order to ensure an accurate bank balance.

- 4. SAMPLE POLICY FROM THE CEO- COMPANY POLICIES AND PROCEDURES SERIES INCLUDES AN EXAMPLE POLICY AND CONTENTS OF ALL NINE MANUALS. 5.0 ADJUSTMENTS AND OTHER TROUBLESHOOTING 5.1 In spite of the best of efforts, the reconciliation result may not agree with the bank balance. The obvious first step is to make sure that all checks and deposits on the bank statement agree with the entries in the cash account. Discrepancies of this type are usually rare in computerized environments but may be caused by improperly recording manual checks or credit card deposits and fees. Checks are generally posted and printed simultaneously so that what shows up in the accounting system will always agree to what was processed through the bank. Deposits are another matter. The bank might group deposited checks differently than they were in the accounting system. As explained in more detail in procedure CSH101 CASH DRAWERS AND CREDIT CARDS. To simplify the month end reconciliation, receipts should be batched in a total deposit amount that agrees to both the accounting system and the bank. Make sure to print a totaled deposit report when daily receipts of checks and cash are batched for deposit. After making the bank deposit, staple the validated bank deposit slip to the deposit report. This will document the two events: 1) what was deposited per the accounting system, and 2) what was actually deposited in the bank. These two amounts must agree. This helps eliminate deposit errors for check and cash receipts. 5.2 A more difficult reconciling task is in obtaining agreement of all credit card receipts. The difficulty results from three unique situations. First, there is a time lag of several days between the time the credit card transaction occurred in the store and the time it is settled or deposited to the store's bank account. Second, depending on the type of credit card and/or the merchant provider, the fee charged (typically 1% to 4%) on each transaction may be automatically deducted from the deposit before it shows up on the bank statement. And third, “chargebacks” are usually deducted immediately by the processor and only reversed if the dispute is resolved in the company’s favor. This may even occur before the chargeback notice has arrived in the mail. Consequently, the deposit on the bank statement may not agree with the daily credit card batch (receipts). In the face of these difficulties, the CFO and Controller should thoroughly understand the particular credit card daily closing procedures. An end of day report for each credit card closing should be printed and saved as a reference for the month end reconciliation process. Alternatively, the credit card processor will provide a month-end statement listing each credit card “batch” submitted each day. This report can be used to reconcile the credit card batches to the settlement deposits. 5.3 After reconciling checks and deposits, the next area to reconcile are bank generated Credit and Debit memos. These can result from various events including, returned checks, returned check charges, monthly bank activity charges, credit card merchant fees, charges from the use of debit cards, interest income and other service charges. The CFO may not know many of these until the bank statement is received. Each one of these entries must be entered and distributed to the proper income or expense account. Whatever the accounting system, its reconciling program usually provides a routine for entering these “end of month” bank credits and charges. 5.4 After agreeing all checks and deposits and entering all other bank credits and charges, the balance per accounting system and reconciled bank balance should agree. Any remaining difference must be investigated. If there is no other explanation, an adjustment should be made. This would be entered as a bank charge or credit and posted to a miscellaneous account.

- 5. SAMPLE POLICY FROM THE CEO- COMPANY POLICIES AND PROCEDURES SERIES INCLUDES AN EXAMPLE POLICY AND CONTENTS OF ALL NINE MANUALS. 5.5 Any outstanding checks or deposits in transit over six months old should be reviewed for disposition including write-off by a journal entry. Revision History: Revision Date Description of changes Requested By 0 mm/dd/yy Initial Release

- 6. SAMPLE POLICY FROM THE CEO- COMPANY POLICIES AND PROCEDURES SERIES INCLUDES AN EXAMPLE POLICY AND CONTENTS OF ALL NINE MANUALS.

- 7. SAMPLE POLICY FROM THE CEO- COMPANY POLICIES AND PROCEDURES SERIES INCLUDES AN EXAMPLE POLICY AND CONTENTS OF ALL NINE MANUALS.

- 8. SAMPLE POLICY FROM THE CEO- COMPANY POLICIES AND PROCEDURES SERIES INCLUDES AN EXAMPLE POLICY AND CONTENTS OF ALL NINE MANUALS. 36

- 9. SAMPLE POLICY FROM THE CEO- COMPANY POLICIES AND PROCEDURES SERIES INCLUDES AN EXAMPLE POLICY AND CONTENTS OF ALL NINE MANUALS.

- 10. SAMPLE POLICY FROM THE CEO- COMPANY POLICIES AND PROCEDURES SERIES INCLUDES AN EXAMPLE POLICY AND CONTENTS OF ALL NINE MANUALS.

- 11. SAMPLE POLICY FROM THE CEO- COMPANY POLICIES AND PROCEDURES SERIES INCLUDES AN EXAMPLE POLICY AND CONTENTS OF ALL NINE MANUALS.

- 12. SAMPLE POLICY FROM THE CEO- COMPANY POLICIES AND PROCEDURES SERIES INCLUDES AN EXAMPLE POLICY AND CONTENTS OF ALL NINE MANUALS.

- 13. SAMPLE POLICY FROM THE CEO- COMPANY POLICIES AND PROCEDURES SERIES INCLUDES AN EXAMPLE POLICY AND CONTENTS OF ALL NINE MANUALS.

- 14. SAMPLE POLICY FROM THE CEO- COMPANY POLICIES AND PROCEDURES SERIES INCLUDES AN EXAMPLE POLICY AND CONTENTS OF ALL NINE MANUALS.

- 15. SAMPLE POLICY FROM THE CEO- COMPANY POLICIES AND PROCEDURES SERIES INCLUDES AN EXAMPLE POLICY AND CONTENTS OF ALL NINE MANUALS.

- 16. SAMPLE POLICY FROM THE CEO- COMPANY POLICIES AND PROCEDURES SERIES INCLUDES AN EXAMPLE POLICY AND CONTENTS OF ALL NINE MANUALS.

- 17. SAMPLE POLICY FROM THE CEO- COMPANY POLICIES AND PROCEDURES SERIES INCLUDES AN EXAMPLE POLICY AND CONTENTS OF ALL NINE MANUALS.

- 18. SAMPLE POLICY FROM THE CEO- COMPANY POLICIES AND PROCEDURES SERIES INCLUDES AN EXAMPLE POLICY AND CONTENTS OF ALL NINE MANUALS.

- 19. SAMPLE POLICY FROM THE CEO- COMPANY POLICIES AND PROCEDURES SERIES INCLUDES AN EXAMPLE POLICY AND CONTENTS OF ALL NINE MANUALS.

- 20. SAMPLE POLICY FROM THE CEO- COMPANY POLICIES AND PROCEDURES SERIES INCLUDES AN EXAMPLE POLICY AND CONTENTS OF ALL NINE MANUALS.

- 21. SAMPLE POLICY FROM THE CEO- COMPANY POLICIES AND PROCEDURES SERIES INCLUDES AN EXAMPLE POLICY AND CONTENTS OF ALL NINE MANUALS.