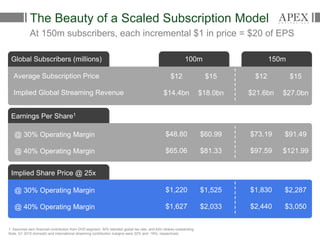

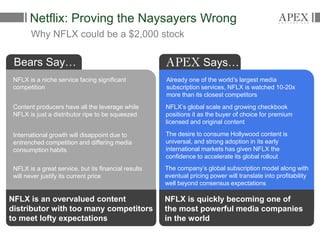

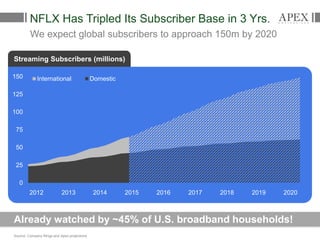

This document discusses why Netflix could become a $100 billion company and reach a stock price of $2,000 per share within 3 years. It argues that Netflix is quickly becoming one of the most powerful media companies in the world as it scales its global subscription business. The document asserts that Netflix's large global subscriber base and growing content library will allow it to be highly profitable with margins over 40%. It projects Netflix could have over 150 million global subscribers by 2020, generating billions in revenues and supporting a stock price over $2,000. However, some remain skeptical that Netflix faces too much competition and high content costs to meet such expectations.

![8

Consumers Already Love Netflix…

57% of the nearly 800 Netflix

users queried said that, if

forced to choose, they would

keep Netflix over traditional

pay TV; 49% reported

spending more time watching

Netflix than traditional pay TV.

- From ClearVoice/FBR Survey Says

Consumes Love It More Than TV by

Barton Crockett, FBR 4/16/2015

Netflix is the 5th most

popular network … [and] is

now considered a must

have channel right behind

most broadcast channels

and ESPN.

- From A Proprietary Service of

“Must See” TV by Marci Ryvicker,

Wells Fargo 3/11/2015

And the service is only getting better](https://image.slidesharecdn.com/apexcapital-nflx2015-150511200716-lva1-app6891/85/Apex-Capital-LLC-Why-Netflix-Will-Be-The-Next-100-Billion-Internet-Company-8-320.jpg)