What is Bookkeeping

Bookkeeping is the process of systematic recording and classification of

financial transactions of an organisation.

Bookkeeping is said to be the basis of accounting, whereas accounting

forms a part of the broader scope in finance.

The most important focus of bookkeeping is to maintain an accurate record

of all the monetary transactions of a business. Companies use this

information to take major investment decisions.

The bookkeeper maintains bookkeeping records. Accurate bookkeeping is

critical for business as it gives a piece of reliable information on the

performance of a company.

3.

Bookkeeping process

Bookkeeping processconsists of the following

steps:

Identifying a financial transaction

Recording a financial transaction

Preparing a ledger account

Preparing trial balance

4.

What is Accounting?

Accounting is the systematic process of recording, measuring and

communicating information about the financial transaction taking

place in a business. Accounting helps in determining the financial

position of a firm and present the same to stakeholders.

It helps a business in the short and long term decision making and

also conveys the credibility of a company to the market.

It is also known as the language of business.

The purpose of accounting is to provide a clear view of financial

statements to its users, which includes investors, creditors,

employees, and government.

5.

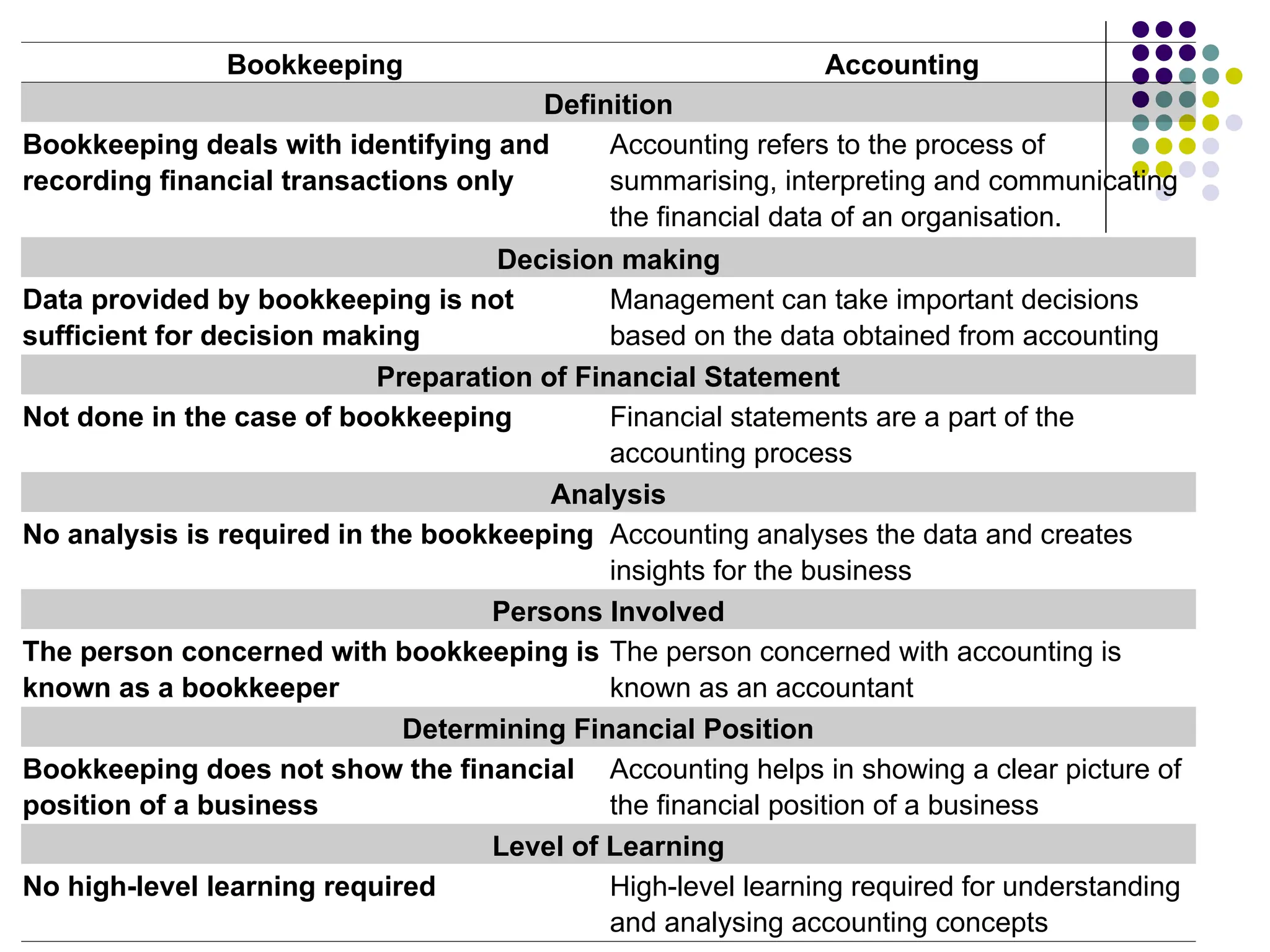

Bookkeeping Accounting

Definition

Bookkeeping dealswith identifying and

recording financial transactions only

Accounting refers to the process of

summarising, interpreting and communicating

the financial data of an organisation.

Decision making

Data provided by bookkeeping is not

sufficient for decision making

Management can take important decisions

based on the data obtained from accounting

Preparation of Financial Statement

Not done in the case of bookkeeping Financial statements are a part of the

accounting process

Analysis

No analysis is required in the bookkeeping Accounting analyses the data and creates

insights for the business

Persons Involved

The person concerned with bookkeeping is

known as a bookkeeper

The person concerned with accounting is

known as an accountant

Determining Financial Position

Bookkeeping does not show the financial

position of a business

Accounting helps in showing a clear picture of

the financial position of a business

Level of Learning

No high-level learning required High-level learning required for understanding

and analysing accounting concepts

Financial Accounting:

Financialaccounting is the branch of accounting concerned with the

supplying of financial information about a company to external stakeholders,

such as shareholders, financers/creditors and the government.

The financial accounting function of a company engages itself in preparing

the periodic financial statements which are then made available to the public

and stakeholders.

Financial accounting creates four main reports:

Balance sheets (what the company owns and owes).

Income statements (how much money came in and went out).

Cash flow statements (how cash moved through the business).

Statements of retained earnings (profits kept in the business).

8.

Management Accounting:

Managementaccounting focuses on analysing finances to prepare internal

financial reports and records that assist the managers of different

departments in the decision-making process to help drive business value.

Management accounting includes:

Planning budgets and comparing actual results.

Analyzing costs and benefits of business decisions.

Measuring how well different departments perform.

Forecasting future financial needs.

Management reports are kept within the company and help managers

improve budgeting and asses the performance of products or departments.

Management accounting is one accountancy outsourcing service that

Outbooks excels at.

9.

Cost Accounting:

Costaccounting, often considered a subset of management

accounting, specifically addresses the costs associated with

producing goods or services. This helps businesses understand

their cost structure and optimise pricing strategies.

It involves the recording, classifying and summarising of the cost

data via a completely quantitative approach. It includes the

management of the overall costs involved in running a business.

Cost data is used by the company management to plan and control

cost operations. Cost accounting aims to track the production cost

and the fixed costs of a company.

10.

Tax Accounting:

Taxaccounting ensures companies follow the tax regulations and stay

compliant with the government. It handles the tax-related matters of the

business and entails the calculation of the taxable income.

Tax accountants play a key role in managing tax filings and planning ahead

to reduce the company’s future tax burden. They are also responsible for

sharing accurate financial information with tax officials when required. Their

work helps businesses stay on the right side of the law.

Since tax rules change often and vary across countries, accountants must

stay constantly updated. They also advise on how taxes impact different

business activities and how to legally minimise them. In some cases, they

help resolve tax-related legal issues as well.

11.

Auditing:

Auditing involvesthe systematic and independent examination of a

company’s financial records, statements and internal control

systems. It ensures accuracy, reliability and compliance with

accounting standards, helping maintain public and stakeholder trust

in financial reporting.

Businesses invest heavily in audits because they offer assurance

that financial data is credible. The audit process includes examining,

verifying and evaluating financial accounts and internal controls to

identify any errors, fraud or misstatements that could mislead users

of financial information.

12.

Forensic Accounting:

Forensicaccounting is often said to be an amalgamation of accounting,

auditing, and investigation. It involves the analysing of information and

records of a company’s accounts for use in a court of law.

It also involves quantifying the damages in matters of embezzlements,

frauds, and falsification of accounts as well as in cases of personal

insurance, injury, business dispute, divorce and marital clashes,

environmental harms, and cybercrimes, among others.

Anything that involves court litigation, investigation and dispute resolution

comes within the ambit of forensic accounting. Forensic accountants may

be called in if anything suspicious surfaces during the external audit of a

company.

13.

Social Accounting:

Socialaccounting aims to incorporate the realisation of social and

environmental impact on the day-to-day accounting activities of

organizations. In the corporate setup, social accounting is closely related to

the Corporate Social Responsibility (CSR) concept.

Social accounting analyses and measures the impact of an organization on

society and the environment. It also measures the social costs and benefits

of organisation’s activities.

Just like any other branch of accounting, social accounting is also a method

of quantifying the performance of a company, but in terms of social

accountability.

14.

Users of Accounting

Information

Investors: They provide capital to the firm. Hence,

they need information to assess the inherent risk

of loss of capital and the return their investment

in the firm is likely to yield. They also need

information to buy, sell or hold these investments.

Lenders: They are interested in ascertaining the

ability of the firm to service their loans over the

entire term of the loan by paying interest and

repaying installments on the due dates.

15.

Suppliers andother creditors: They would

like to assess the ability of the firm to pay

amounts owed to them within the credit

period allowed to the firm. Normally, the

interest of the trade creditors is over shorter

periods as compared to lenders.

Customers and employees: They would like

to know if the firm represents a stable source

of supply/employment.

16.

Government: Thegovernment is interested in

information that will help it to assess the

taxes that can be collected from the firm,

regulate the businesses in general, draft tax

and economic policies, and prepare national

income statistics.

Public: Members of the public are interested

in assessing the economic benefits and costs

arising from factors such as employment of

people from the locality, patronage to local

suppliers and hazards to environment

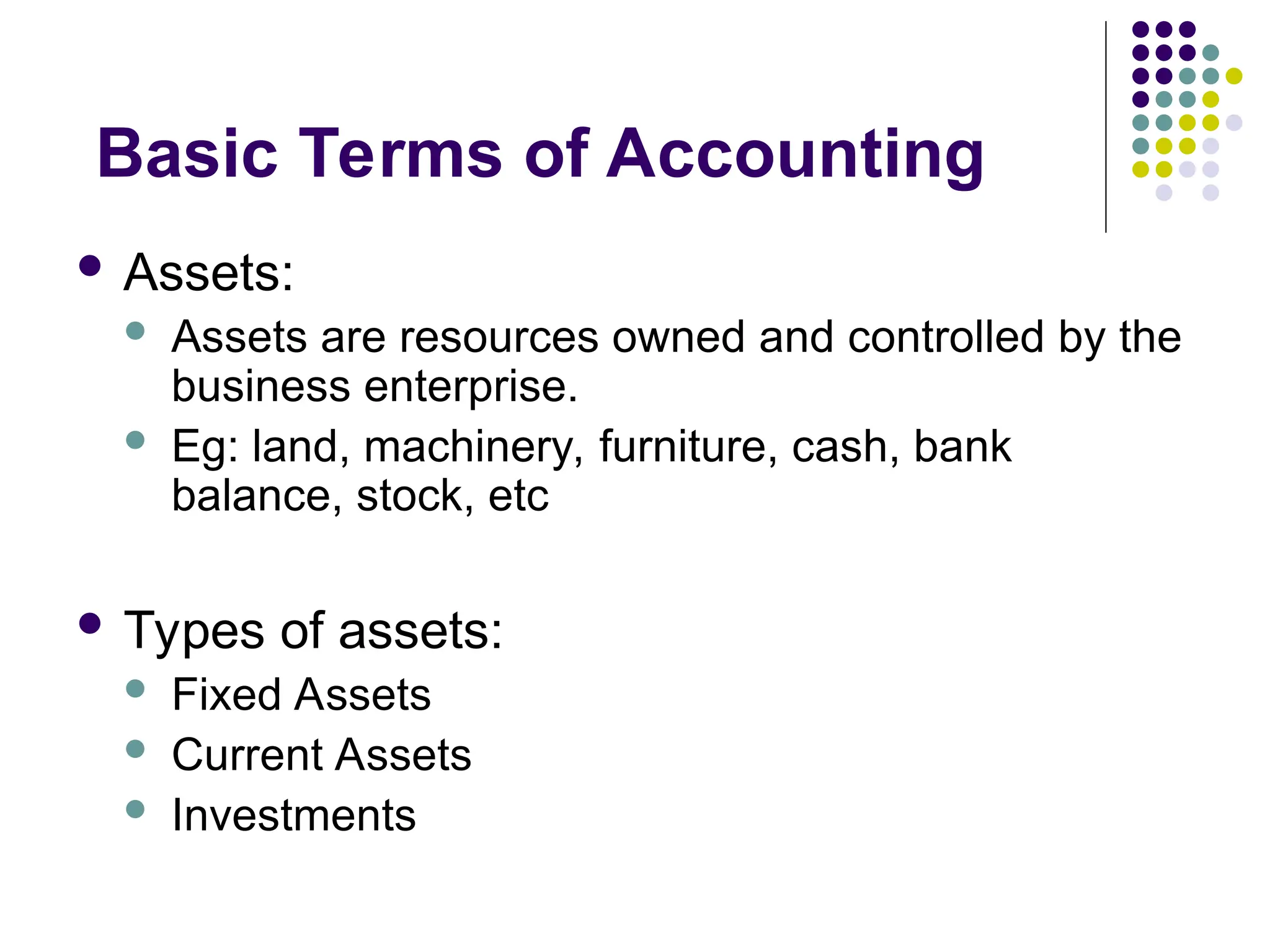

Basic Terms ofAccounting

Assets:

Assets are resources owned and controlled by the

business enterprise.

Eg: land, machinery, furniture, cash, bank

balance, stock, etc

Types of assets:

Fixed Assets

Current Assets

Investments

19.

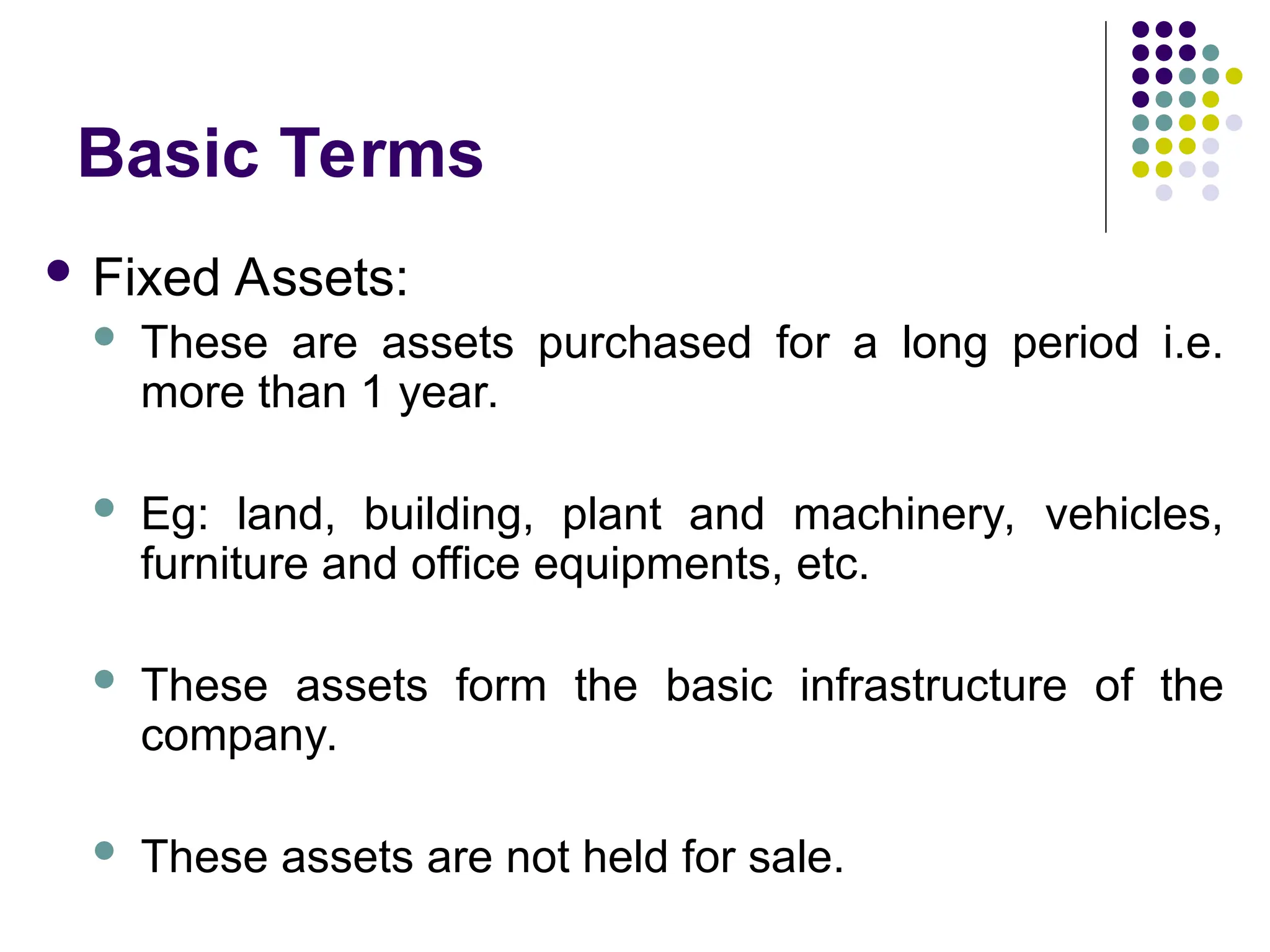

Basic Terms

FixedAssets:

These are assets purchased for a long period i.e.

more than 1 year.

Eg: land, building, plant and machinery, vehicles,

furniture and office equipments, etc.

These assets form the basic infrastructure of the

company.

These assets are not held for sale.

20.

Basic Terms

CurrentAssets

These assets are required to carry on the day to

day business activities.

Eg:

Inventories [raw material, work in progress & finished

goods]

Cash balance

Bank balance

Debtors

Receivables

21.

Basic Terms

Investments:

When a business enterprise puts its surplus funds

in shares or bonds of governments, it is known as

investments.

Investments generate income in form of interest,

dividends, etc.

They generate gains or loss when sold.

22.

Basic Terms

Liabilities:

Liabilities are obligations of the business enterprise,

payable to outsiders & to owners of the business.

Eg:

Owner’s capital

Borrowings

Creditors

Payables

23.

Basic Terms

Typesof liabilities;

Long term liabilities:

Any liability payable after a period exceeding 1

year.

Eg: owner’s capital, bank loans for more than a

year

24.

Basic Terms

CurrentLiabilities

Any liability payable within a year or liabilities

incurred in day to day course of business.

Eg: creditors, payables, bank O.D or short term

credit, etc.

25.

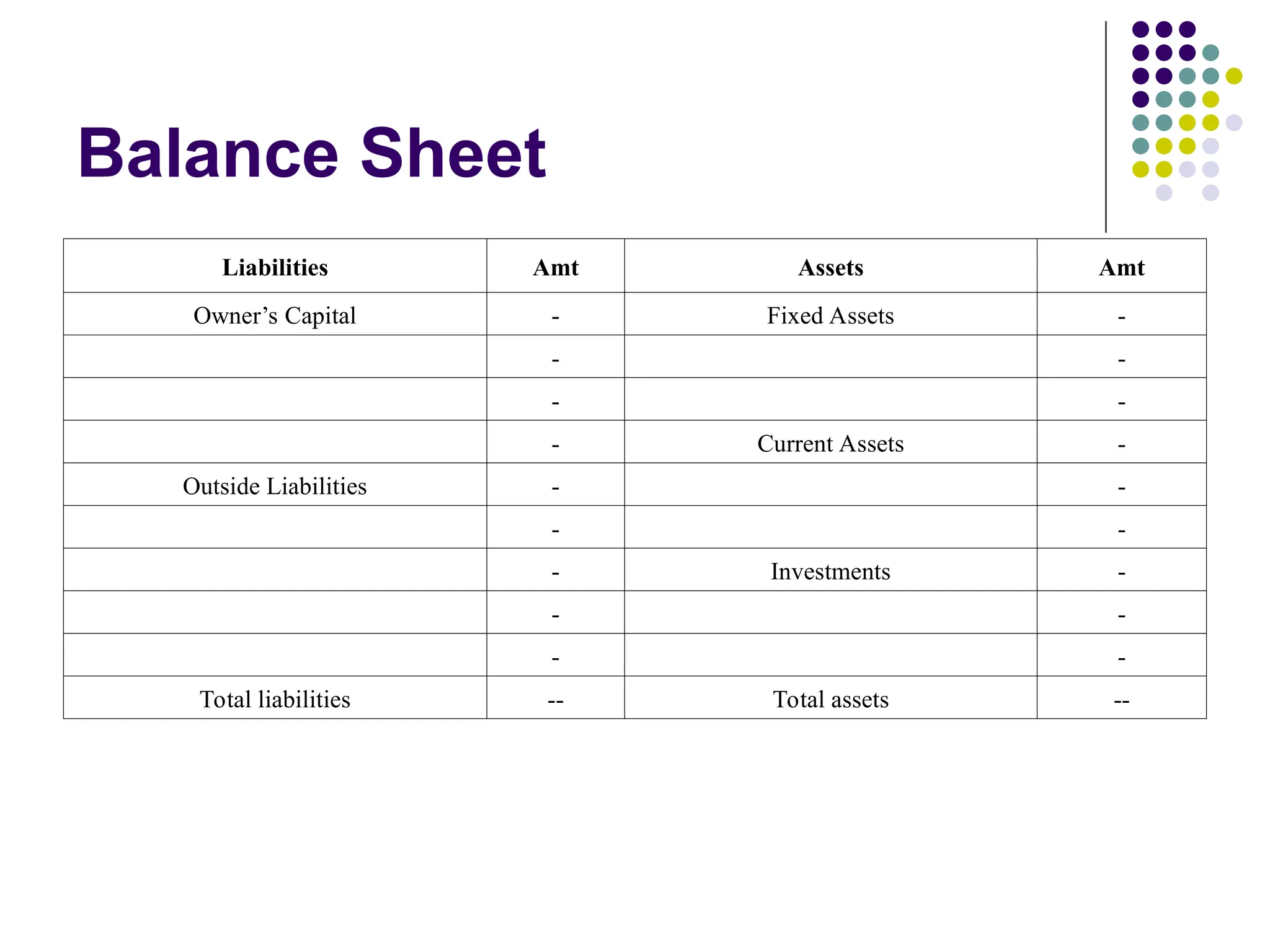

Balance Sheet

Liabilities AmtAssets Amt

Owner’s Capital - Fixed Assets -

- -

- -

- Current Assets -

Outside Liabilities - -

- -

- Investments -

- -

- -

Total liabilities -- Total assets --

26.

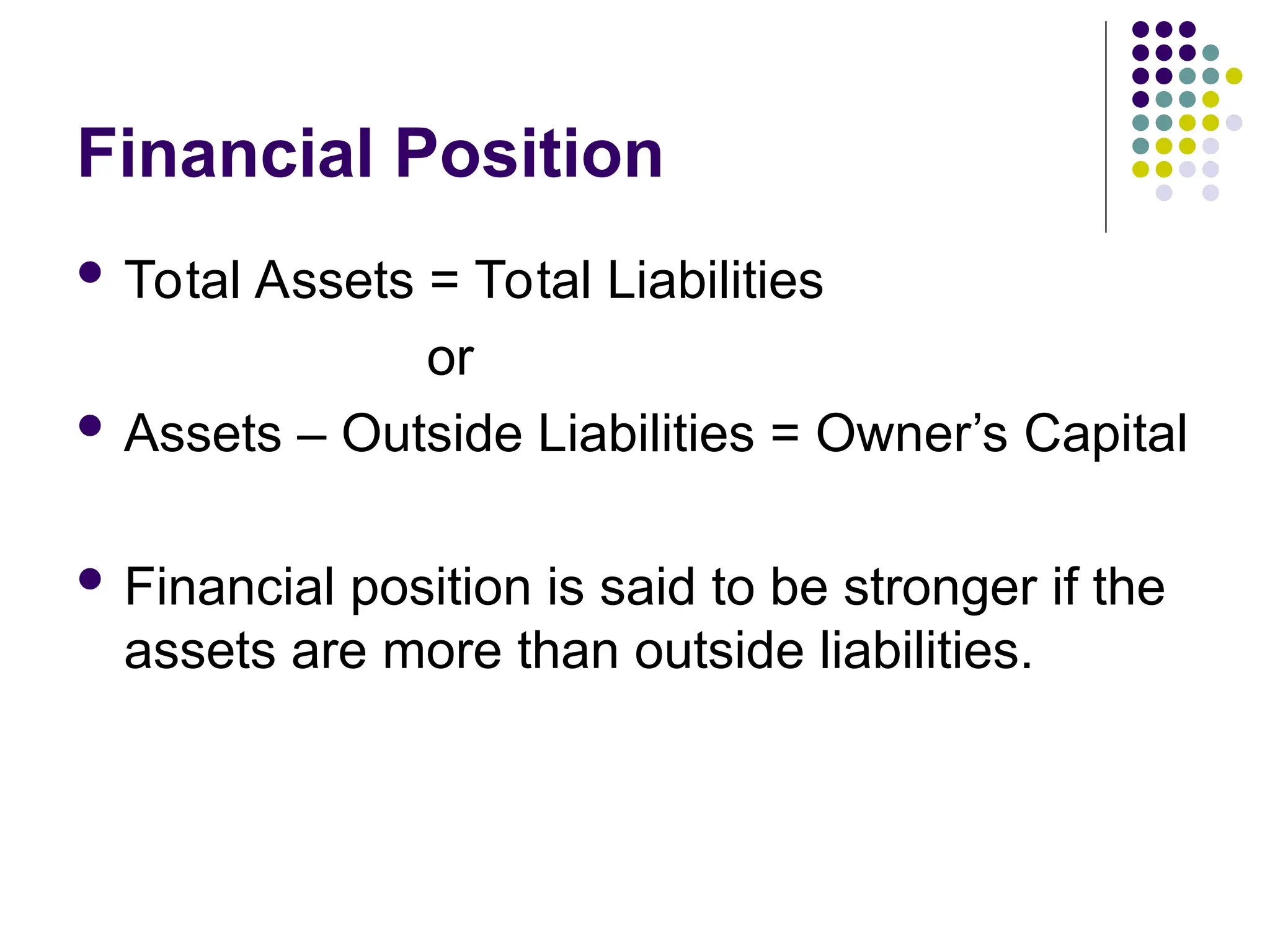

Financial Position

TotalAssets = Total Liabilities

or

Assets – Outside Liabilities = Owner’s Capital

Financial position is said to be stronger if the

assets are more than outside liabilities.

27.

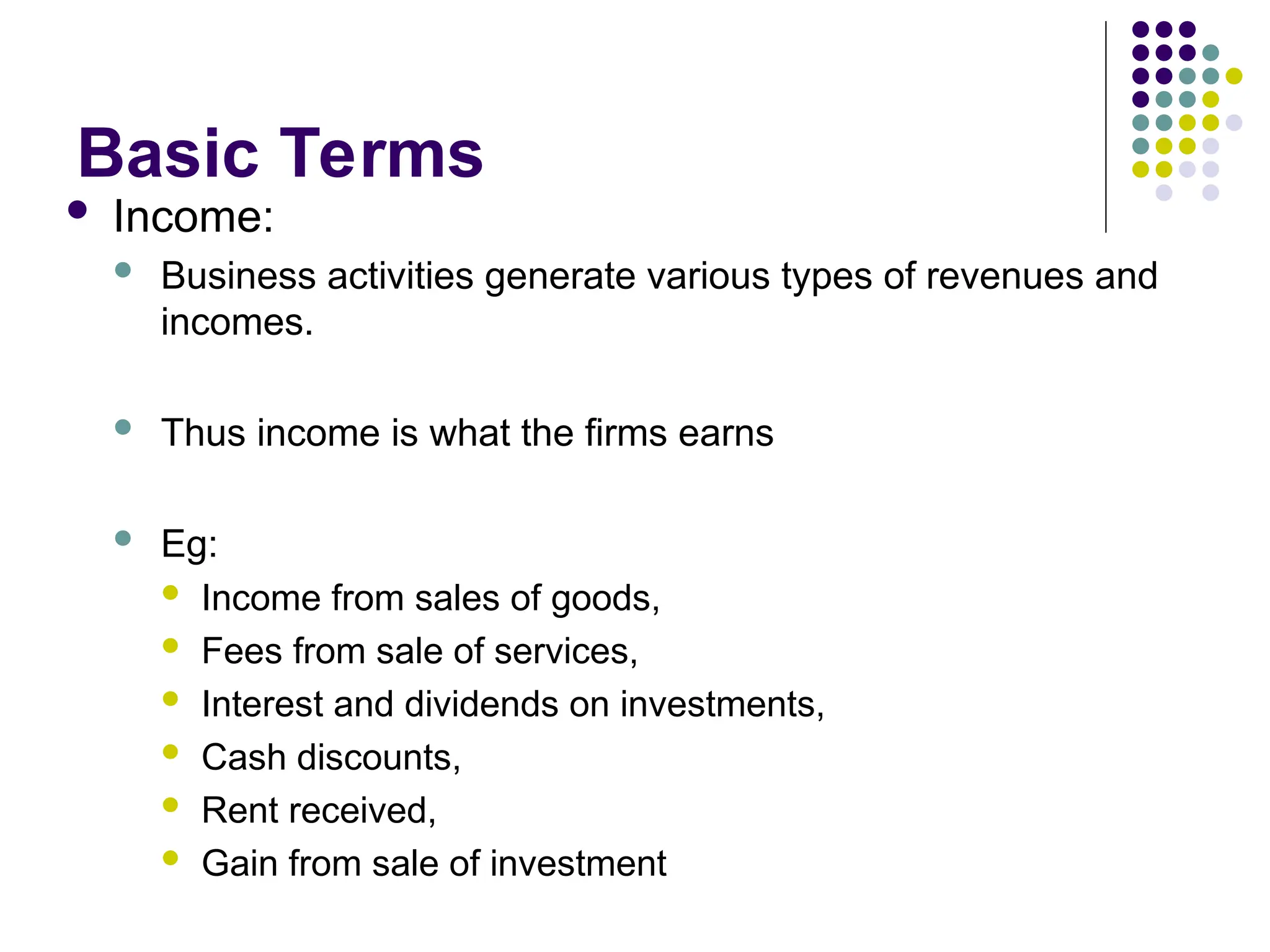

Basic Terms

Income:

Business activities generate various types of revenues and

incomes.

Thus income is what the firms earns

Eg:

Income from sales of goods,

Fees from sale of services,

Interest and dividends on investments,

Cash discounts,

Rent received,

Gain from sale of investment

28.

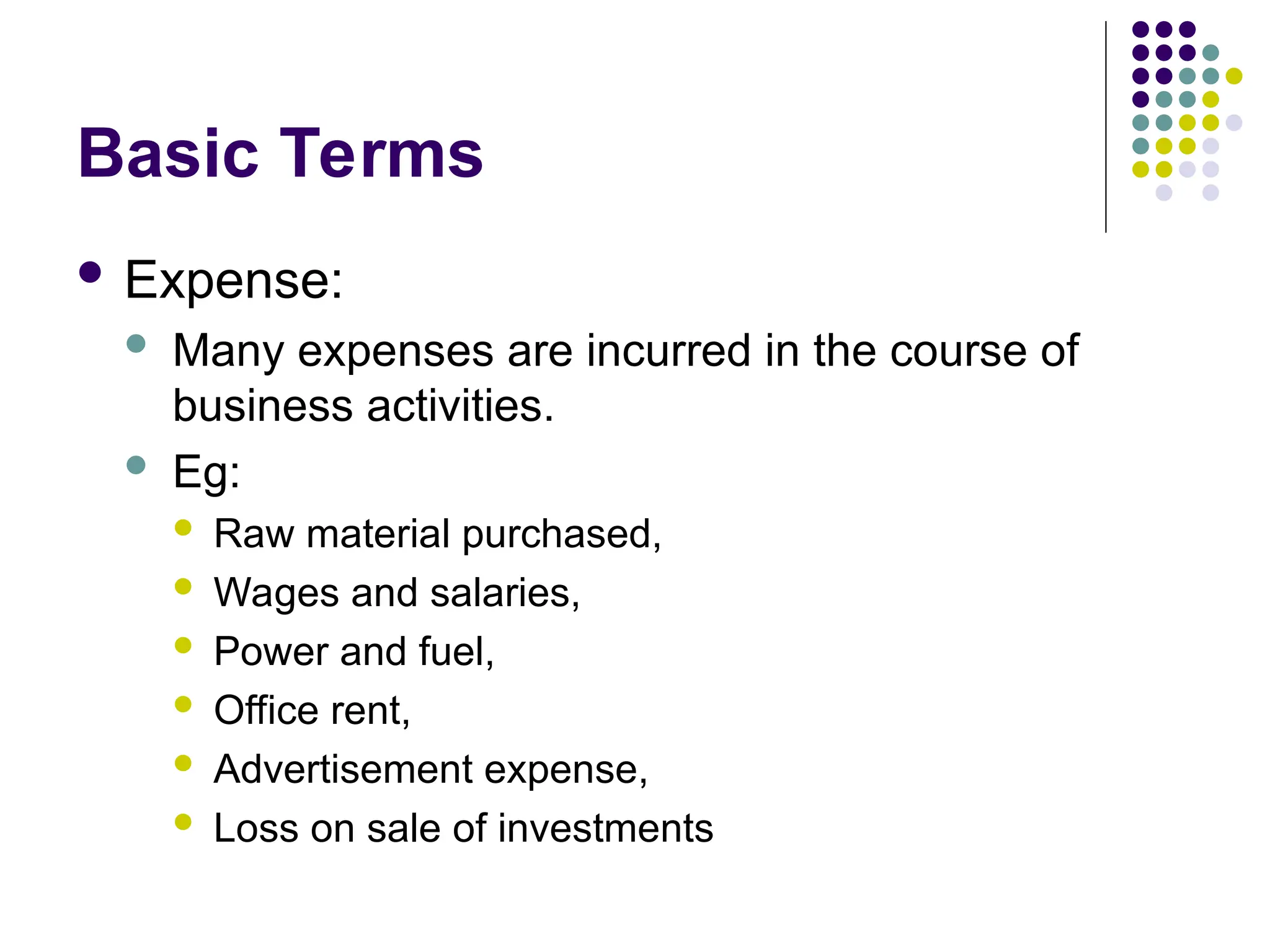

Basic Terms

Expense:

Many expenses are incurred in the course of

business activities.

Eg:

Raw material purchased,

Wages and salaries,

Power and fuel,

Office rent,

Advertisement expense,

Loss on sale of investments

29.

Financial Performance

Excessof income over expenses is known as

net profit.

Excess of expenses over income is known as

net loss.

Every business strives to earn profits.

30.

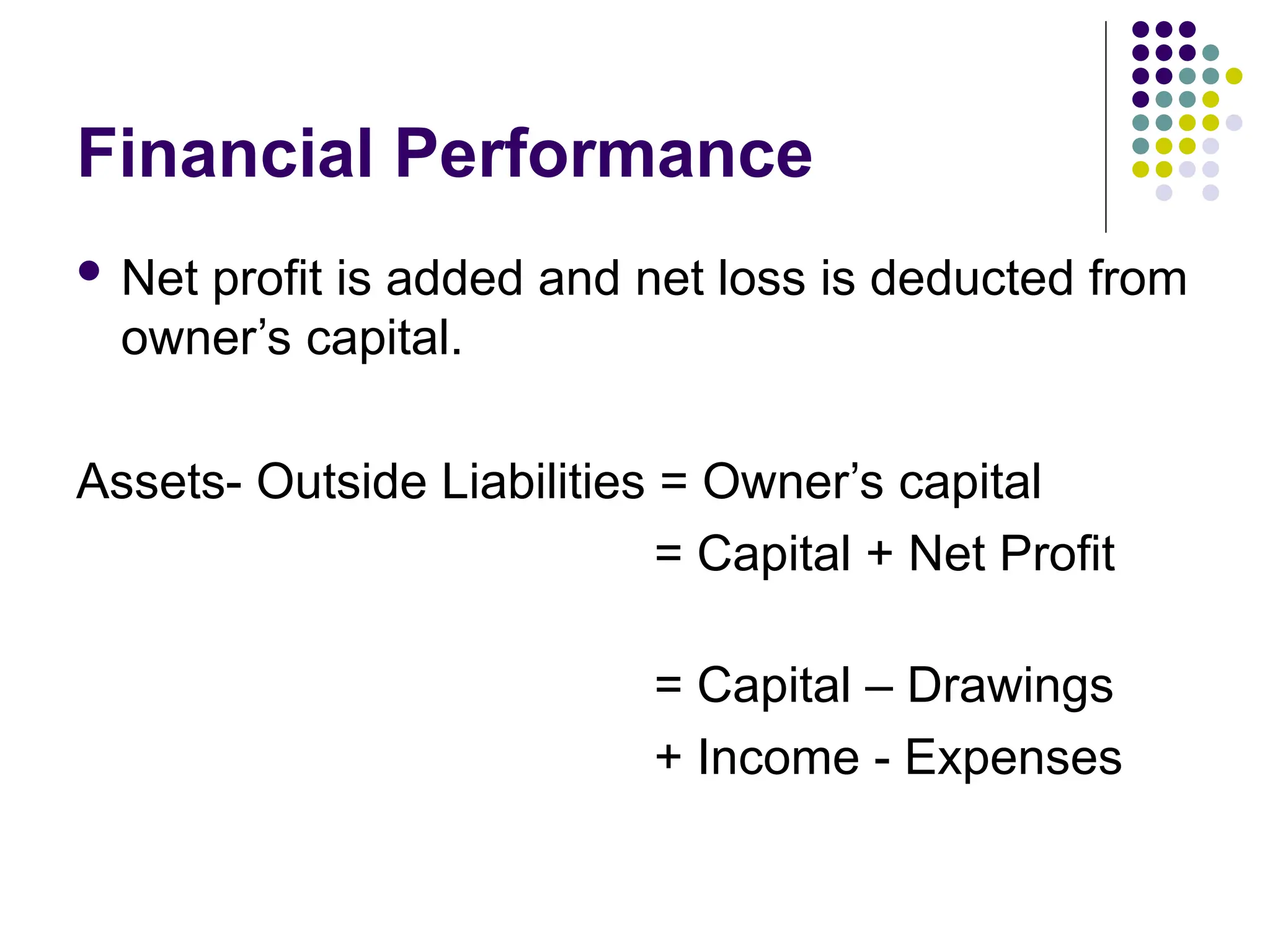

Financial Performance

Netprofit is added and net loss is deducted from

owner’s capital.

Assets- Outside Liabilities = Owner’s capital

= Capital + Net Profit

= Capital – Drawings

+ Income - Expenses

31.

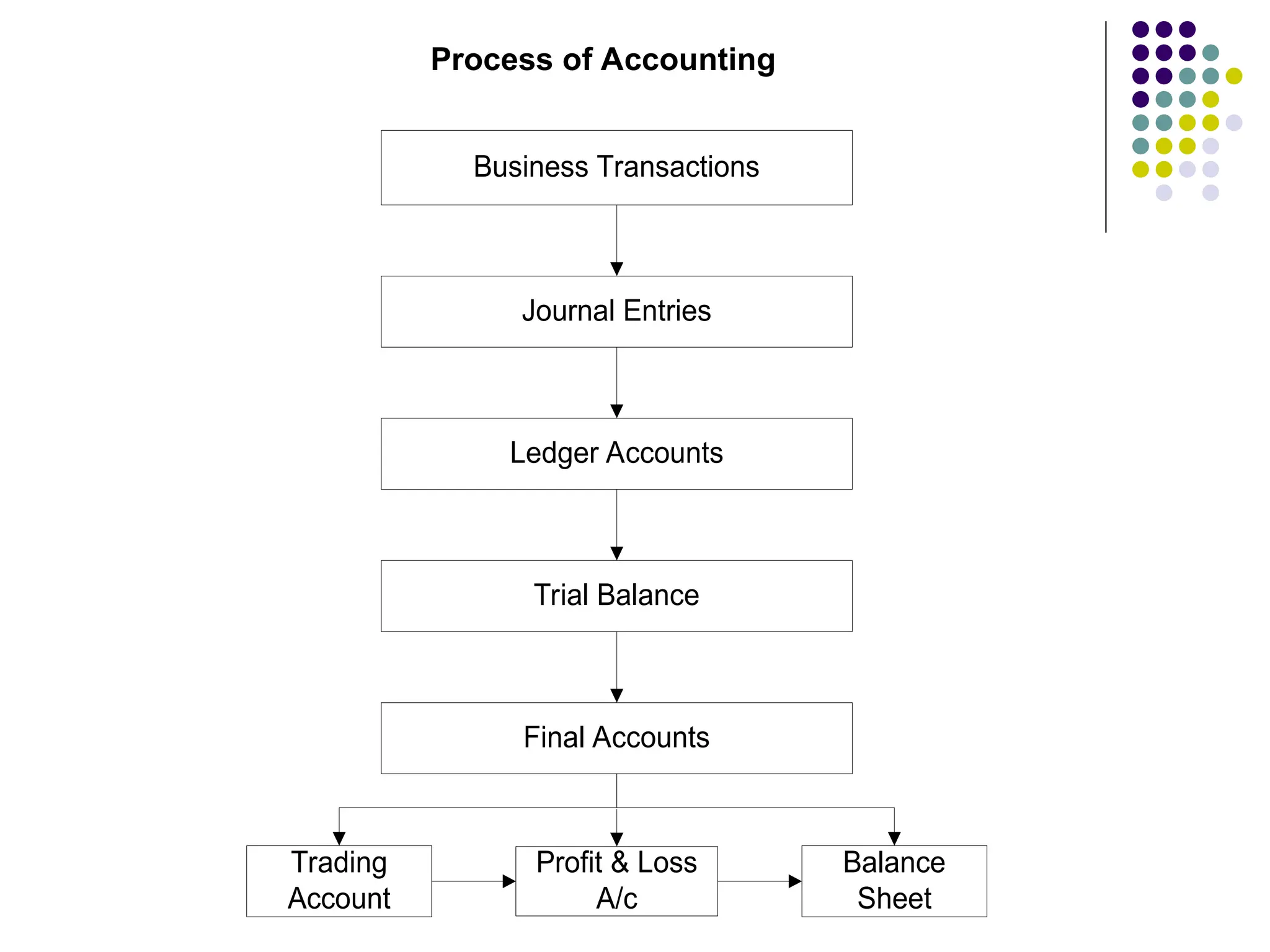

Accounting Process orCycle

1.) Analysis of business transactions

2.) Documentation

3.) Recording

4.) Classifying

5.) Summarizing

6.) Bifurcating

32.

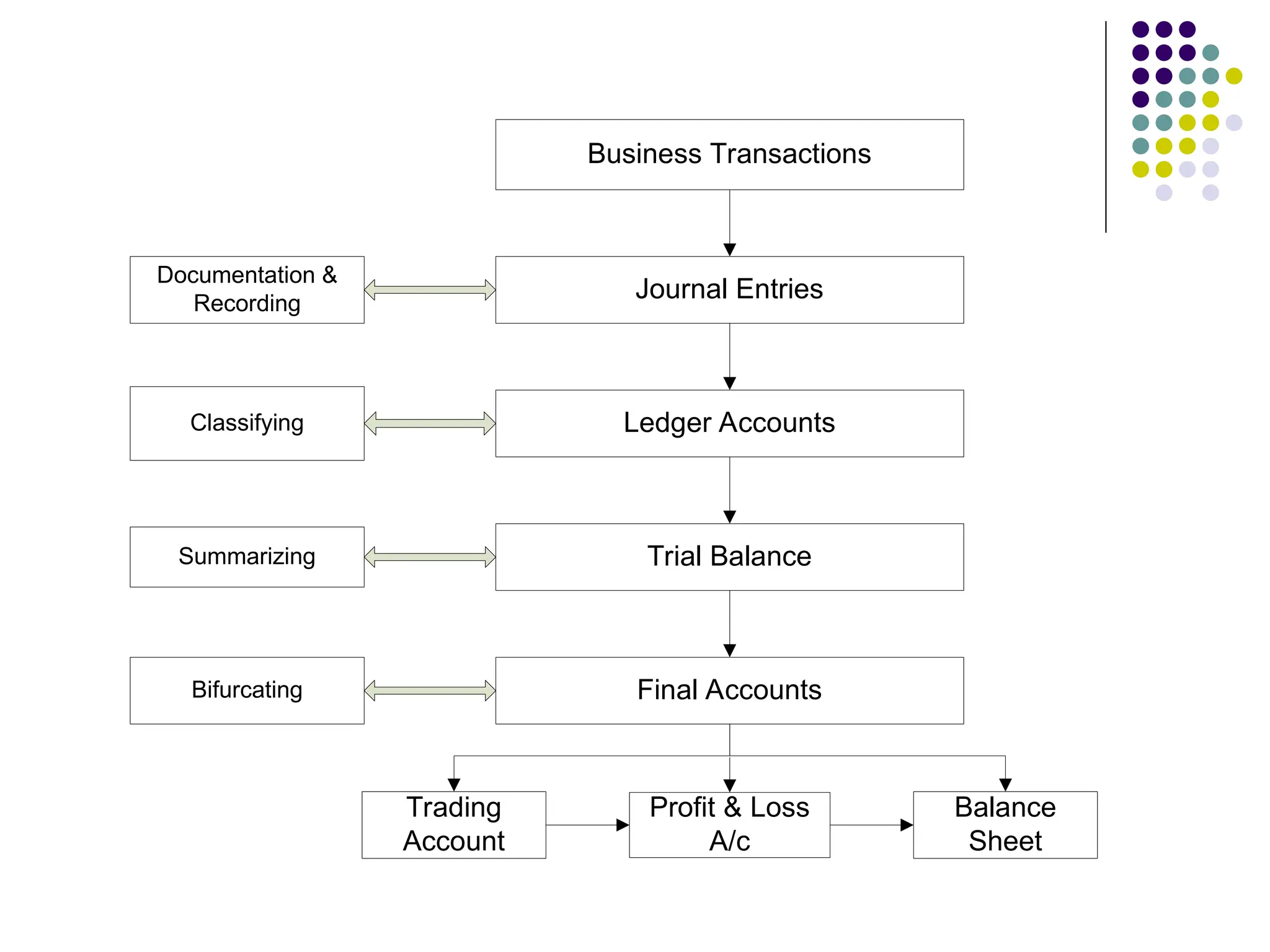

Business Transactions

Journal Entries

LedgerAccounts

Trial Balance

Final Accounts

Trading

Account

Profit & Loss

A/c

Balance

Sheet

Documentation &

Recording

Classifying

Summarizing

Bifurcating

33.

What is anAccount?

An account is a device to record business

transactions.

There are various accounts prepared for

each asset, liability, income and expenses.

An account has two sides:

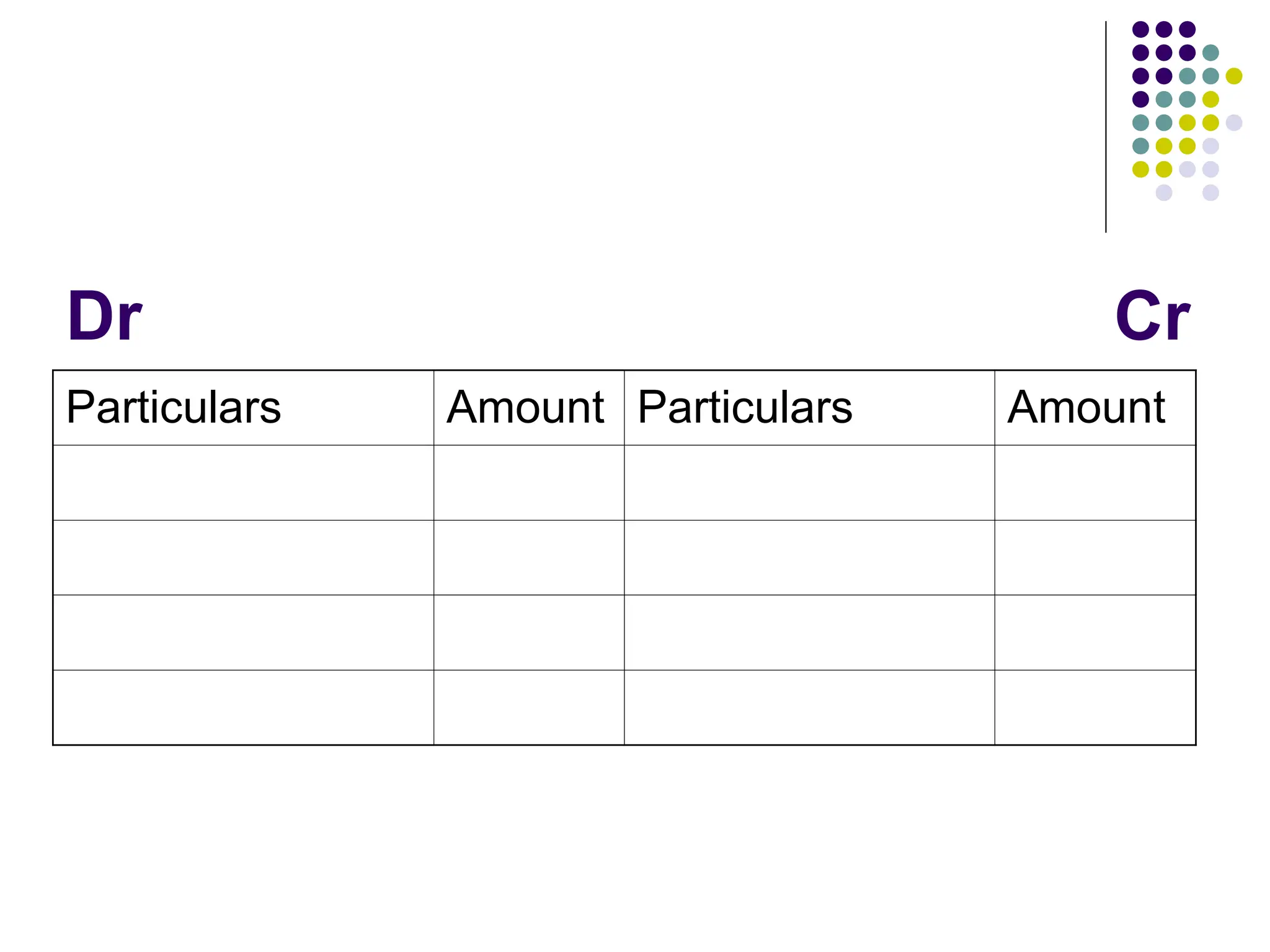

What is anAccount?

The left side of an account is known as debit

(Dr).

The right side of an account is known as

credit (Cr).

In any account, on one side increase is

recorded and on other side the decrease in

the item is recorded.

36.

Types of Accounts

Nominal / temporary accounts

The accounts related to all incomes and expenses.

Eg: Interest A/c, Rent A/c, Salary A/c, Etc.

Personal accounts

Accounts of natural persons like Mr. Ramesh, Mr. Suresh, etc.

Accounts of legal persons like companies, banks, government,

etc.

These persons are generally the buyers, sellers, lenders,

investors, etc. associated with the company.

In short they are debtors or creditors.

37.

Types of Accounts

Real / Permanent accounts

These are accounts of various assets and goods.

Eg: Buildings A/c, Machinery A/c, debtors’ A/c,

purchase A/c, Sales A/c.

38.

What is Debitand Credit?

Debit is the left hand side of an A/c.

Thus amounts written on the left side of an

account are called debits.

Credit is the right side of an A/c.

Thus amounts written on the right side of an

account are called credits.

39.

Debit Balance &Credit Balance

Every A/c has a debit balance or a credit balance.

Debit Balance:

An account has a debit balance when the total of debit side

is more than the total of credit side.

All assets and expenses have a debit balance.

For assets and expenses, an increase is written on debit

side and a decrease on credit side.

40.

Debit Balance &Credit Balance

Credit Balance

When the total of credit side is more than the total

of debit side, it is known as a credit balance.

All liabilities and incomes have a credit balance.

For liabilities and incomes, an increase is written

on credit side and decrease is written on debit

side.

41.

Rules of Debitand Credit

The system of accounting is a double entry

system.

Under double entry system of accounting,

every transaction has two effects – one debit

and one credit.

This means for every business transaction

one A/c is debited and one A/c is credited.

42.

The 3 mainrules

For nominal accounts i.e. incomes and

expenses:

Rule 1:

“ Debit all expenses and losses & credit all

revenues, incomes & gains. ”

43.

The 3 mainrules

For personal accounts

Rule 2:

“ Debit the receiver and credit the giver.”

44.

The 3 mainrules

For real accounts i.e. for assets and goods

Rule 3:

“ Debit what comes in and credit what goes out.”

45.

Method of debitingand

crediting

1. Determine accounts associated with the

transaction.

2. Determine the type of account (personal,

real or nominal)

3. Record the transaction using rules of debit

and credit.

![Basic Terms

Current Assets

These assets are required to carry on the day to

day business activities.

Eg:

Inventories [raw material, work in progress & finished

goods]

Cash balance

Bank balance

Debtors

Receivables](https://image.slidesharecdn.com/accountsintro-250918062344-b00b957a/75/Basic-Introduction-to-Accounting-Terminology-20-2048.jpg)