BASED ON THEVIDEO

PRESENTATION,

WHAT IS ECONOMICS?

5.

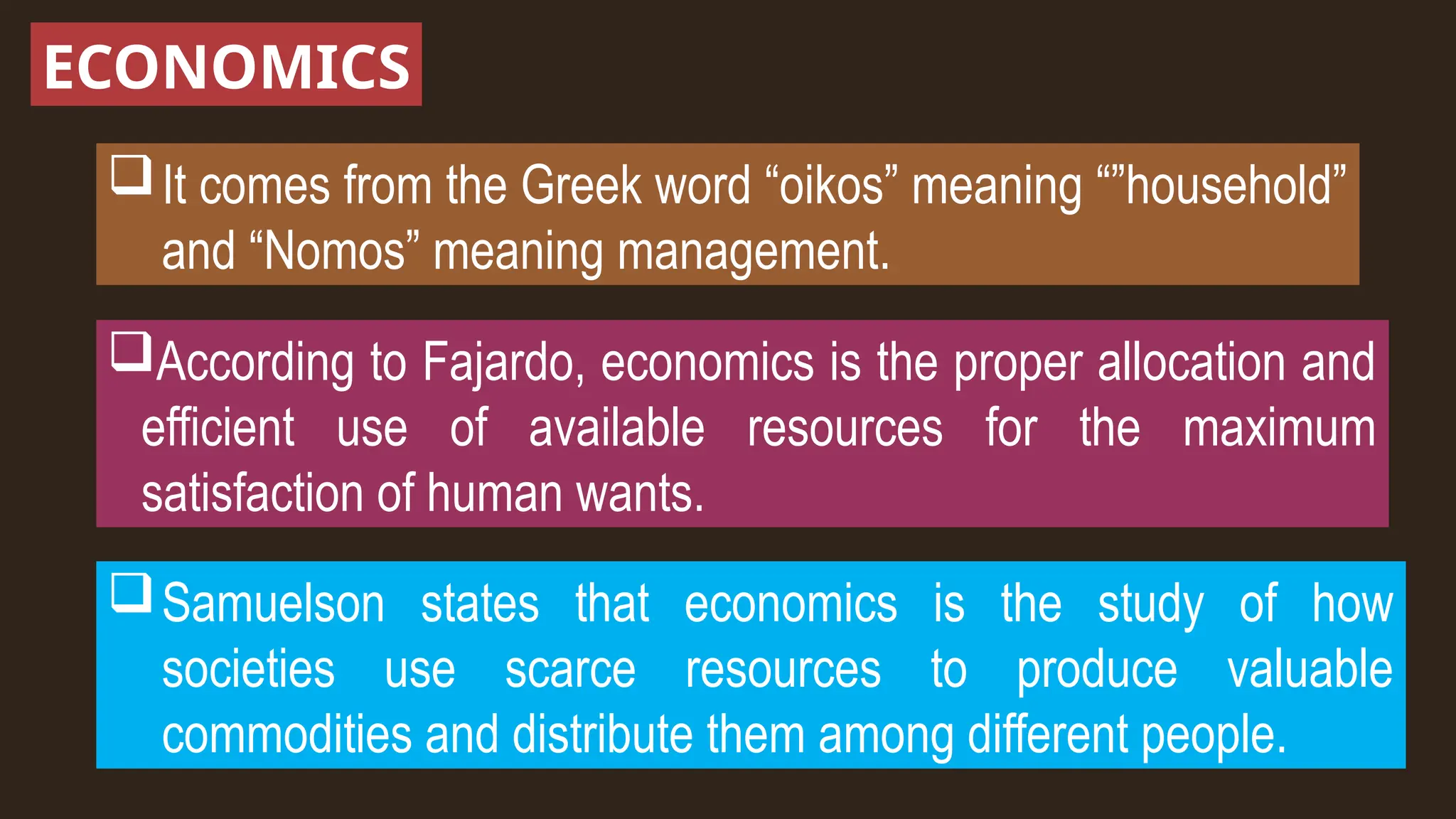

ECONOMICS

It comes fromthe Greek word “oikos” meaning “”household”

and “Nomos” meaning management.

According to Fajardo, economics is the proper allocation and

efficient use of available resources for the maximum

satisfaction of human wants.

Samuelson states that economics is the study of how

societies use scarce resources to produce valuable

commodities and distribute them among different people.

6.

Ultimately, economics isdedicated

to figuring out how society manages

its limited resources.

Why "limited"? Because we can't

have everything we want!

from theGreek word mikros, meaning “small”)

It zooms in on the behavior of individual parts of the economy. It

focuses on how individual households, firms and industries

make their choices, and the interaction of such decisions in the

particular market.

SCOPE OF ECONOMICS

9.

SCOPE OF ECONOMICS

How households (like your family) make decisions about what

to buy.

How firms (businesses) decide what to produce and at what

price.

How industries (like the rice industry or the tech industry)

operate in specific markets.

10.

Example: If we'restudying the price of rice in a local

market – how much it costs, how much is produced,

and how government rules or taxes affect it – we're

looking at microeconomics.

SCOPE OF ECONOMICS

11.

from theGreek word makros, meaning, “Large”

Deals with the problem of the economy as a whole. It looks at

aggregate prices, production, and income.

SCOPE OF ECONOMICS

12.

Example: Studying the

Philippineeconomy's

total income (Gross

National Income) or

total employment

levels.

SCOPE OF ECONOMICS

Looking at

economy-wide issues

like inflation (prices

going up),

unemployment rates, or

how fast the economy

is growing (GDP).

It is theuse of inputs for generating output.

This is all about creating goods and services.

U T O N R O C I P D

PRODUCTION

16.

PRODUCTION

o Inputs: Theseare the "ingredients" or resources (like labor,

land, materials) used to make something.

o Outputs: These are the final goods and services that come

out of the production process.

o The Big Question: Society has to decide what to produce (Do

we make more phones or more food?) and how much of it.

CONCERNS OF ECONOMICS

17.

Once goods andservices are produced,

how are they shared among the people in society?

I T R I D T U N O I S

B

DISTRIBUTION

18.

DISTRIBUTION

o This islinked to the question: For whom are these goods

and services being produced? Is it for everyone, or just a few?

CONCERNS OF ECONOMICS

19.

It is theuse of products or services.

It is also the final conclusion of economic operation.

N O C M S U P N O I T

CONSUMPTION

20.

CONSUMPTION

o It's the"end game" of the economic

process – when someone finally uses what

was produced.

CONCERNS OF ECONOMICS

21.

It is concernedwith government spending and revenue.

This focuses on the government's role in the economy.

C L U B P I

A N N E C I F

PUBLIC FINANCE

22.

PUBLIC FINANCE

o Itstudies how the government collects

money (through taxes, borrowing) and how it

spends it (on roads, schools, healthcare,

etc.).

CONCERNS OF ECONOMICS

24.

TYPES OF ECONOMICS

1.Household Economics

o Focus: How individual families and households

make economic choices.

o What it looks at: How families manage their limited

money, time, and skills to buy what they need and want,

and to improve their well-being.

25.

TYPES OF ECONOMICS

2.Business Economics

o Focus: How businesses use economic principles to

make smart decisions

o What it looks at: Analyzing problems, improving

efficiency, and maximizing profits for companies.

26.

TYPES OF ECONOMICS

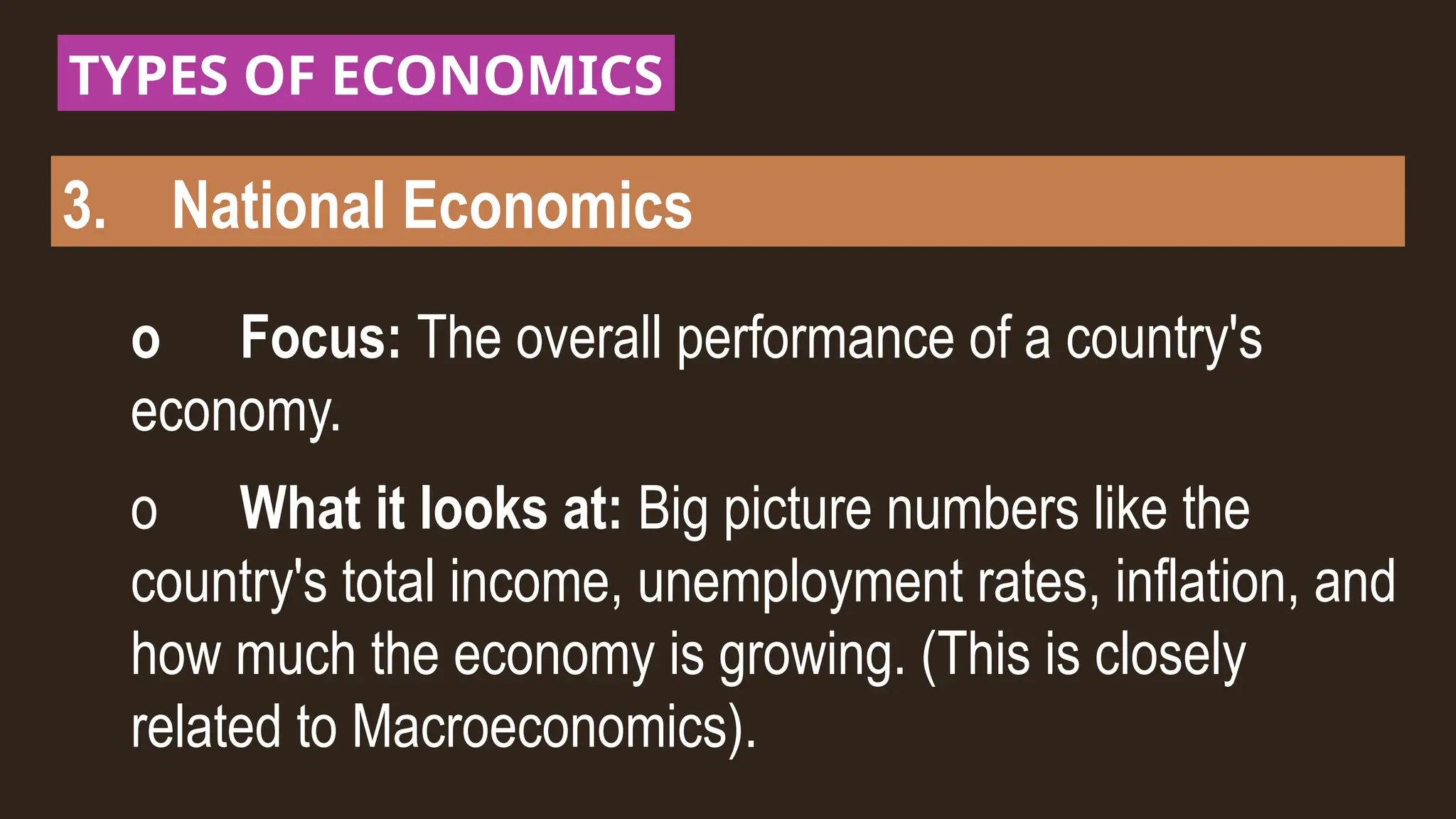

3.National Economics

o Focus: The overall performance of a country's

economy.

o What it looks at: Big picture numbers like the

country's total income, unemployment rates, inflation, and

how much the economy is growing. (This is closely

related to Macroeconomics).

27.

TYPES OF ECONOMICS

4.International Economics

o Focus: How one country's economy interacts with

others.

o What it looks at: Things like international trade

(buying and selling goods between countries), tourism,

and exchange rates (how much one country's money is

worth compared to another's).

THE ECONOMIC AGENTS/STAKEHOLDERS:

1. CONSUMERS

o These are the individuals or companies who buy and

use goods or services.

o They don't sell the item they purchased; they use it to

satisfy their needs or wants. (That's you when you buy a

new phone or a snack!)

31.

THE ECONOMIC AGENTS/STAKEHOLDERS:

2. PRODUCERS:

o These are the firms or individuals who create and

sell goods and services.

o They can be self-employed people (like a baker

who owns their own shop) or huge multinational

companies.

32.

THE ECONOMIC AGENTS/STAKEHOLDERS:

3. GOVERNMENT / PUBLIC

SECTOR:

o This group tries to maximize the well-being of

society as a whole.

o They interact with consumers and producers

within a specific location, culture, and environment,

shaping the rules of the market.

GOODS

anything used tosatisfy your needs and wants.

Intangible Goods

Tangible Goods

a physical object

or product that

can be touch

a product that

cannot be touch, like

insurance policy

35.

1. Consumer Goods:

oThese directly satisfy the needs and

wants

of consumers.

o Example: A slice of pizza, a pair of

shoes, a

CLASSIFICATION OF GOODS

36.

2. Capital /Industrial Goods:

o These goods help to produce other

goods or services. They indirectly meet

consumer needs.

o Example: The oven in a bakery (helps

produce bread), a machine in a factory, a

delivery truck.

CLASSIFICATION OF GOODS

37.

3. Essential Goods:

oThese are goods consumed to

satisfy the basic needs of people.

o Example: Food, basic clothing,

shelter, clean water.

CLASSIFICATION OF GOODS

38.

4. Economic Goods:

oThese goods are useful AND

scarce. Because they are scarce, you

need to pay for them. They have a

"value" and a "price."

CLASSIFICATION OF GOODS

39.

4. Economic Goods:

oThink: If something is so abundant that

everyone can have it without paying (like

fresh air in the countryside), it's "free." But

air-conditioned air is an economic good

because it's limited and costs money to

produce.

CLASSIFICATION OF GOODS

40.

5. Luxury Goods:

oThese goods are not necessary for

survival but are highly valued, often by

wealthy individuals.

o Reason for purchase: To show status,

for their high quality, or for their

craftsmanship.

o Example: A designer handbag, a

CLASSIFICATION OF GOODS

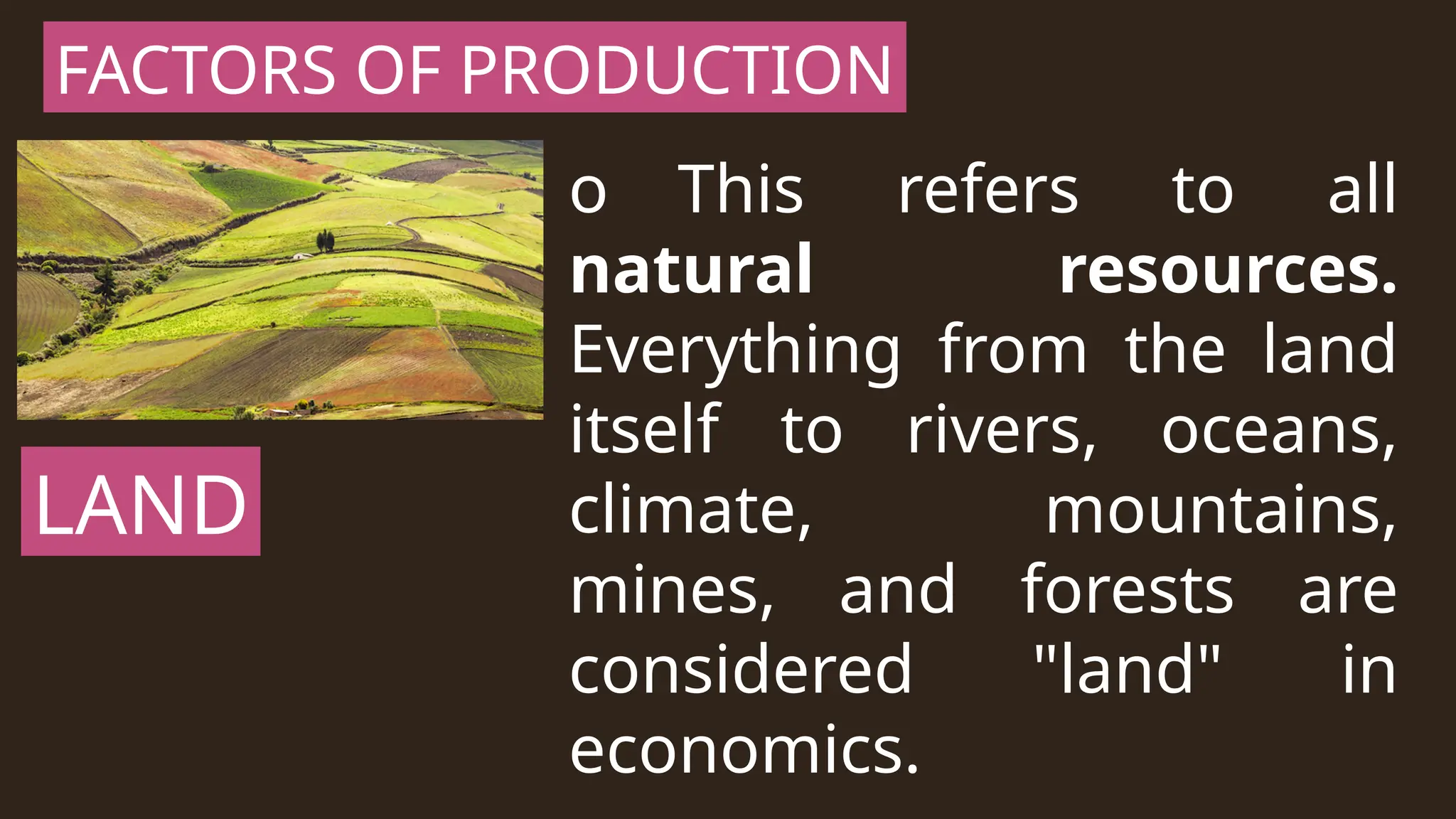

LAND

FACTORS OF PRODUCTION

oThis refers to all

natural resources.

Everything from the land

itself to rivers, oceans,

climate, mountains,

mines, and forests are

considered "land" in

economics.

49.

LAND

FACTORS OF PRODUCTION

oIt's the primary and

natural factor of

production – gifts from

nature.

o Payment for Land:

Rent.

50.

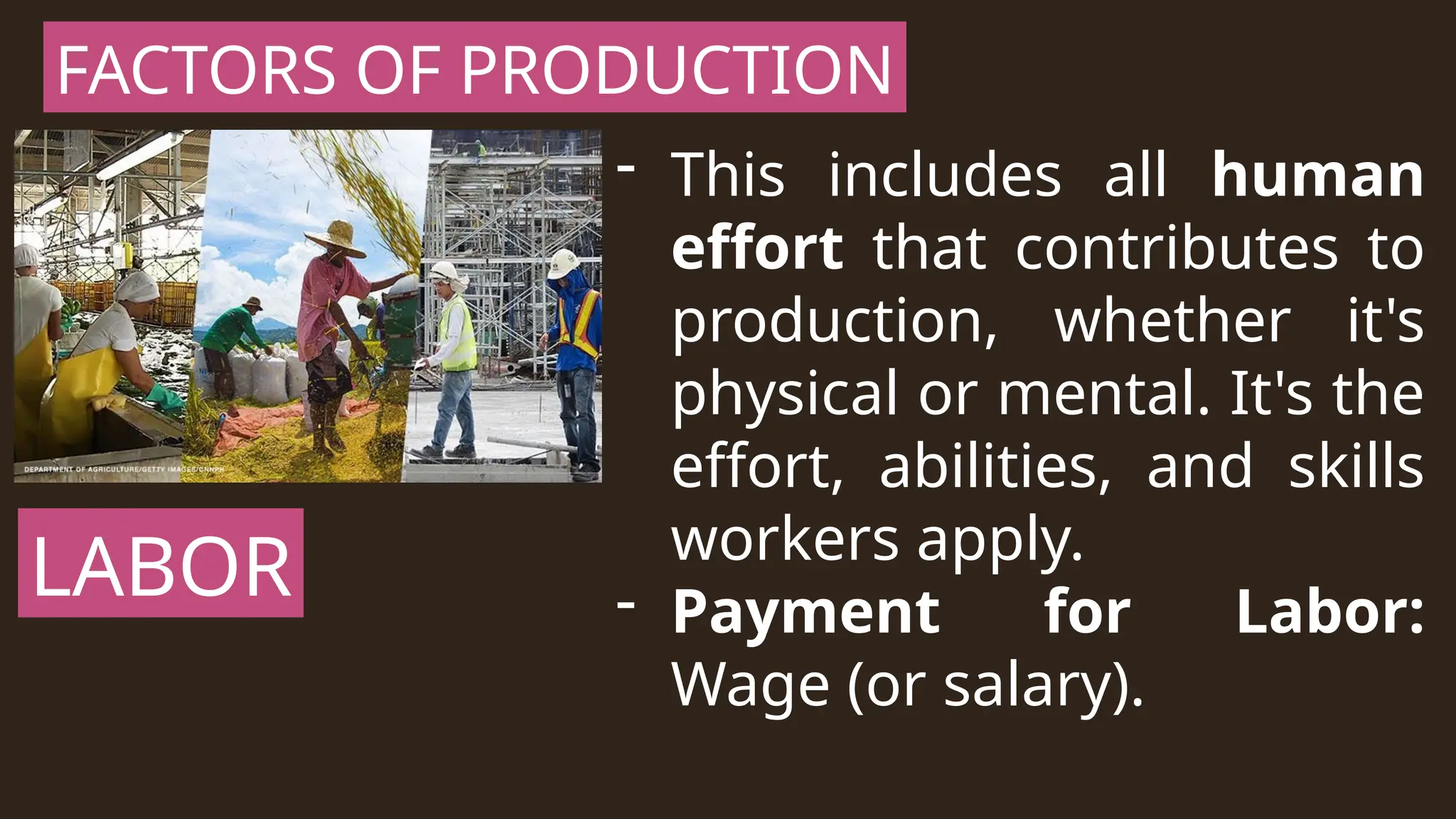

LABOR

FACTORS OF PRODUCTION

-This includes all human

effort that contributes to

production, whether it's

physical or mental. It's the

effort, abilities, and skills

workers apply.

- Payment for Labor:

Wage (or salary).

51.

CAPITAL

FACTORS OF PRODUCTION

-These are man-made items

used to produce other goods

and services.

- It's a "produced" factor of

production because it's

something we create to help

us create more.

52.

CAPITAL

FACTORS OF PRODUCTION

-o Examples: Factories,

machinery, tools, equipment,

raw materials, and even

money used for investment.

- Payment for Capital:

Interest.

53.

ENTREPRENEURSHIP

FACTORS OF PRODUCTION

-This is the special ability

to combine the other

three factors (land,

labor, capital) to create

something new or to

transform an idea into a

business.

54.

ENTREPRENEURSHIP

FACTORS OF PRODUCTION

-Entrepreneurs are often

innovative and willing to

take risks. They are the

ones who organize and

manage the production

process.

- Payment for

Entrepreneurship:

1. SCARCITY

Characteristics ofResources

This is the fundamental problem in economics: there's

simply not enough of everything to satisfy all human

wants. Our desires are unlimited, but our resources are

limited.

57.

1. PROBLEMS BECAUSEOF SCARCITY

Characteristics of Resources

Land: Not enough land, natural resources, pollution,

overcrowding.

Labor: Not enough skilled workers, insufficient overall workforce.

Capital: Lack of good equipment/machines, not enough funds.

Entrepreneurship: Not enough training for entrepreneurs,

limited opportunities,

fierce competition for

good ideas.

58.

2. MULTIPLE USAGE

Characteristicsof Resources

o Many resources can be used for more than one

purpose.

o Example: A piece of land can be used to grow

coffee, or you could build a factory on it. This forces

us to make a choice!

Choice and Decision-Making

Becauseof scarcity, we are constantly

forced to make choices. We have to decide

how to use our limited resources in the

best possible way to satisfy as many wants

as we can.

62.

Opportunity cost

the valueof the next best alternative that you give

up when you make a choice.

• Since resources are scarce, choosing one

thing means you can't have something else. The

opportunity cost is that "something else" you

missed out on.

63.

Opportunity cost

It helpsus make the smartest decisions by

understanding the true cost of our choices.

Example: If a mother decides to be a full-time

mother instead of returning to her job, the

opportunity cost is the salary she could have

earned. She chose the benefits of full-time

motherhood over the financial benefits of a salary.

64.

Importance of Economicsin our daily lives

It helps us understand:

How to earn a living

and manage our

personal finances.

How to earn a living

and manage our

personal finances.

o How businesses

make decisions and

maximize profits.

How societies

distribute resources

fairly.

Economics: A SocialScience AND an Applied Science

Economics as a Social Science

Focus: It aims to understand human

behavior – how people, families, businesses, and

governments make choices about scarce

resources.

Approach: It uses theories (like supply and

demand) to analyze how economies work.

67.

Economics: A SocialScience AND an Applied Science

Economics as an Applied Science

Focus: This is about the practical use of economic

theories and tools to solve real-world problems.

• Role: Economists use their knowledge to address

issues like:

o How to reduce unemployment.

o How to stabilize prices (preventing inflation or

deflation).

o How to promote economic growth.

o How to reduce inequality.

Editor's Notes

#5 economics is about managing our limited resources to meet our unlimited wants.