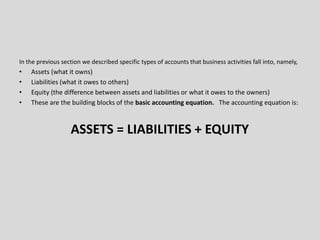

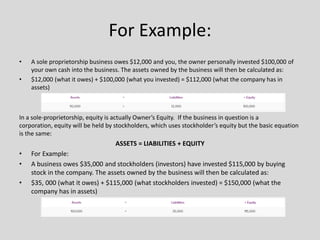

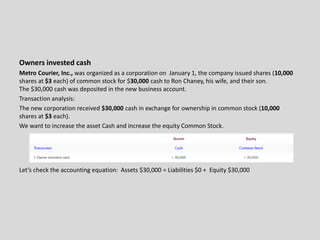

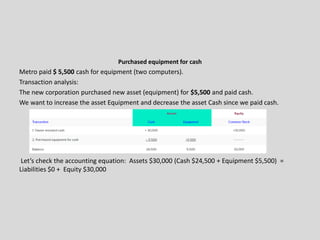

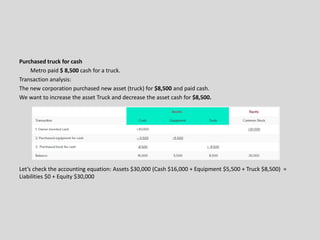

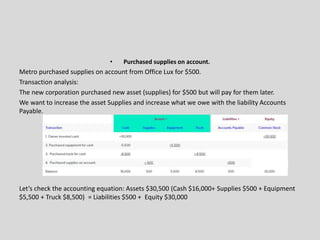

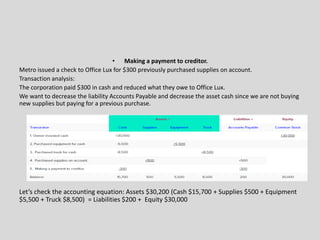

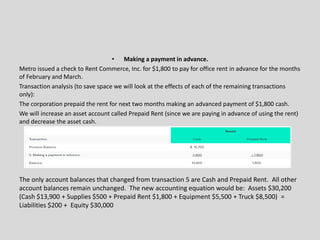

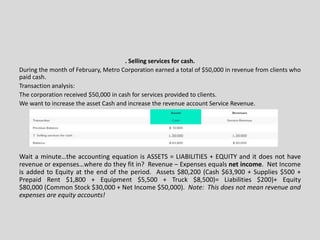

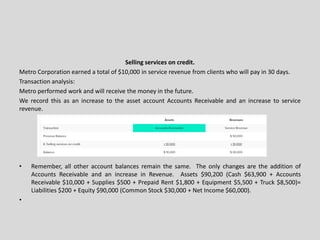

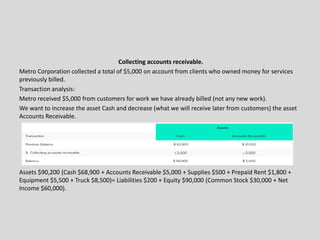

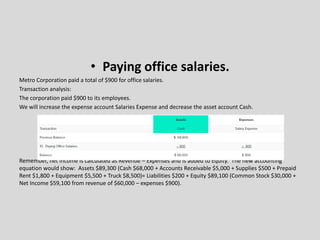

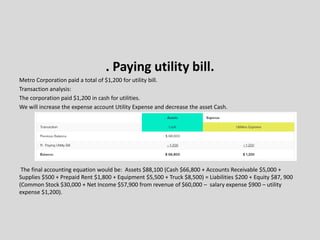

The document explains the basic accounting equation of Assets = Liabilities + Equity. It provides examples of common business transactions and their impact on the accounting equation. Transactions like purchasing equipment for cash, selling services for cash or credit, paying expenses, and collecting on accounts receivable are analyzed. For each transaction, the impacted accounts and the new accounting equation are presented to demonstrate the balancing nature of double-entry bookkeeping.