Assessing ABS players table

This document outlines the key players involved in a securitization transaction and their contractual duties and disclosure requirements. It discusses the originator who initiates the securitization program to lower borrowing costs, the debtors whose payment experience is important to the success of the program, and the investors who purchase the securities issued by the special purpose vehicle (SPV). Other players covered include the arranger who designs the transaction structure, underwriters who market the securities, auditors who provide financial confirmation, the depositor who transfers assets to the SPV, lawyers who ensure legal efficacy, and the SPV itself which issues securities to fund asset acquisition. For each player, the document specifies required disclosure documents and the types of information that must be disclosed.

More Related Content

What's hot

What's hot (19)

Viewers also liked

Viewers also liked (20)

Similar to Assessing ABS players table

Similar to Assessing ABS players table (20)

More from Arthur Mboue

More from Arthur Mboue (20)

Assessing ABS players table

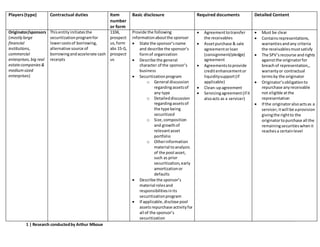

- 1. 1 | Research conductedby Arthur Mboue Players (type) Contractual duties Item number or form Basic disclosure Required documents Detailed Content Originator/sponsors (mostly large financial institutions, commercial enterprises, big real estatecompanies & mediumsized enterprises) Thisentity initiatesthe securitizationprogramfor lowercostsof borrowing, alternative source of borrowingandaccelerate cash receipts 1104, prospect us,form abs 15-G, prospect us Provide the following informationaboutthe sponsor State the sponsor’sname and describe the sponsor’s formof organization Describe the general character of the sponsor’s business Securitizationprogram o General discussion regardingassetsof any type o Detaileddiscussion regardingassets of the type being securitized o Size,composition and growthof relevantasset portfolio o Otherinformation material toanalysis of the pool asset, such as prior securitization,early amortizationor defaults Describe the sponsor’s material rolesand responsibilitiesinits securitizationprogram If applicable,disclose pool assetsrepurchase activityfor all of the sponsor’s securitization Agreementtotransfer the receivables Assetpurchase & sale agreementorloan (consignment/pledge) agreement Agreementstoprovide creditenhancementor liquiditysupport(if applicable) Clean-upagreement Servicingagreement(if it alsoacts as a servicer) Must be clear Containsrepresentations, warrantiesandany criteria the receivablesmustsatisfy The SPV’srecourse andrights againstthe originatorfor breachof representation,, warrantyor contractual termsby the originator Originator’sobligationto repurchase anyreceivable not eligible atthe representation If the originatoralsoactsas a servicer,itwill be aprovision givingthe rightto the originatortopurchase all the remainingsecuritieswhenit reachesa certainlevel

- 2. 2 | Research conductedby Arthur Mboue Debtor (anytype of customersof the originator-each personliable forthe full orpartial paymentor performance of any loanor debt whethersuch personisobligated directly, indirectly, primarily, secondarily,jointly or severally) Theyare the originator’s obligors. Theircreditscores and historicpayment experience are nucleustoa successof the full ABS program. Theydo notneedto be notifiedof,consenttothe transferof the receivables because theyare not participatingpartiesinthe securitizationprogram. Estimate of lossesor allowance forlossesrequires considerationof historical loss experience adjustedfor currentconditionand judgmentsaboutthe probable effectsof relevantobservable data includingpresent economicconditionssuchas delinquencyratesforhealthof specificcustomersandmarket sectors,collateral valuesand the presentandexpected future levelsof interestrates. The underlyingassumptions, estimatesandassessments usedto provide forlossesare updatedperiodicallytoreflect currentconditions. These assessmentsare subjectto regulatoryexaminations whichcan resultinchange to these assumptionsorworse. 1112, prospect us,FWP, 10-D, 10- K Provide informationabout each significantobligorand the nature of the obligation For obligorsthatare notABS issuers,provide information o Summaryfinancial informationfor10% obligors o Auditedfinancial statementfor20% obligors If the obligorisAnissuing entityof ABS:the discussion requirementunderitems 1104, 1115, 1117, and 1119 of RegAB applied Bill Sale notice orsale agreement Lease or rentcontracts Itemnumber Warranty duration of buyer Price agreedon AgreedInstallationpayments Investors(financial institutions, insurance companies,pension Purchase the securities issuedbythe SPV Receive interestand principal paymentsfrom Prospect us,1111 To enhance theirknowledge of the ABSbefore any investment,investorswould alsorelyon Securitypurchase agreement Securitytrustdeed (certificate) Index of stockpurchase agreement o Definition o Sale and purchase of

- 3. 3 | Research conductedby Arthur Mboue funds,hedgefund and wealthy individuals) the payingagentas scheduled o State of Pool assets o Tax matters o Legal proceedings Pool assets: Describe the pool assetswith a tabular representationof average pool tosales, average balance,weighted average coupon,average age,remainingterm,average loanto value or simple ratio and weightedaverage standardizedcreditscore or otherapplicable measureof obligorcreditquality o Describe the typesof pool assetsto be securitized o Describe material termsof the pool assets o Describe solicitation, creditgranting o Provide the method and criteriabywhich the pool assetswere selectedforthe transactions o The cut-off rate or similardate for establishingthe compositionof the assetpool,if applicable o Identifybrieflylegal and regulatory provisions o Provide the nature Stock certificates Offeringmemorandum Investorqualification questionnaire (forPPM) Subscriptionagreement Agreementtobecome a party to shareholders shares o Representationand warrantiesof seller o Representationand warrantyof buyer o Certaincovenants o Conditions precedent o Terminationpolicies o Indemnification

- 4. 4 | Research conductedby Arthur Mboue of the reviewof the assetsperformedby an issueror sponsor o Disclose whichentity determinesthat those assetsshould be includedinthe pool despite o Provide atabular presentationof the pool asset characteristics Chosenby the sponsorofthe program Arranger/structurer (financial institution) Designthe structure of the program Designthe structure of the riskprofile of the receivablesinorderto create tranchesand their sequentialpayments schedules Designa creditarbitrage strategy Arrangescredit enhancement Designa liquid strategy Designa profitextraction method List andmake arrangementof counterpartiestotake on risks Ensuresthat the transactionproceeds througheach step is closed Make agreementwithfirst buyersof the securities prospectus Disclose the arrangername and itsformof organization Describe the characterof the arranger business Describe the arranger material rolesand responsibilitiesinits securitization Disclose the arranger relevantfactsits participationinstructuring the transactions Disclose the arrangerother informationincludingthe size,type andgrowth Disclose the arranger’s experience andthe period of time thatthe arranger has beenengagedinthe securitization Subscriptionagreement Agreementbetweenthe corporationand investmentbankers Agreementamong bankers Agreementsbetween investmentbankersand underwriters,dealersor QIB Offeringmemorandum, prospectus(offering circular) Purchase agreement betweenthe company and the initial purchasers Legal opinionsand Comfortletters Provisionsrelatedtothe initial purchase price forthe securitiesonthe issue date, subjecttoconditionsrelating to o The SPV’slegal status o Listingandrating of the securities Provisionrequiringa cancellationof asale to investorsif amaterial adverse eventoccurs betweensigningthe subscriptionagreementand closingthe securitiesissue

- 5. 5 | Research conductedby Arthur Mboue Underwriter Managers (financial institution) Exercise agreementas firstbuyerof the securities If it is a PPM, select qualifiedinvestors Market the securitiesto the investors,brokersand qualifiedbuyers prospectus Indicate the underwriter name and addressand telephonenumberof its registeredoffice Describe the characterof itsbusiness List all the typesof underwritersinvolvedin thissecuritizationandtheir duties Describe the permissible activitiesandrestrictions on the activities Disclose the total amount of feestobe paid Provide informationabout originator’sunderwriting criteriaforthe assettypes Disclose the anticipated schedule forthe offering and descriptionof market events Describe the procedures by whichthe underwriter will conductthe offering and the proceduresfor transactionsinconnection withthe offeringwithan underwriterand participatingdealer Agreementbetweenthe sponsorand underwriters Agreementbetweenthe underwritersanddealers Provide information aboutoriginator’s u8nderwritingcriteriafor the assettypes Disclose the anticipated schedule forthe offering and descriptionof material events Describe the procedures by whichthe underwritingwill conduct the offeringand the proceduresfor transactionin connectionwiththe offeringwithan underwritingor participatingdealers Agreementamong underwriters(AAU) Underwriters questionnaire and responses Numberandtype of securitieseachmanagerhas agreedto buy Paymentandallocationof the managers’commission Delegatespowertothe arranger/leadmanagertoact on behalf of the syndicate Auditors (Accountingfirms, mostlybig4, kpmg, PWC, Ernst & Young and Deloitte) Provide confirmationof financial informationin relationtothe SPV,and any guarantors,andthe receivablesthemselves Involvedinthe latestaudit reportand financial statementsof the vehicle Provide the name of the auditingfirm Describe itsmaterial role and responsibilitiesinthe securitization Provide the general character of its business and itsactions Auditingagreement Discussionwiththe independentauditor report Reportfrom management Comfortletters Addressedtounderwriter managers o 1st at the time of signingof subscription agreement o 2nd justbefore completion

- 6. 6 | Research conductedby Arthur Mboue For newlyincorporated SPV, reporton itsposition immediatelyfollowingthe securitization Provide the due diligence results(change ornot) Carry-outthe financial modelingof the cashflows Conductand disclose the resultsof financial analysis of the collateral File the required reportto be includedinthe offering and disclosure documents Disclose the auditorreport Disclose if auditoropinion isunqualified,qualified, adverse ordisclaimer Provide fees,directand indirectandall the engagementtobe paid (fee andexpensestable) It mustbe dated,signed and state of certificationof the leadauditoror firm SAS59 requiresauditorto evaluate goingconcernfora reasonable time with explanationparagraphif neededtoenhance managers’knowledge o Discussthe degree of independenceof the auditorand auditor’s consentduringthis assessment o State reasonsfor the offering o Confirmsthe reliabilityof the unauditedfinancial information The report must o Be dated o Be manuallysigned o Indicate the cityand state o Identifythe financial statementand reportsthat theydid cover o Must followPCAOB standards Depositor (originatoritself or any financial institution) A SPV acts as a depositor and registrant. Conveys,assigns,receives, purchasesandtransfersor sellsthe pool of assets (real,personal andmixed, whereverlocatedand howeveracquired) or receivablestothe issuing SPV 1106 If it is differentfromthe sponsor, o Provide its ownership structure o Provide general character of its activities o Discussits continuingduties Purchase and assumption agreement Purchase price Manner of conveyance Warranty provisions Recourse provisions Paymentdate Servicingprovisions Reversal clause Agreementwithrespectto safe deposit Governinglaw

- 7. 7 | Research conductedby Arthur Mboue afterissuance Successionprovision Securitiesfinance lawyers (lawfirms specializedin financial transactionsand securitieslaw) Ensure a legal efficacyof the structure Advise onthe legal and regulatoryaspectsof the structure Advise onthe tax aspects of the structure Draft and negotiate the legal documents andcases Establishthe relevant legal entities Reviewthe corporate capacityand authority (includingdelegationof authority) of eachparty prospectus Provide name of the law firmand itsexpertise and experience relatedtothis type of securitization Describe the formmaterial contractual dutiesinthe securitization Provide the nature,terms and limitationsof its contractual agreement Retentionagreement Legal opinion Comfortletters All contractual agreements shouldinclude opinionson o each party’scapacity and authority (includingdelegation of authority) toenter intoa transaction o whetherthe transaction documentshave beendutyexecuted and representlegal bindingand enforceable obligations o whetherthe requisite consents and authoritieshave beenobtainedand registrationsmade timely o whetherall legal formalitiesforthe transferof receivableshave beencompliedwith o whethersecurity interestare effective o whetherchoice of lawand state of organization provisionare effective o tax treatmentfor each jurisdiction Issuer- Special Purpose Vehicle (establishedbythe Thisis a pre-existingor newlycreatedSPE(mostly a trust but alsoa LLC, LLP 1107, 10-K Describe thisentityandits formof organization Describe itspermissible almostall agreements Offeringcircular: termsand conditionsof the securities

- 8. 8 | Research conductedby Arthur Mboue originatorandthe structurer) or corporation) forthe purpose of the securitization. Itisthe nucleusof the securitization. Itissues securitiesinPPMor public offeringmarket. It buysor receivesthemas a loan In case of sale,the originatorwill remove themfromits legal control and portfolio It alsoissuesdebt securitiestothe investors to fundthe acquisitionof beneficial interestrights activitiesanddiscretionary activitieswithregardto the administrationof the assets Describe anyassetsowned or to be ownedbythe issuingentity Describe itsboardof directorsor the like,if applicable Describe the capitalization of issuingentityandthe amountof anyequity contributingtothe entity Describe sale andtransfer of the pool assetstothe issuingentity Describe anyarrangement, provisions,expensesand bankruptcy provisions informationaboutSPV informationonthe underlyingassetson which the securitizationisbased mustcomplywithlegal requirementsapplicableto securitiesofferingsineach jurisdictionwhere securities are listedandthe jurisdiction where the SPV is incorporatedororganized Chosenby the SPVleadership Security Trustee (professional corporate trustee) He isthe guardianof the trust certificatesissuedto newownersof securities Holdscertificatesaccounts before distributiondate Makes paymentto investors Holdsnote and securities documents Holdsand drawson reserve fund Advancesonbehalf of Master servicer,if necessary Maintainscertificate register 1109 Some disclosure relatedto Trustee mayapplyto them trust deed Provisionsabout the securityinterestoverthe assetsmakingupthe security package Securitytrustees enforcementpowersand rightsto deal withthe assets comprisingthe security package

- 9. 9 | Research conductedby Arthur Mboue OverseesMaster servicer’sperformance Representsinterestof all certificate holders Holdsand reinvests reserve fundamounts, payoutexcesstothe originatororinvestors(it dependsoncontractual agreement) Calculatespaymentsof certificate holders Trustee (appointed corporate trustee) isappointedtolookafter the interestsof the investors. can holdassetsgrantedto investorsandbenefit (includingbeneficial interests) of covenantand rightsinthe securitization on behalf of the investors. has fiduciaryduty obligationtowardthe investorstosafeguardthe assetspledgedas collateral.Leadedbya Master, trusteescan conferreal and discretionaryrightstothe investorsbeneficiariesof the trust. 1109 Disclose the trustee name, itsduties,responsibilities and itsformof organization Describe the trustee prior experience Disclose anyactionsthat wouldbe requiredbythe trustee uponan eventof default,potential eventof defaultaswell asrequired percentage of a classor classesof ABS thatis neededtorequire the trustee totake action Describe anylimitationson the trustee’sliabilityunder the transaction agreementsregardingthe ABS transaction Disclose anycontractual provisionorunderstanding regardingthe trustee’s removal,replacementor resignationaswell ashow the expensesassociated securitytrustdeed Trust Certificate SPV’scovenantstopaywhich runs parallel withthe SPV’s promise topay inthe certificatesrepresentingthe securities SPV’sfurthercovenants, representations and warrantiesforthe benefitsof the investors Schedule of termsand conditionssetout inthe offeringcircularandthe form of certificatesrepresenting the securities

- 10. 10 | Research conducted by Arthur Mboue withchangingfromone trustee toanothertrustee will be paid Chosenby the structurer/arranger or trustee ofthe SPVon behalfofthe SPV Paying agent (major bank) Setout agentpowers, duties Setout documents policies concerning paymentstoinvestors prospectus Provide the name of the payingagentand itsform of organization Describe the payingagent material rolesand responsibilities inthe securitization Provide the general character of its contractual agreement Provide itsexperience in the securitizationand indicate astatementor reportincludedattributed to such experience includingprioractions Provide feesandexpenses tablesindicate toeach itemandits purpose Payingagency agreement Setsout techniquesfor paymentstoinvestorsof principal andinterests Mechanismto exchange or replace damagedorlost certificates Servicer(alsoacts somethingas receivingandpaying agent,originator itself or) Collectingprincipal, interestandescrowfrom the borrowers o Late paymentfees o Legal document prepaidfee o Float o Otherdue to the issuer(servicer) Payingtaxesand insurance fromescrowed funds Monitoringdelinquencies Workouts/restructurings Executingforeclosures 1108 Provide servicing experience of the company o General o Relating toassets of the type being securitized Discussmaterial changes in servicingpoliciesduring past 3 years Discussinformationabout financial condition,if material Provide material termsof servicingagreement o Advancing Servicingagreement Cleanupagreement(if it alsoplaysan originator duties) Main dutyto collectamounts due underthe receivables contracts Procedures andactionsto be takenagainsttroubled debtors Provisionsabouttroubled debtormanagement (includingdefaultnotice, collectiontimeline and notices,repossessionand liquidation)

- 11. 11 | Research conducted by Arthur Mboue Remittingfeesto guarantors,trusteesand othersprovidingservices In some case including revolvingstrategy, investingfunds temporarilypriortotheir distribution Accountingforand remittingprincipal and interestpaymentstothe holdersof beneficial interestsinthe financial assets o Proceduresof handling delinquentand defaultedassets o Abilitytowaive or modifyfees o Abilityto documentcustody Provide limitationson servicer’sliability Discussback-upservicing arrangements Investment manager (collateral managerand 3rd party investment managementfirm) The portfolioof receivablesunderlyingthe securitizationrequires active management o Determine the assetsmakingup the portfolioboth initiallyandonan ongoingbasis o Negotiate and enteragreements for the acquisition, managementand sale of receivables o Deal with valuationsof the portfoliorequired by the SPV o Complywith reporting requirements relatingtothe assetportfolio Prospectus, FWP Provide the name of the investmentmanagerand itsform of organization Describe the investment managermaterial roles and responsibilitiesinthe securitization Disclose there any restrictiononthe manager duties Disclose general character of itsbusinessactivities Provide the nature and termsof itscontractual agreement Provide total amounts fees,directandindirectto be paid Investmentmanagement agreement Vendortradingpartner agreement Strict eligibilityguidelinesin respectof the assetsthat may formpart of the portfoliowhichthe investmentmanagermust complywith eventstriggeredthe replacementof the manager compliance withstrict investmentmanagement reportingrules

- 12. 12 | Research conducted by Arthur Mboue Paidon a percentage basis plusotherdiscretional incentive Can be requiredtoholda juniortranche inorderto share riskand raise confidence andvalue of the securitization Collateral administrator (independent3rd party,a bank) agenthiredto administer the portfolio Maintainsa database detailingthe contentof the portfolioanduses to o Run performance tests o Provide reportson the underlying assets o Obtainvaluations of the underlying assets o Calculate payment and receipt requirements o Openand administerbank accounts o Directpayments to be made accordingto the transaction documents Prospectus, Form S-3, FWP Disclose the name of the collateral administrator and itsform Describe the collateral administratormaterial contractual agreement Disclose termsof any administrationagreement regardingissuingentity Provide itsexperience in the securitization Collateral Administration agreement Poweranddutiesof the collateral administratorand the collateral manager provisions Theircompensationsclauses Termsof theirduties provisions Termination,resignationand appointmentof successor provision Representation and warrantiesprovision Governinglawclause (‘this agreementshall be constructedinaccordance withand thisagreementand any mattersarisingoutof or relatinginanyway whatsoevertothis agreement,incontract,tort or otherwise,shallbe governedbythe lawsof the State of…’) Bankruptcynonpetition, limitedrecourse clause Assignmentof issuer’srights provisions Jurisdictionclause signatures

- 13. 13 | Research conducted by Arthur Mboue Swap counterparty (Wall Streetfirm specializedin derivatives) It can serve as eithera brokeror a dealer As a broker,thisbank matchescounterparties but doesnotassume any of the risksof the swap transactions As a dealer,the swapbank acceptseitherside of the currencyand thenlater reducestheirrisksor matchesit with counterparty It can line upbehindon the sequential payment schedulesagreementwith the investors asa residual classowner A swapis a derivative whentwocounterparties agree to a contractual agreementtoexchange cash flowsatperiodic intervals 1115 Disclose the name of the of the swap counterpartyor calculationagent Disclose the name of the derivative counterparty Disclose whetherthe significance percentage is lessthan10%, at least10% but lessthan20% or 20% or more Describe amaterial provisionsregarding substitutionof the derivative counterparty Disclose itsdetermination of anyAmountof derivatives Disclose,insertandfile the swapagreementasexhibit Disclose total fees,direct or indirecttobe paid File the agreementrelating to the derivative instrumentasan exhibit Swapagreement documents o General o Early termination o Taxation o Rating downgrade or withdrawal o Creditsupport agreement o Interestdeferral o Transfers Provisionaboutdetailedrisks and eventsleadingtoa swap Provisionaboutcredit defaults,swaparrangement, swapcounterpartyand premiumpayment Provisionsaboutrisksharing arrangementsinclude price adjustmentclause,neutral zone,outside neutral and zerocost insurance clauses. Monoline Insurer (Monolineinsurance company and large insurance specialized as providerof financial obligation,credit enhancers) An insurance policywitha monoline andirrevocable agreementtopayinterest and principal atthe originallyagreedschedule payments Monoline insurersaimto minimize the riskby o Acceptingonly selected investmentgrade program o Usinga deterring toughanalysisand 1114 Disclose the name of such enhancementproviderand the nature of businessof the monoline insurer Disclose anyactionsthat wouldbe requiredbythe monoline insureruponan eventof defaultand potential eventof default Disclose anylimitationof thiscontractual agreement Disclose anycontractual provisionorunderstanding regardingitstermination, Insurance policy agreement Commonpolicydeclaration Policynumber,effective date,expirationdate Name of the insurance companyand broker Premiumforeachcoverage Commonpolicycondition Cancellationterms Changes examinationof booksand records inspectionsandsurvey transferrights

- 14. 14 | Research conducted by Arthur Mboue due diligence process o Maintaina diversified portfolio In evaluatingthe overall creditworthinessof the monoline,ananalysis mustevaluate the adverse change in cash flow waterfall andthe sufficiencyof the monoline cashreserves and capital,ratingactivity, whetherthe monoline is indefault,inthatred zone or defaultappears imminentandthe potential forintervention by an insurance orother entities resignationorreplacement Describe the methodused for calculation,coveringa least5 fiscal years o Aggregate principal amount of all guarantee o Reserve ratio o Recoveryrate o Loss rate o Claimrate coverage parts Clearinghouses (Depositary Trust& clearing corporation or Fedwire) Provide clearingand settlementservicesforthe securities prospectus Disclose the name andthe nature of the businessof the clearinghouse Identifyeachclearing house usedandany minimumamountthat mustbe assignedasa conditionof the transaction Discussany arrangement to keepthisamount outstanding Disclose anyrightsrelated to any excesscash Disclose anyrequirement inthe transaction agreementstomaintaina Insurance clearinghouse service (ICS) agreement Vendortradingpartner agreement Fedwire testinginstruction o Institutionname o ABA number o Testcontact name o Type of test o Teststart date Fedwire FundandFedwire securitiesservice form(3rd party service arrangement, operatingcircular)

- 15. 15 | Research conducted by Arthur Mboue minimumamountof excesscashflowor spread fromor retainedinterest in,the transactionand any actionsthat wouldbe requiredorchangesto the transactionstructure that wouldoccur if such requirementswere not met Rating agencies (Standardand Poors,Moody’s investorservices, Fitchratingsservice or Duff&Phelps CreditratingCo) Ratesthe securitiesto opinion whetherthe SPV has a strong or weak capacityto pay interest and principal whendue The rating isprovided afterdetailedstatistical analysisonthe probability of defaultandthe effects of suchdefaultonthe abilityof the SPV to complywithitspayment obligationsinrespectof the securities 1120 Disclose whetherthe issuance orsale of any classof offeredsecuritiesis conditionedonthe assignmentof acredit ratingagencieswouldbe useful informationto investors Identifyeachratingagency that isusedand the minimumratingthatmust be assignedasa condition of the transaction Discussany arrangement to have that rating monitoredwhilethe ABS are outstanding Include astatement explainingthatthe ratingis not a recommendationto buy,sell orholdsecurities Disclose if the arrangerand sponsorhas obtaineda preliminaryratingtothat classof ABS Partnershiportrust Deedor certificate of incorporation Copyof the Board resolutionauthorizing the rating Copyof the Bylaws Copyof the projectto be rated Copyof all financial statementsforthe last3 fiscal years Additional documents underrequestfromthe ratingfirm CIKnumber Usually,if the issuerdoesnot requestthe rating,Moody and S & P will simplydothe ratingon the basisof the publiclyavailable informationanddiscloseitto the public Fitchand Duff Phelpshave onlydone solicitedratingof any type of securities Fees o Onetime fee to requestrating anytime o S&P ($25,000 to $125,000) o Moody’s(~$ 130,000) Listing agent(law formor company specialized inlisting Researchandlistthe companyor its shareson the national securities prospectus Provide the name andthe nature of the businessof the listingagent Draft Form 8-A Listing applicationfor debenture In lieuof Form8-A,other formscan be usedincluding Form 10

- 16. 16 | Research conducted by Arthur Mboue inexchange) exchange Setout the detailsof the listingstrategies Disclose towhatextent the listingagentrelyonthe company’saudited financial reports Disclose if the listingagent didrequestrelated shareholdersdata Disclose of the listingagent didfindthe securitizer’s resourcessufficientto meetitsobligations Disclose whetherthe listingagentdidfindany conflictof interestarising fromthe securitizing transactions Disclose whetherthe listingagentdidverifyany accuracy of the transactions Disclose anylimitations arisingfromthe listing agent’scontractual duties Statementof understanding Policiesandprocedures, instruction Listingapplicationfor AmericanDepositary Receipt Rule 315 letter o 8 copies,one is manuallysigned Stock exchange (NYSE,NASDAQ, JapanExchange group,Euronext, LondonStock exchange group, Hong Kongstock Exchange,TMX (Canada),Deutshe Bourse) Servesasa global platformtotrade securities withelectronic, anonymous andhybrid trades Maintaina bodyof rules to regulate itsmembers prospectus Provide the name andthe nature of the national securitiesexchange Disclose if youwill notlist the securities Disclose where the trading will be developed Copyof Charter Copyof By laws or Partnership,operating agreementorTrust deed Descriptionof registrant’ssecuritiesto be registered Certifiedcheckpayment of the registrationfee Copiesof the latest definitionof proxy, annual reportto the shareholders,annual reportfiledtoSEC and quarterreportsfiledto Afterthe program:the companymustfile 2 copies of final listingapplication

- 17. 17 | Research conducted by Arthur Mboue SEC Copyof Board resolution authorizingthe securitization (certificate of secretary as to adoptionof resolutions) Copyof shareholders resolutionauthorizing the issuance of securities for listing Copyof specimen certificate (if needed) Copyof goodstanding certificate from jurisdictionof the entity Letterto NYSE fromthe companyGeneral counsel Copyof thisletterfor filingstamp(along addressedstamped envelope) Liquidityfacility provider Setsout the detailsof the liquiditysupportfacility Thisis a lenderunder short termbasisin relationtocertain tranchesof the issued securities prospectus Disclose the name of the liquidityfacilityprovider, itsbusiness andits material rolesinthe securitization Provide the nature and termsof itscontractual agreement Disclose anylimitationson the liquidityfacility providerunderthe provideragreement regardingthe ABS transaction Provide asummary Liquidityagreement Detailedof the standardloan agreementtermsand conditionsincludingthe amountof the loanfacility and the eventsleadingto theiruses For tax reason,the jurisdictiondoesmatter

- 18. 18 | Research conducted by Arthur Mboue financial informationof the liquidityprovider Disclose if there isany custodianintermediate transferorandliquidity providersinthe secondary markets Disclose anymaterial termsof anyagreement withthat partyregarding the ABS transaction Credit enhancement provider Use as a financial technique toimprove the creditworthinessof the issuedsecurities Guaranteespaymentof all contractual cash flow waterfall withinvestors for interventionwhenthe defaultappearsimminent prospectus Describe externaland internal enhancement For external enhancement providers o Describe the providerandits business o Summaryfinancial informationfor 10% provider o Auditedfinancial statementfor20% providers Creditenhancement agreement Subordinationclause Reserve accountsclause Demandnotes clause Lettersof creditclause Suretybondclause Guaranteedinvestment contract clause Swapsor otherinterestrate protectionagreement Repurchase obligations