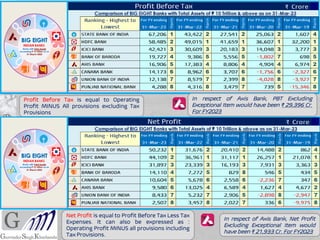

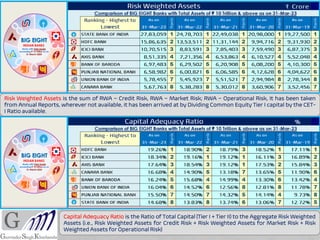

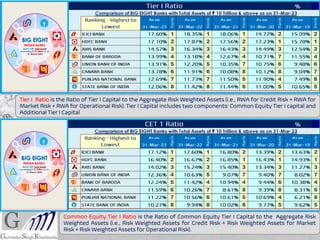

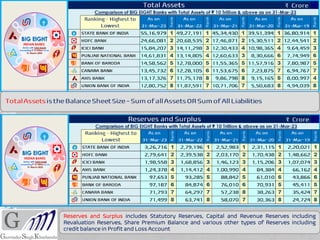

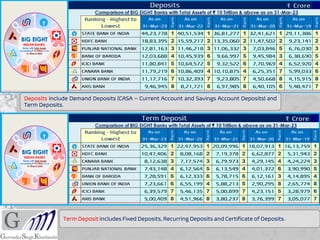

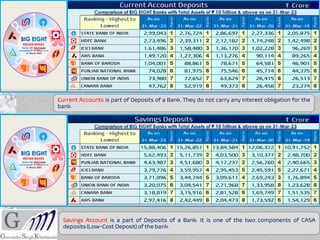

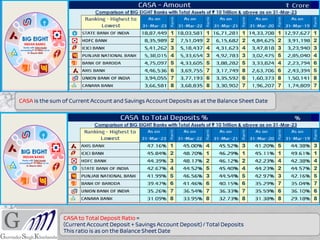

This document provides definitions and explanations of key financial terms and ratios used to analyze the financial performance and position of major Indian banks over a five year period. It defines various components of reserves and surpluses, deposits, loans, investments, income, expenses, asset quality, capital adequacy, profitability, and other metrics. Formulas are provided for calculating ratios like CASA, net interest margin, return on assets, return on equity and others.

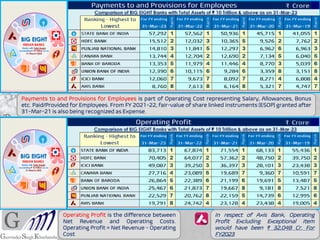

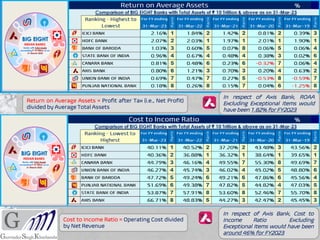

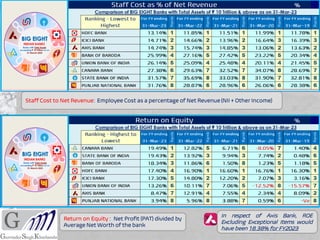

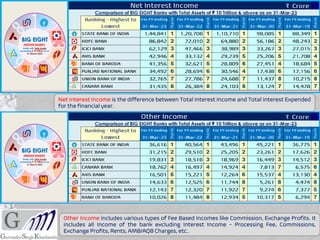

![Net Revenue is the Sum of Net Interest Income and Other Income. NET REVENUE = Net Interest

Income + Other Income

Operating Costs include all

expenses of the Bank for FY

excluding a) Interest Expended

and b) Provisions.

In respect of Axis Bank, Operating Cost

[FY2023] includes Exceptional Item

pertaining to acquisition of Citi Bank’s

Consumer Businesses](https://image.slidesharecdn.com/bigeightindianbanks1690609324-231222192221-6ea0b9ea/85/BIGEIGHT_INDIAN_BANKS-and-their-analysis-pdf-9-320.jpg)