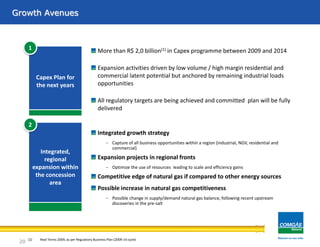

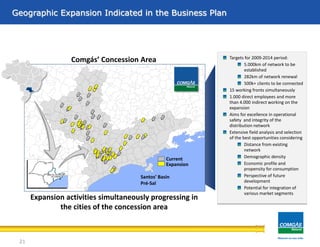

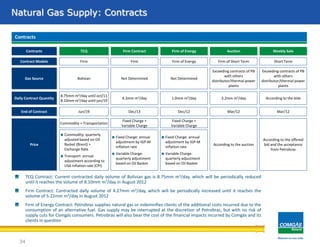

Comgás is a natural gas distribution company operating in São Paulo, Brazil. It has experienced significant growth since privatization in 1999. Comgás' strategic plan focuses on expanding its gas distribution network through new infrastructure projects within its concession area to capture additional residential, commercial, and industrial customers. The plan involves connecting over 500,000 new clients and building 5,000 km of new pipelines by 2014. Capturing growth in the residential segment is a key priority. Comgás also aims to diversify its industrial customer base and bring new corporate clients into its service area.