Downloaded 18 times

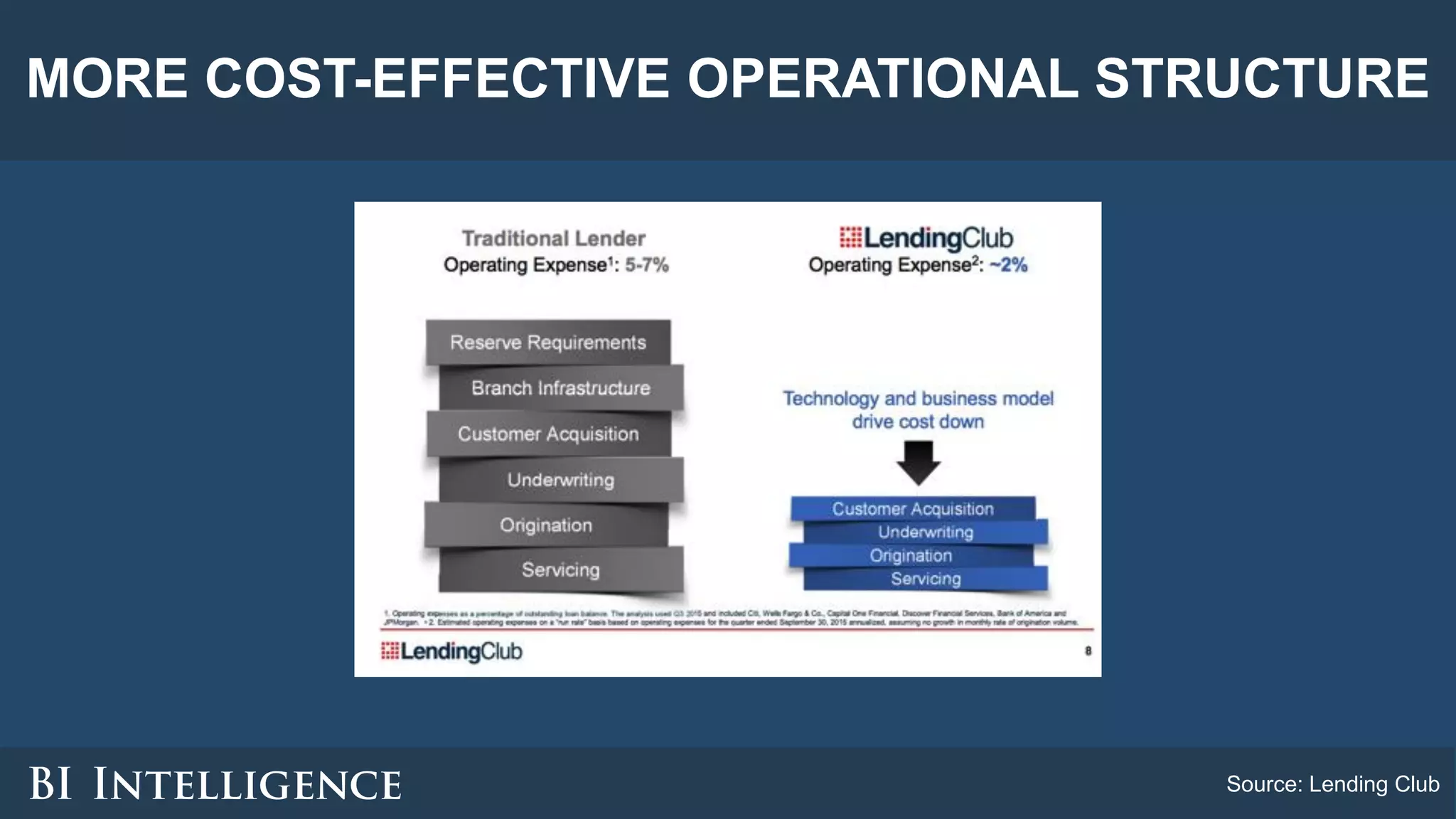

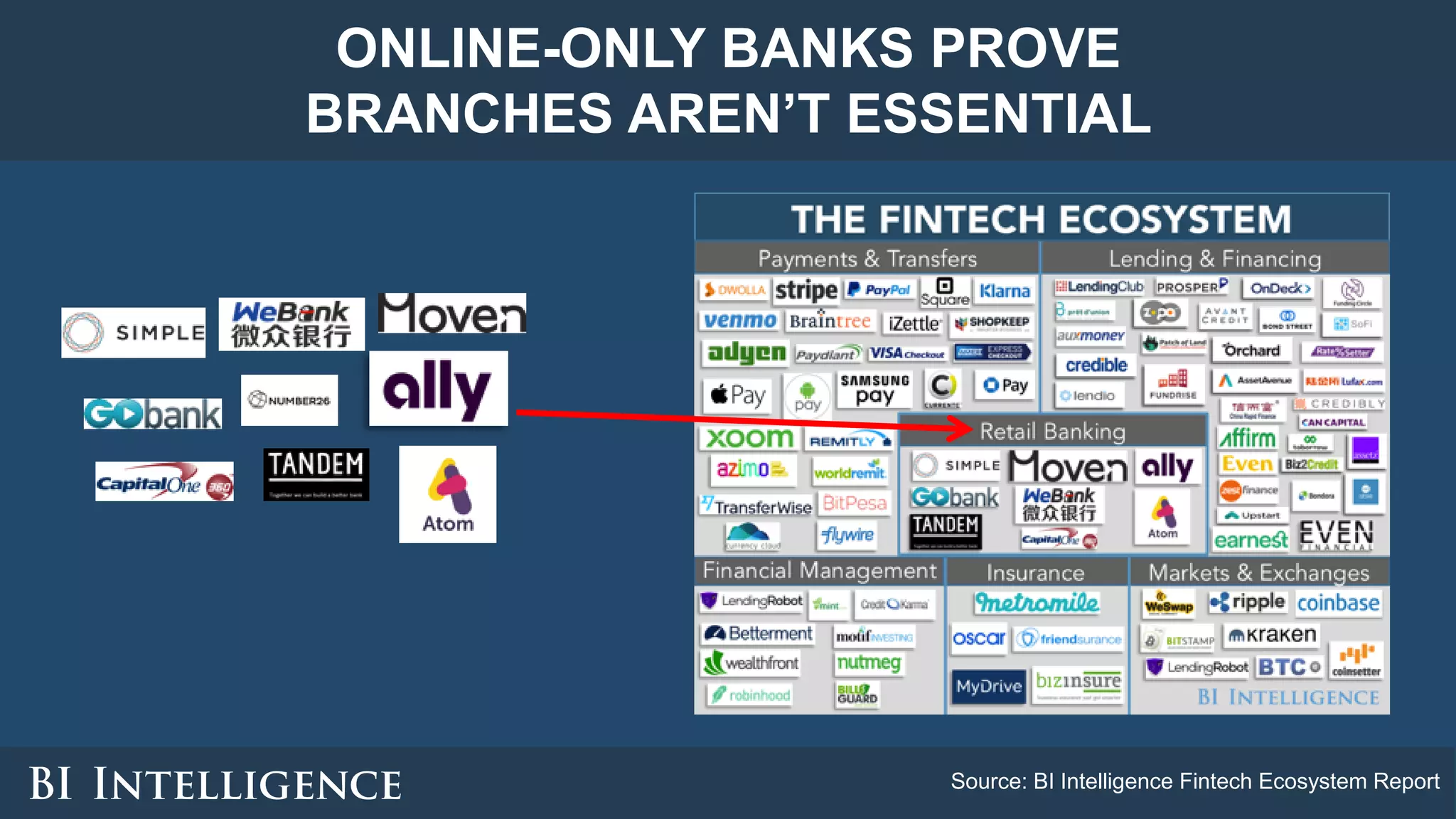

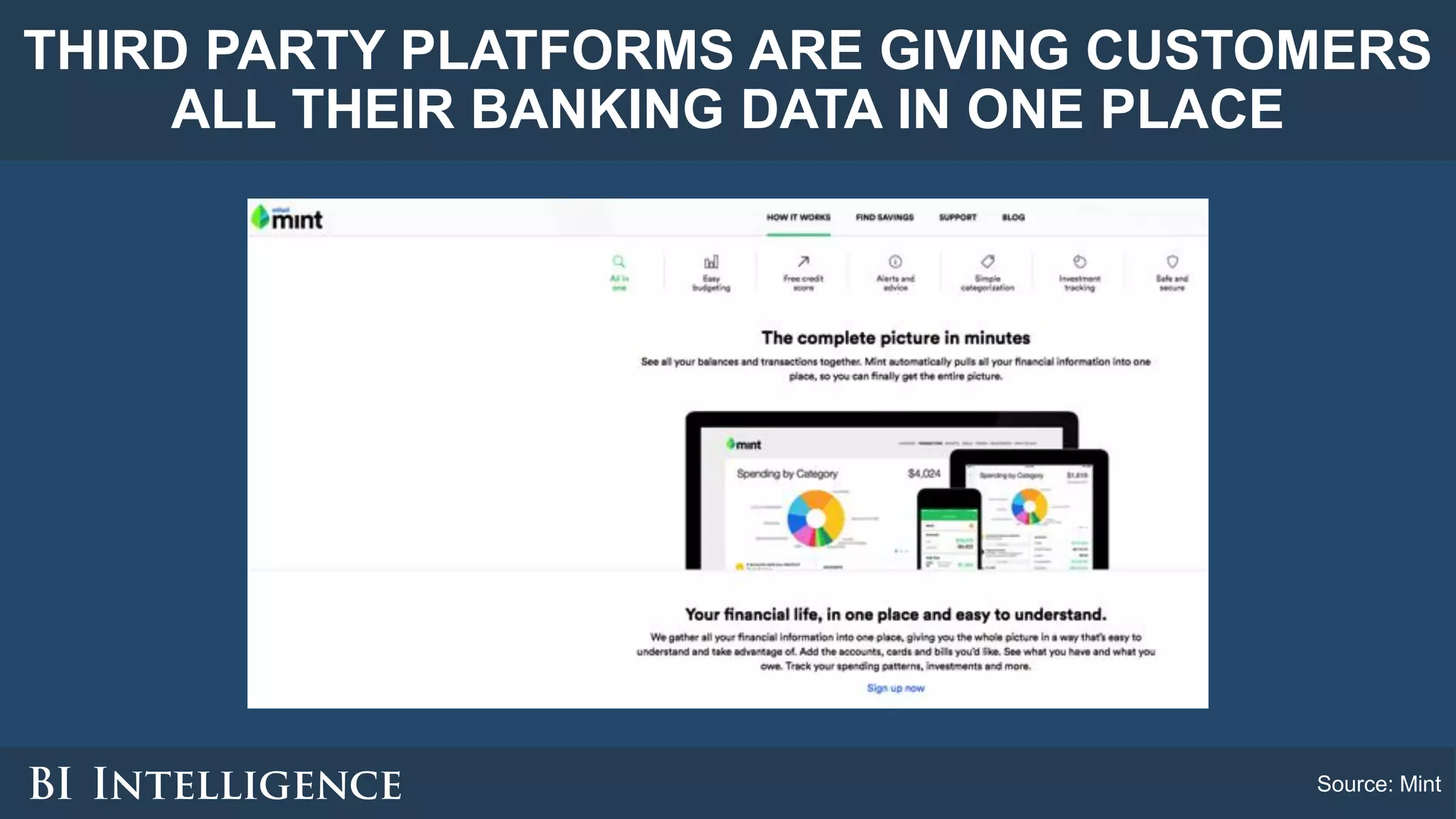

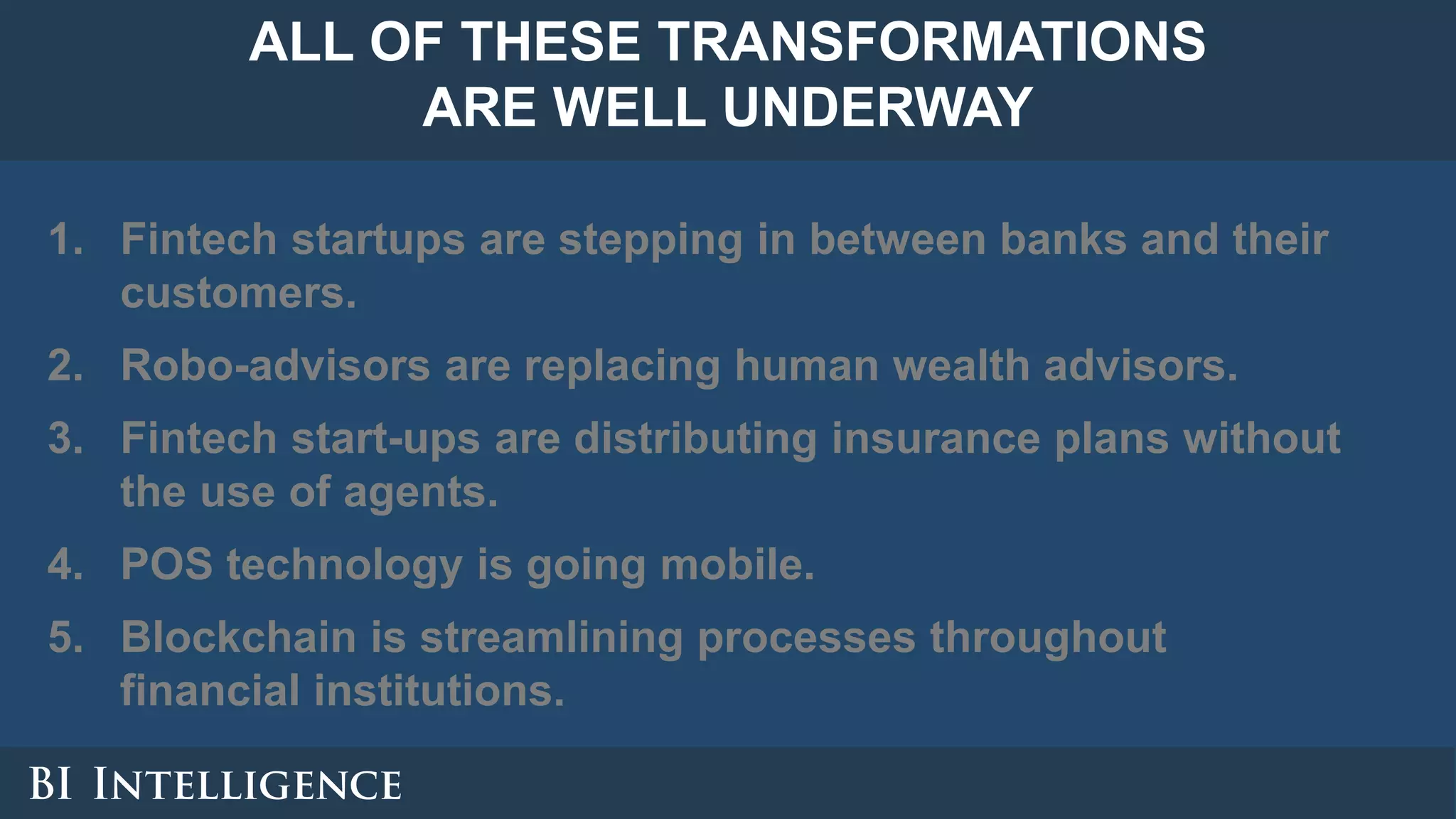

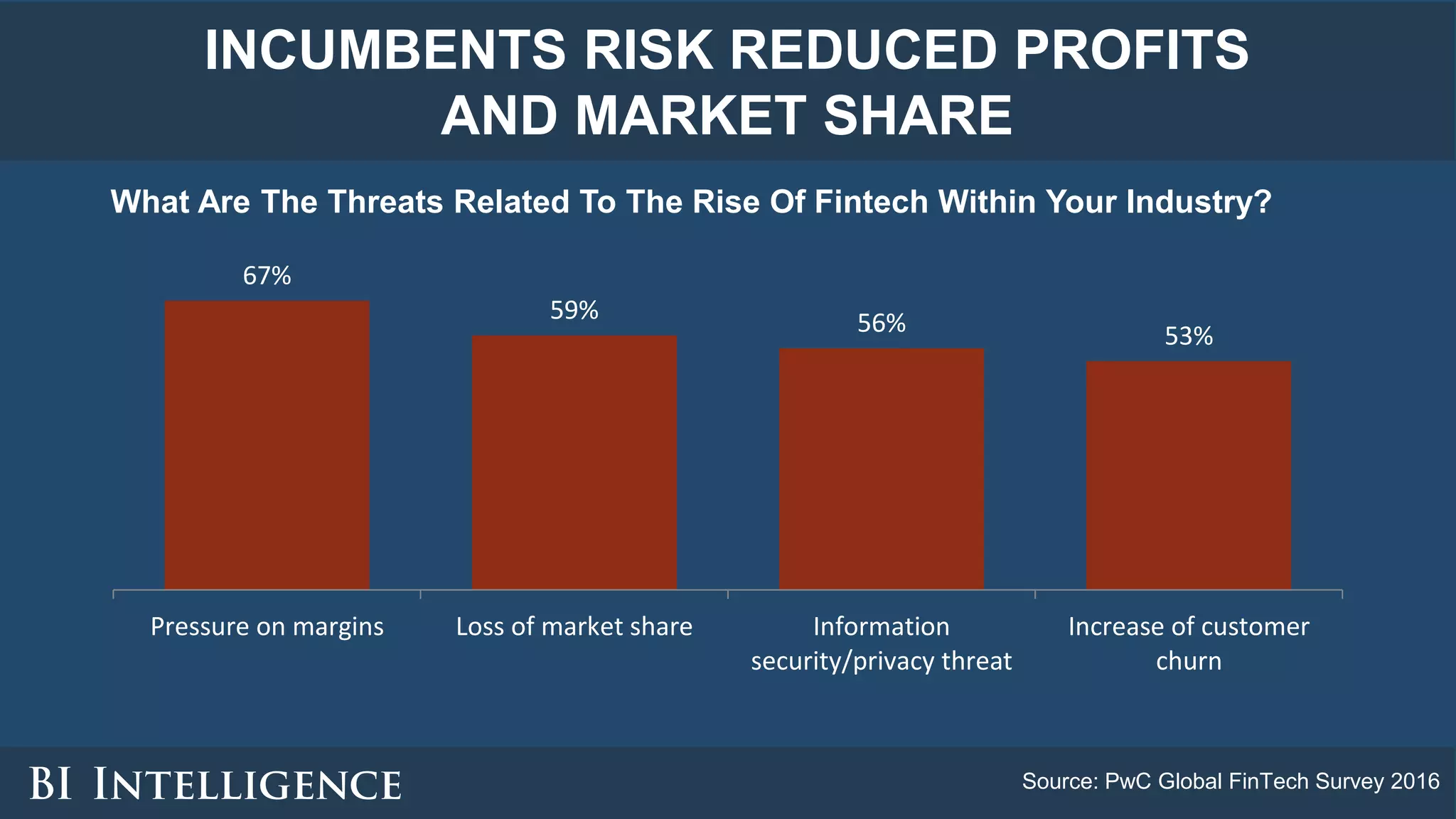

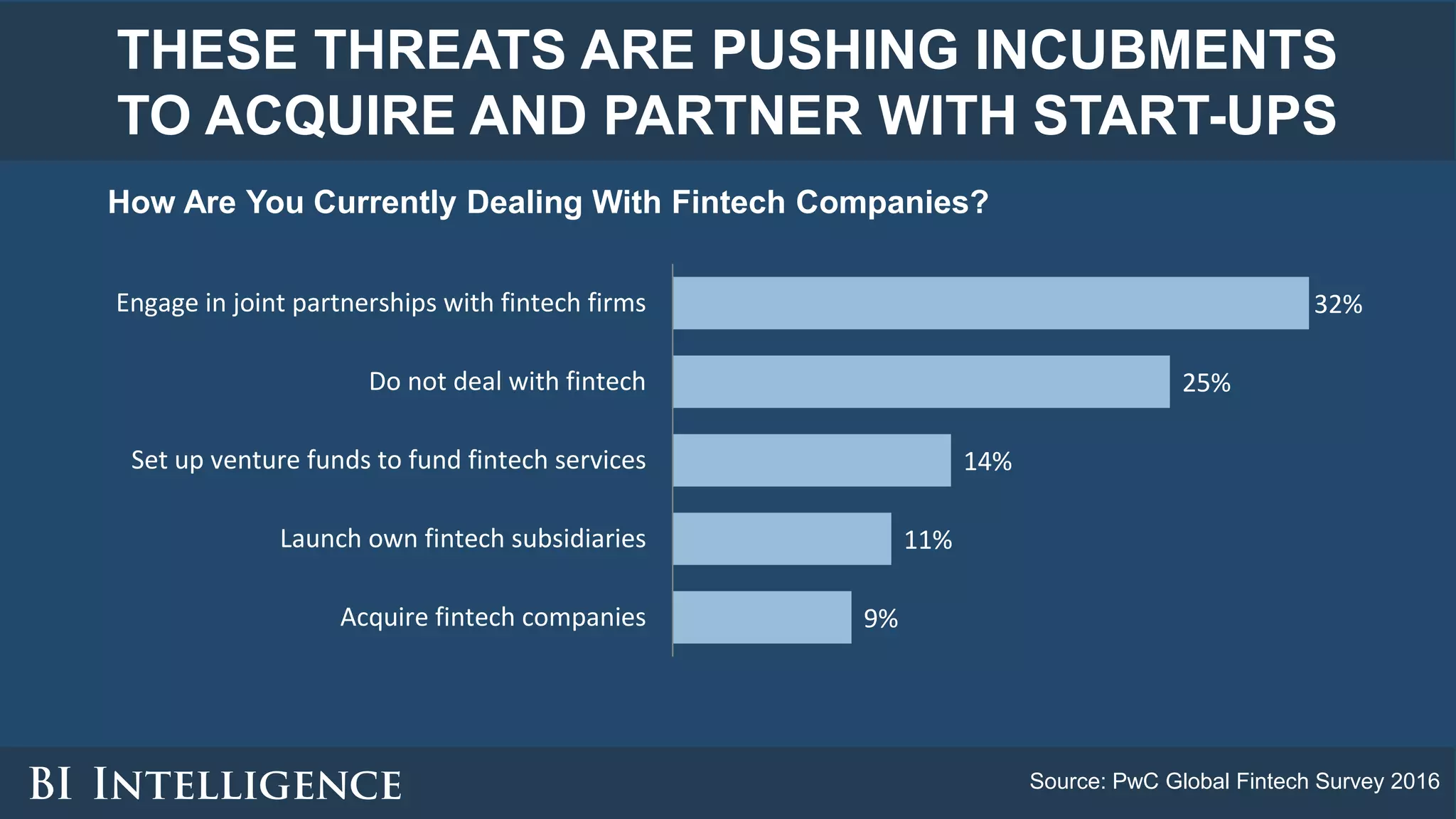

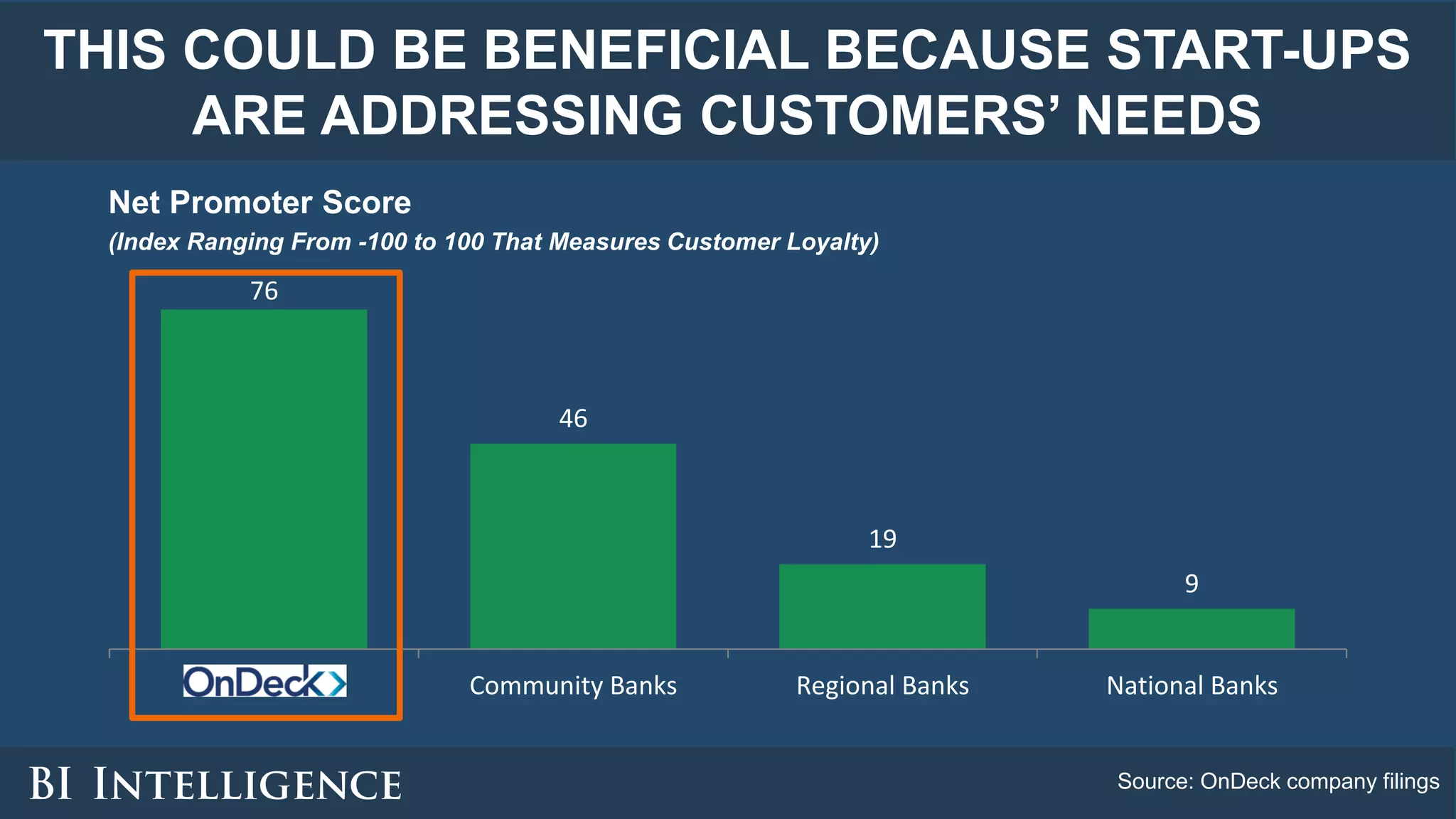

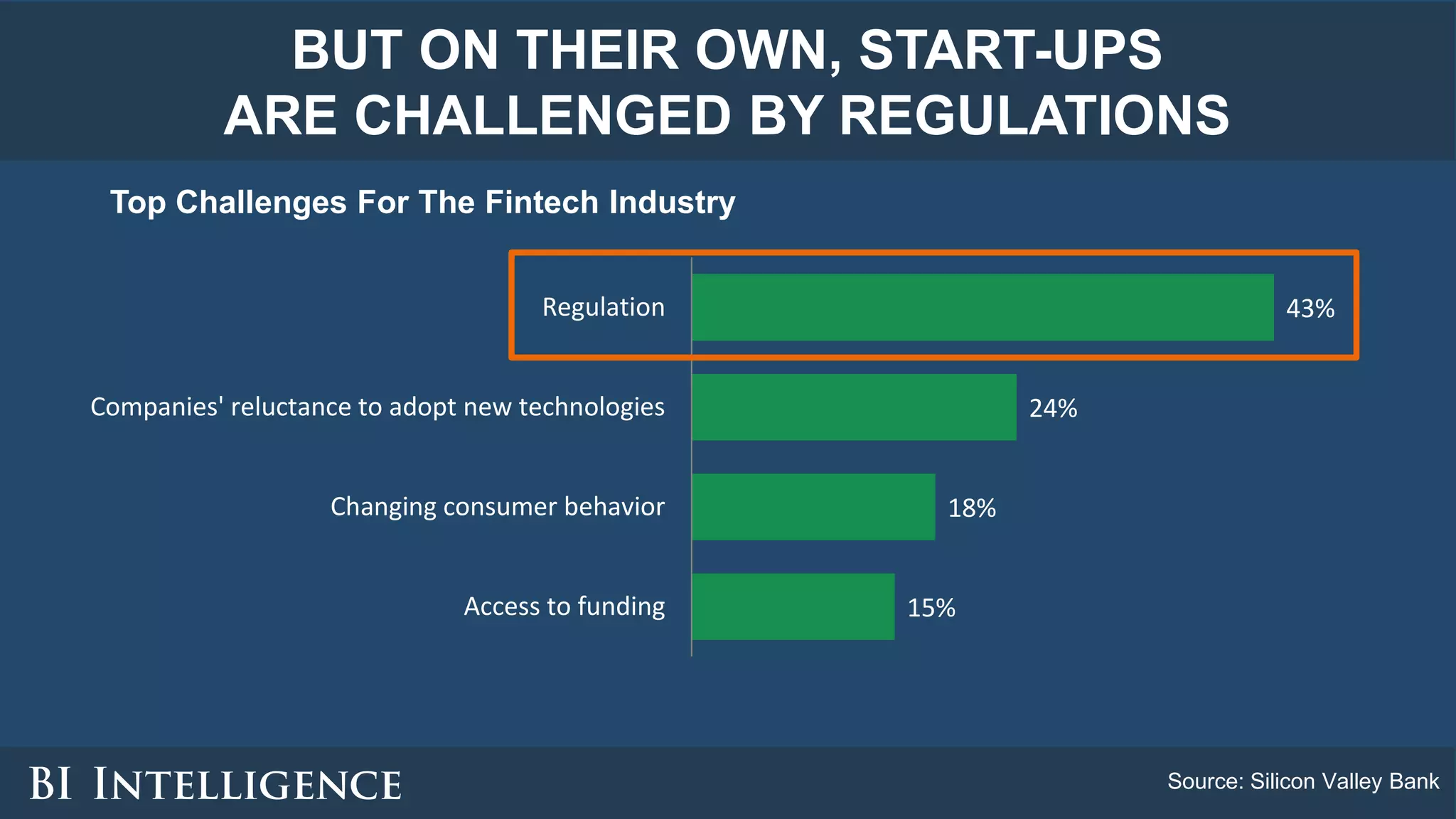

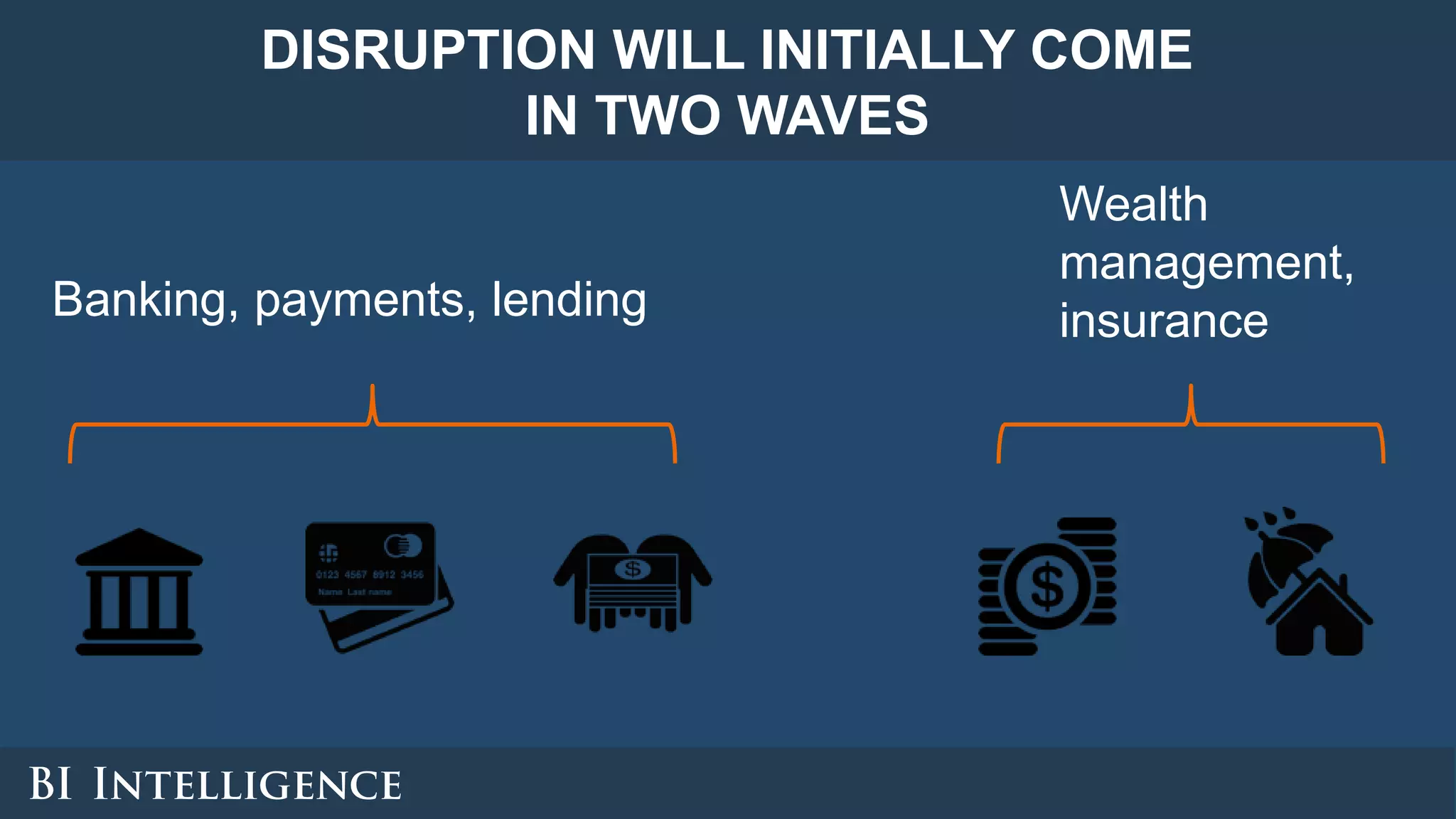

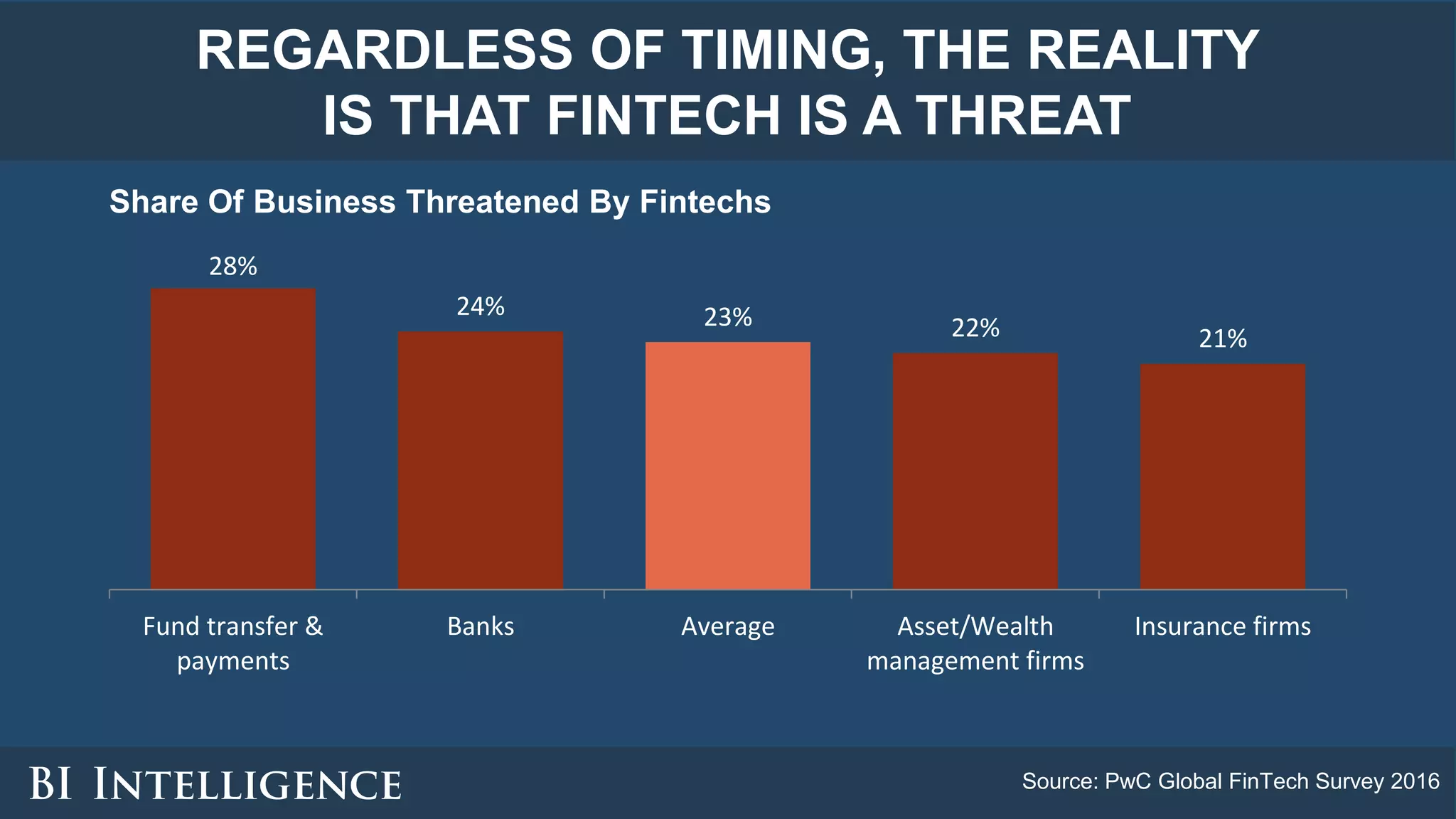

1. Fintech is leading five transformations in the financial services industry: (1) startups are stepping between banks and customers, (2) robo-advisors are replacing human advisors, (3) startups are distributing insurance without agents, (4) POS technology is going mobile, and (5) blockchain is streamlining processes. 2. These transformations threaten traditional financial institutions with reduced profits and market share, but also provide opportunities to partner with or acquire startups to address customer needs. 3. Regardless of timing, fintech poses a threat as it is disrupting areas like banking, payments, lending, and wealth management.